With interest rates rising to attractive levels, why are some fixed income investors still on the sidelines? Find out why we believe it’s time to take advantage of a potentially overlooked opportunity.

A growing number of investors share our favorable outlook for short- and intermediate-term investment-grade (IG) corporate bonds, as evidenced by the strong year-to-date inflows into high-quality fixed income funds and separately managed accounts. Our investment thesis rests on three main pillars:

- The highest all-in yield since 2009 provides a solid cushion against additional interest rate increases and wider spreads.

- IG companies used the extraordinarily low postpandemic rate environment to help insulate their balance sheets against rising rates.

- The odds of a hard economic landing appear to be receding.

Despite this compelling value, many investors remain on the sidelines, waiting to deploy their cash until interest and credit risk further subside. They cite the risk of even higher rates, the narrowness of credit spreads, the supposed maturity wall, and the likelihood that a recession could create sharply wider credit spreads. Today we’ll attempt to address those concerns.

What’s the impact of rising interest rates on the bond market?

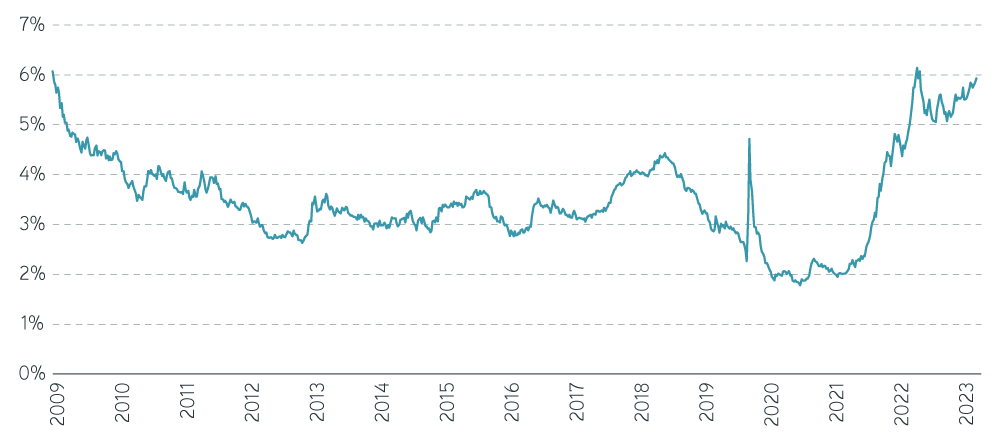

The strongest argument for investing in IG bonds is that the high starting yield provides a substantial margin of error. At over 6%, the yield of the ICE BofA US Corporate Index represents the highest all-in yield since June 2009. As a result, a one- to five-year IG corporate ladder could withstand a 325 basis point (bps) rise in yield and still generate a positive one-year return. At the same time, a one- to 10-year IG corporate ladder could still produce a positive one-year return as long as the increase is 150 bps or less. Of course, for investors with an investment time frame beyond one year, the cushion increases along with the time horizon. This is true whether corporate bond yields rise because of higher US Treasury rates, wider credit spreads, or any combination of the two. Our Laddered Interest Rate Scenario Tool allows investors and their advisors to shock yields (moving the curve higher or lower) and view the impact on returns for ladder structures of different maturity ranges and credit quality.

ICE/BofA Corporate Bond Index yield to worst, June 2009–September 2023

Source: ICE/BofA, 9/22/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

What’s behind narrowing credit spreads in the corporate bond market?

Another concern investors raise is whether spreads offer adequate compensation for the market’s current level of credit risk. Since the beginning of the year, the option-adjusted spread of the ICE BofA US Corporate Index has narrowed from 138 bps to 128 bps, bringing it below its 10-year average of 131 bps but still above its June 2021 low of 86 bps. We believe we can attribute much of the recent spread narrowing to the strong demand for the asset class.

But it’s also possible to attribute the spread to the recognition that IG balance sheets are in solid shape. For instance, interest coverage—a company’s ability to service its debt—remains strong, although it has declined as companies refinance debt at higher yields. According to the latest Barclays US Investment Grade Credit Markets quarterly update, companies currently generate enough cash flow to cover their interest expense 12.3 times, well above the levels seen before the last four recessions.

Is a maturity wall coming to the corporate bond market?

It’s worth noting that because IG companies used the low-rate environment to issue longer-maturity bonds, higher rates are just beginning to flow through to balance sheets. Because rates rose after the issuance, they pay far less in coupon interest than current market rates imply.

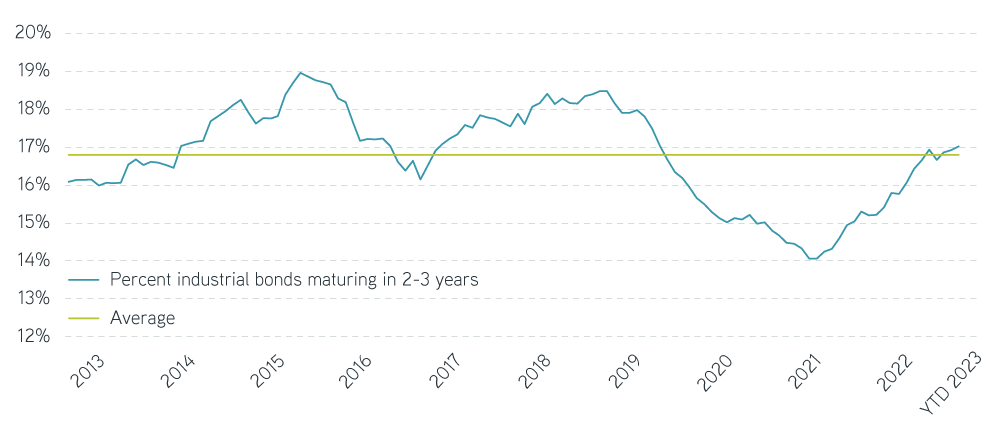

Another reason investors cite for avoiding the IG sector is the supposed maturity wall. The argument is that IG corporates face a daunting number of maturities over the next two to three years that might force them to issue new debt at much higher rates. But that overstates concerns around IG company refinancing risks. IG companies used the extremely-low-rate environment to refinance and prefund existing debt, and they issued longer-maturity bonds at the same time. We see this in the average maturity of the debt in the corporate index over time. Before the 2019 rate cuts, the average maturity of debt in the index was 11.2 years. By the end of 2021, just before the first Fed rate increase, the average maturity had extended to 13.2 years. Looked at another way, index maturities in 2024 and 2025 for US industrials are only roughly 17% of the total outstanding debt. This is very near the long-term median and may push up corporate funding costs, but only moderately so.

Average corporate index debt maturity, 2013–2023

Source: ICE/BofA, 8/31/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

How high is the risk of a recession in 2024?

If the economy enters a recession, credit spreads could potentially double from their current levels to the low 200s in bps. This would be roughly equivalent to the widest levels reached during the 2001 recession, which is a good reference point because it was the last “normal” cycle before the great financial crisis. Assuming the spread widening occurred over the course of a year, even a one- to 10-year ladder could easily cover this amount and produce a positive one-year return. The cushion is likely to prove much larger, because such a recession would very likely see Treasury rates fall, potentially offsetting some or all the spread widening.

While we still think the odds favor a mild recession in 2024, the resilience of the economy continues to pleasantly surprise. Consumer confidence—buoyed by rising wages and sharp increases in interest income—remains solid, and the GDP continues to expand at a satisfactory rate. The improvement has led the Fed to remove a recession from its base case. With inflation improving significantly, the Fed appears to be nearing the end of its rate-hiking campaign. Because the lags in monetary policy are working their way into the real economy, the bulk of last year's rate increases have yet to be reflected in current activity. But because of IG companies’ postpandemic restructuring, they have very strong balance sheets and very modest refinancing needs. We should therefore see significantly less deterioration in credit metrics than in past recessions. In fact, credit rating trends continue to be positive, with several large companies moving from high-yield to IG.

The bottom line

We believe IG bonds, particularly when used in the ladder structure, should provide solid near-term incremental returns. Attractive yields approaching 6% make corporate ladders less vulnerable to rising rates, and corporations are better positioned to avoid downgrades than in past cycles. The current corporate bond market, therefore, presents opportunities fixed income investors may be overlooking.