How do direct indexing ideas fit into a fixed income portfolio? These two powerful strategies make one compelling combination with potential tax and risk management opportunities.

Today’s evolving rate environment has presented new opportunities for investors to enhance income by locking in higher yields. By combining the benefits of professional fixed income management and direct indexing, a bond portfolio can remain resilient through all kinds of market conditions. Let’s explore how customized bond ladders can leverage customization and tax and risk management to meet client goals.

How do customized bond ladders work?

Traditional direct indexing essentially replicates an equity index with the addition of an investor’s customizations. Recreating fixed income indexes in the same way is more challenging. For example, the Dow Jones US Total Market Index is the largest broad-market US equity index and holds about 3,700 stocks. On the other hand, the Bloomberg US Aggregate Bond Index holds more than 10,000 issues.

A bond ladder can be an attractive vehicle for implementing a direct indexing-like approach in fixed income. Bond laddering is a dynamic strategy that may provide predictable income and benefits from rising interest rates. Proceeds from maturing equally weighted investment-grade bonds get reinvested into longer maturities, which typically have higher yields. Through this continuous reinvestment, investors may earn higher income during periods of rising rates.

The reinvestment cycle of bond ladders

Source: Parametric. For illustrative purposes only. Not a recommendation to buy or sell any security.

How does tax management in bond ladders compare to traditional strategies?

One of the inherent advantages of direct indexing is tax efficiency. Funds that include high-dividend or interest-paying securities, like many bond ETFs and mutual funds, generate more pass-through dividends and distributions. Depending on what type of dividend-paying stocks the ETF holds, investors will receive distributions once a year or more frequently. The investor could have to pay taxes on these distributions as ordinary income at 37%, or they may be subject to a holding period. A mutual fund could also leave shareholders owing long-term capital gains taxes on any distributions. All this could leave clients with a higher tax bill.

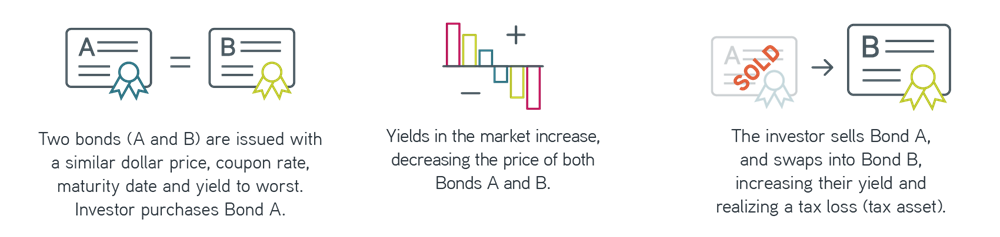

Luckily, laddered portfolios are effective vehicles for year-round systematic tax-loss harvesting. Managers thoroughly analyze liquidity, yield and structure on a bond-by-bond basis, aiming to find loss-harvesting opportunities that help investors take advantage of volatile periods. Proceeds from maturing bonds, calls and coupons offer ongoing opportunities for reinvestment at current rates. These can help reset the portfolio’s book yields and cost basis at a higher rate. Doing this throughout the year can unlock many more losses to harvest than are available only at the year’s end. This is especially true for fixed income, since municipal and investment-grade corporate bond yields have historically rarely peaked in December. Systematic loss harvesting may also help investors avoid poor liquidity conditions that often come about later in the year.

Transform fixed income opportunities into optimization

How tax-loss harvesting works in fixed income

Source: Parametric. For illustrative purposes only. Not a recommendation to buy or sell any security.

How can investors manage risk through customization?

Customization is a key feature of direct indexing. Clients get to decide on their exact asset allocation through individual exposures based on their needs. For fixed income, this allows for flexibility around exposures such as state preferences for municipal bonds, maturity, credit parameters and risk management for corporate bond portfolios. Investors can also select bonds across asset classes—munis, Treasurys and corporates—based on their individual tax profile, which includes their federal marginal rate and any applicable state and local income taxes. In environments where market dislocations occur or tax brackets change, an investor may benefit from optimizing across asset classes to potentially achieve a higher after-tax yield.

Direct indexing also offers investors the ability to align their fixed income exposures with their values. For corporate bonds, investors can choose from a variety of environmental and social screens based on business involvement, reporting transparency or analyst ratings. For munis, investors can opt to invest the bond’s proceeds in projects with certain community impacts.

Clients can also escape concentrated positions through a diversity of assets in fixed income and beyond. Among the many risks to holding concentrated positions is having high exposure to one issuer. This would be the equivalent of holding a high percentage of a single stock in an equity portfolio. An effective manager will have lower maximum concentrations in a single issuer and look to diversify across various states in a national portfolio. Partnering with a professional credit team enables managers to build out high-quality portfolios while seeking to proactively manage downgrade risk and stay ahead of emerging credit concerns.

The bottom line

Markets change, and so do investor’s needs. At Parametric, we believe portfolios should be able to adapt accordingly. By leveraging customization and tax management across fixed income as well as equities, we help clients build portfolios that can better align with current market environments and their long-term goals.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

06.23.2026 | RO 4595219