In environments of geopolitical stress, diversification* is tested, and investors may need to think more wholistically about the assets included in their portfolio.

Diversification is supposed to be an investor’s first line of defense. The logic is familiar: If stocks provide growth, and bonds provide stability, then together they should help a portfolio weather most market environments.

But that relationship has never been guaranteed, and the escalation of hostilities in the Middle East is a timely reminder. As geopolitical tensions rose, markets quickly focused on the risk of disrupted energy flows, higher oil prices and a broader stagflationary impulse. We’ve seen that an oil story is rarely just about oil, and a sustained energy shock tends to reshape the entire macroeconomic backdrop—increasing the odds that stocks and bonds move together again.

Historically, one asset class that has behaved differently during geopolitical stress is commodities. The case for commodities is about owning a diversified basket of raw materials—not just oil—that may respond to global economic and geopolitical shifts unlike traditional assets.

Limits of the traditional core portfolio

The military conflict with Iran illustrates how quickly geopolitical events can ripple through financial markets. Fighting in the Middle East immediately raised concerns about global energy supply—particularly around critical transit points such as the Strait of Hormuz. Oil prices may have reacted first, but the economic effects don’t stop there.

Higher energy prices can push inflation higher while simultaneously weighing on economic growth—a combination commonly referred to as stagflation. When that happens, the traditional relationship between stocks and bonds can break down.

Historically, the negative correlation between equities and bonds depends on a relatively stable macro environment where growth and inflation move together. When growth accelerates, inflation often rises modestly, and equities perform well while bonds weaken.

But oil shocks may disrupt that dynamic by pushing inflation higher while slowing economic activity—a potential shift that markets have begun to fear in recent weeks. Rising energy prices tied to geopolitical instability have increased the risk of both slower growth and higher inflation, raising the possibility that stocks and bonds could once again move in the same direction.

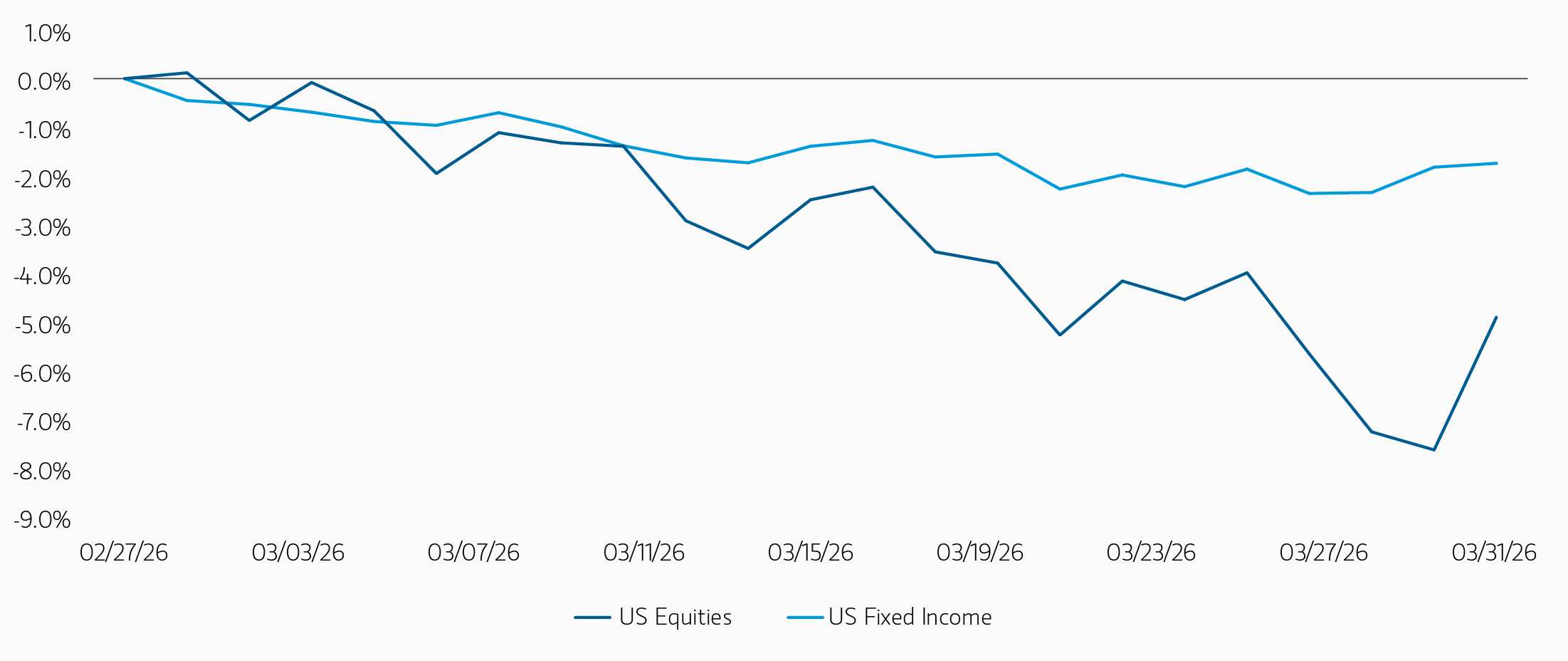

We already see evidence of this dynamic. As the Iran conflict intensified, both equity and bond prices declined in unison, eroding the protective role fixed income has typically played in a diversified portfolio.

Percentage change in US equities and bonds since the Iran conflict began

Past performance is not indicative of future results.

Source: Bloomberg and MSCI, as of 03/31/2026. US Equities represented by MSCI USA Gross Total Return Index and US Fixed Income by Bloomberg US Treasury Index. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses.

For investors relying exclusively on stocks and bonds, this scenario poses a serious threat. If both assets struggle simultaneously, the portfolio loses its primary source of diversification. This is where we think commodities could enter the discussion.

Why diversified commodities may improve portfolio resilience

Commodities have historically provided a diversification benefit when held in combination with traditional assets, such as stocks and bonds. That benefit is realized through the relatively high volatility and low correlation that commodities have exhibited with other risky assets.

A key distinction of commodities relative to other financial assets is that they represent the raw materials underpinning the global economy. Because supply disruptions, geopolitical rifts and shifts in real economic demand drive their prices, they often respond positively to the same shocks that can challenge stock and bond performance. Stocks are claims on future earnings, which are vulnerable to weaker demand and higher input costs. Bonds are claims on nominal cash flows, which are vulnerable when inflation expectations rise. Commodities, by contrast, tend to reprice in the opposite direction when scarcity becomes the market’s dominant concern, and that may work in the investor’s favor.

This helps explain why commodities may outperform traditional assets during geopolitical stress. In a sense, commodities could be described as carrying a positive geopolitical risk premium. In other words, investors are compensated for owning assets whose prices tend to rise when the world becomes more resource-constrained, less predictable or more fragile.

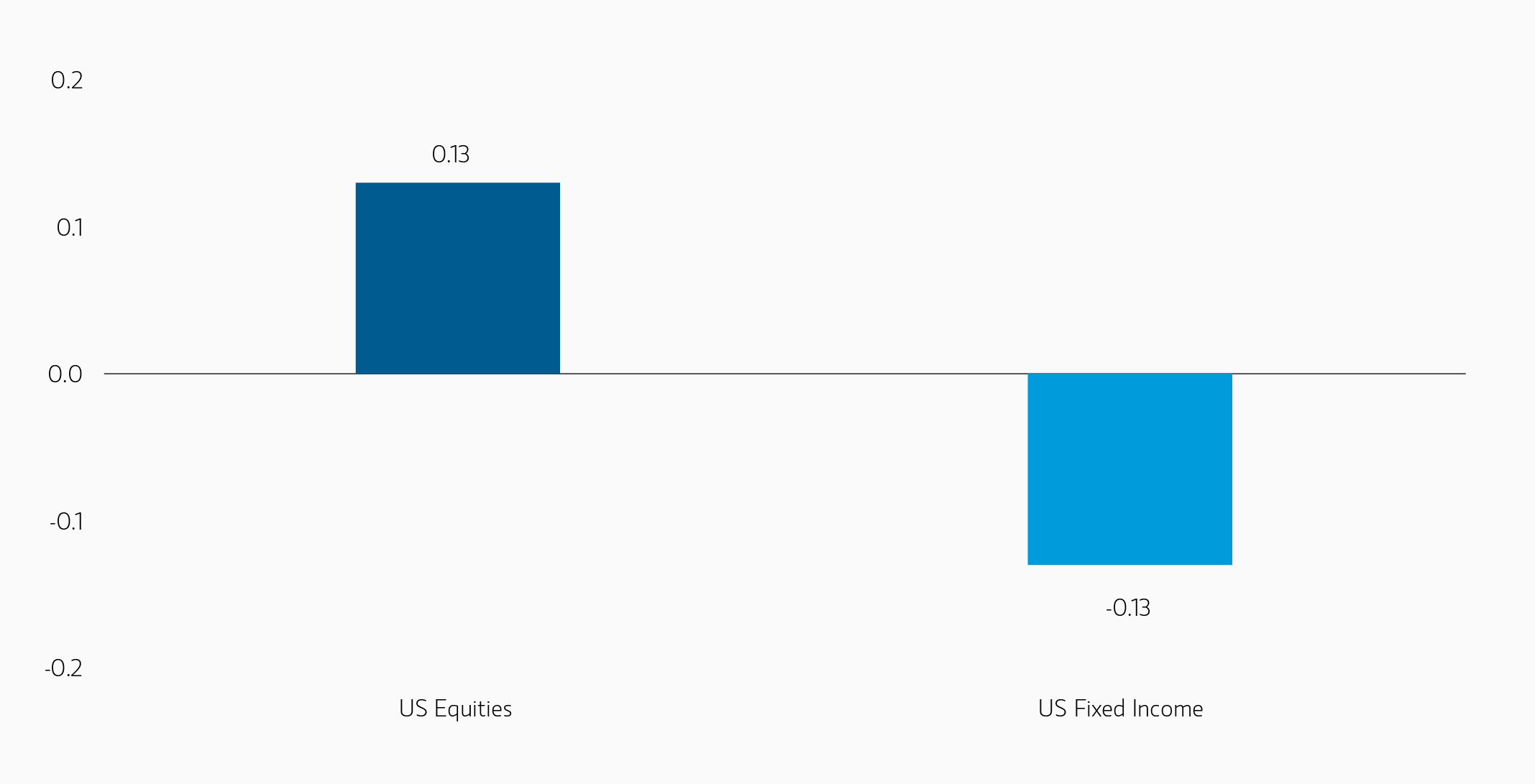

Over the last half-century, a commodity index such as the Bloomberg Commodity Index had a 0.13 correlation with US equities represented by MSCI USA Gross Total Return Index and -0.13 with US fixed income represented by the Bloomberg US Treasury Index. As an asset class that tends to zig while others zag, commodities may help lower expected volatility versus a portfolio that doesn’t contain them, potentially improving resilience.

Risk management solutions for uncertain markets and inflationary periods

Bloomberg Commodity Index correlation with US equities and bonds from 1973 to 2025

Past performance is not indicative of future results.

Source: Bloomberg and MSCI, as of 03/13/2026. US Equities represented by MSCI USA Gross Total Return Index and US Fixed Income by Bloomberg US Treasury Index. Correlation is a statistic that describes the size and direction of a relationship between variables, measured by a coefficient ranging from -1 to +1 indicating a stronger negative or positive relationship. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses.

The lesson here is not replacing a portfolio with oil—in fact, it’s the opposite. Geopolitical events are inherently unpredictable, so investors would be hard pressed to know in advance which part of the commodity complex could feel the strain most acutely. One episode may center on crude oil and refined products. Another may hit grains through disruptions in the Black Sea region. Yet another may move industrial metals through sanctions, shipping bottlenecks or power shortages. We believe a broad basket of commodities helps provide more robust diversification because it may improve the odds of capturing the impact of the next shock—whatever form that takes.

The bottom line

Recent geopolitical events involving Iran highlight a challenge for investors: Diversification may falter when inflation and growth move in opposite directions. In these moments, traditional stock and bond portfolios may struggle to provide the balance investors seek. Commodities may offer an additional source of diversification. Their performance tends to improve during geopolitical stress—precisely the environment where traditional assets can face pressure.

For investors thinking about long-term portfolio resilience, the idea isn’t to abandon stocks or bonds, but rather to consider a modest allocation to commodities. A diversified basket of commodities may provide exposure to a unique opportunity set that stocks and bonds alone cannot capture.

* Diversification does not eliminate the risk of loss.

The value of commodity investments will generally be affected by overall market movements and factors specific to a particular industry or commodity, which may include weather, embargoes, tariffs, health, political, international and regulatory developments. Economic events and other events (whether real or perceived) can reduce the demand for commodities, which may reduce market prices and cause their value to fall. The use of derivatives can lead to losses or adverse movements in the price or value of the asset, index, rate, or instrument underlying a derivative due to failure of a counterparty or due to tax or regulatory constraints.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

04.05.2028 | RO 5359269