We expect the US economy to remain resilient in 2026, providing a constructive backdrop for risk assets, as well as corporate and municipal credit. But the mix of macro uncertainty, policy division and elevated deficits could widen the range of potential outcomes and increase rate volatility—especially as the Federal Reserve approaches the neutral rate.

In our view, investors should prepare for a market where interest rate swings are more frequent, reinforcing the need for active management across fixed income portfolios.

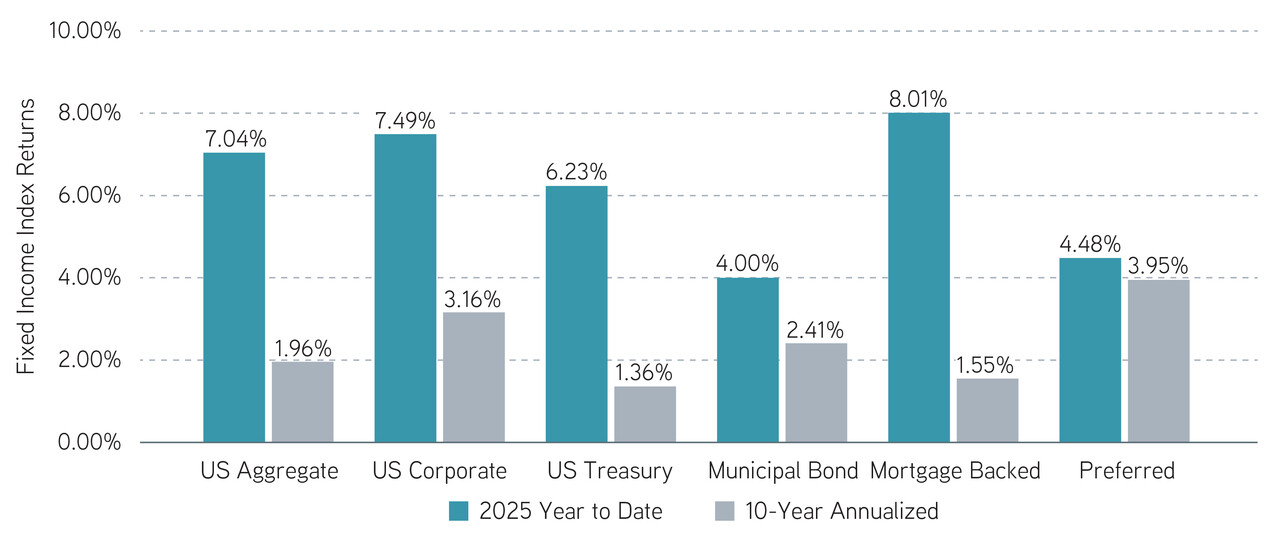

Strong 2025 despite persistent headwinds

Markets once again demonstrated their resilience in 2025. Supportive monetary and fiscal conditions, steady consumer spending and robust AI-driven business investment underpinned broad strength across risk assets—even as investors navigated inconsistent economic data, policy uncertainty and ongoing geopolitical disruption.

Equities reached new all-time highs and delivered another year of double-digit returns. Yet fixed income also posted meaningfully positive performance. Elevated starting yields and continued progress toward rate normalization helped most fixed income sectors outperform their long-term averages. For many fixed income investors, 2025 highlighted the benefits of maintaining strategic duration exposure—even amid uncertainty.

Fixed income index sector performance through December 1, 2025

Source: Bloomberg US Aggregate Index, Bloomberg US Corporate Index, Bloomberg US Treasury Index, Bloomberg Municipal Bond Index, Bloomberg US Mortgage Backed Securities Index, ICE BofA Preferred Index, data as of 12/01/2025. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees and expenses. Past performance is not indicative of future results. All investments are subject to risk, including the risk of loss.

The US Federal Reserve heads into 2026 with a cautious, data-dependent stance. Labor market momentum has weakened: After averaging 167,000 new jobs per month in 2024, job growth has slowed sharply to just 38,000 per month since May, with the unemployment rate reaching 4.4%—its highest level in nearly four years.

Yet inflation remains stubborn: Year-over-year readings hover near 3% as tariffs feed into price levels, while progress toward the Fed’s 2% target has stalled. Even as policymakers maintain that current policy is restrictive, the strong consumer and ongoing AI-related capital expenditures have kept GDP near 3% for several consecutive quarters, leaving the Fed in an uncomfortable position. Supporting employment risks fueling inflation, while maintaining restrictive policy risks slowing the economy too sharply.

Policy division and market expectations

With inflation still running about 1% above target, and without clear signs of labor market deterioration, divided policymakers have been hesitant to cut rates meaningfully. Both sides of the debate carry strong conviction, and uncertainty surrounding the path of rate cuts may persist throughout 2026.

A sustained decline in inflation or a more significant rise in unemployment might be required to move the federal funds rate toward 3%. While the Fed may tolerate some inflation risk to support employment, more rate cuts amid cyclically reaccelerating growth could reignite the upward price pressures that voters are so sensitive to.

Complicating matters further, a fiscal deficit projected to exceed $1.7 trillion in 2026 (over 6% of GDP), concerns over central bank independence and an upcoming Supreme Court decision on tariff authority under the International Emergency Economic Powers Act (IEEPA) all appear poised to keep the term premium elevated and the yield curve steep. These forces suggest that even if the Fed eases, long-end yields may not fall in a straight line.

Here are some possibilities to consider for fixed income portfolio positioning in 2026:

Add duration thoughtfully. Even after a wave of inflows, many investors remain underweight duration and bonds overall. With yields still near decade highs, fixed income may warrant a more prominent role in diversified portfolios. Higher starting yields have historically correlated with stronger forward return potential, and high-quality municipals and corporate credit could offer valuable downside risk mitigation should equity markets experience volatility.

Reassess cash allocations. If the Fed proceeds with additional rate cuts, yields may decline on cash instruments—cash sweeps, CDs and T-bills. Extending modestly along the curve could allow investors to lock in today’s elevated yields, while introducing duration exposure with the potential to stabilize the portfolio if growth slows.

Prioritize professional credit oversight. AI-related capital spending has been extraordinary in scale, yet the payoff path remains uncertain. As investment accelerates and supply picks up, strains may emerge unevenly across issuers. Credit fundamentals look solid today, but spreads are tight, leaving little cushion for surprises. These dynamics point to greater credit dispersion in 2026, which could make disciplined, professional oversight more critical than ever.

Use tax loss harvesting opportunistically. With potential volatility on the horizon, systematic tax loss harvesting within fixed income SMAs could enhance after-tax outcomes and provide valuable flexibility and tax savings when rebalancing. Providers with year-round harvesting capabilities may offer meaningful value.

Embrace active management. With several plausible macro paths ahead, active management provides the tools to help turn volatility into opportunity. Dynamic decision-making around duration, curve positioning, credit exposure and security selection may allow investors to capture opportunities that passive strategies could overlook, while managing emerging risks better. In an environment defined by policy uncertainty and shifting rate dynamics, active fixed income management can become a strategic differentiator.

Solutions for today’s complex interest rate environments

Here are our outlooks for munis, corporates and preferreds in 2026:

Municipals

• Bloomberg’s BVAL AAA Muni Yields remain near decade highs and above long-term averages, up 20–60 basis points (bps) since the Fed started rate cuts in September 2024. Over the past decade, the yield on the Bloomberg Municipal Index has exceeded current levels only 20% of the time.

• Tax-exempt yields of 3% to 4% are likely to attract buyers. For high-income investors in states with high taxes, this can mean tax-adjusted yields of 6% or more—offering competitive value compared to other fixed income and equity options.

• The municipal curve has been significantly steeper than the Treasury curve, offering buyers attractive compensation for extending maturities. For investors transitioning out of cash and preparing for the next stage of the interest rate cycle, extending moderately along the curve may provide an opportunity to increase income while mitigating reinvestment risk.

• Muni fund inflows reached $47 billion in 2025, surpassing 2024 totals. This trend may continue into 2026, as rate cuts have historically driven positive net inflows during easing cycles.

• Muni issuance hit a record $535 billion in 2025, up 30% from the five-year average. High supply has sometimes led to underperformance and higher ratios, but also created attractive entry points. We expect another record year in 2026, potentially offering similar opportunities when net supply rises.

• Municipal credit remains strong, with rainy day funds averaging 15% of state spending in 2025. Solid reserves could help states offset Medicaid cuts with limited effect on their credit ratings. With muni spreads holding steady or tightening, upgrade-to-downgrade ratios may slow but stay at or above parity.

• We believe the muni market could see stable to improving returns depending on yield curve positioning, with better performance possible at the long end of the curve.

Corporates

• Investment grade (IG) credit returned just over 8% in 2025 through November, driven by declining Treasury yields and steady corporate fundamentals.

• Spreads to Treasurys remain historically tight around 80 bps—about where they started the year despite volatility around higher tariffs and shifting Fed expectations. The IG asset class has demonstrated notable resilience to macro and policy shocks.

• We remain constructive on IG heading into 2026, as major sources of uncertainty appear to have passed their peak: Trade policy ambiguity has diminished, and tariff impacts are clearer. Economic growth worries have lessened as earnings growth remains strong and may expand with AI. Debt service pressures are easing, helped by Fed rate cuts that have stabilized credit.

• The Fed’s rate cuts may also be expected to bolster consumers as real incomes and spending stay resilient, with overall delinquencies still under control despite some subprime weakness.

• Bank credit remains resilient, thanks to high capital ratios, ample liquidity and healthy asset quality in both consumer and commercial sectors. US banks have consistently posted solid earnings, showing constructive credit trends and robust capital markets activity.

• We view spread pressure in certain AI-linked technology issuers and financial borrowers exposed to private credit as idiosyncratic rather than systemic. While front-loaded AI capital expenditure has created dispersion across issuers, IG technicals remain firm overall, and the broad sector still trades with solid sponsorship.

• As supply from AI-driven capex and elevated refinancing needs increases sharply, fundamentals and technical demand may serve as anchors for IG—pointing to a carry-driven year, with selection and curve positioning gaining importance.

Preferreds

• Preferreds may benefit from strong issuer fundamentals and renewed investor demand, as the Fed’s expected rate cutting cycle tends to increase interest in high-quality fixed income and improve the relative value of preferred securities versus cash and short-duration instruments.

• Financial preferreds have outperformed again in 2025, supported by resilient credit quality, improving capital markets activity and robust net interest income. We expect these positive earnings trends to continue into 2026, reinforcing the sector’s role as a core anchor of the preferred market.

• Limited net supply remains a key technical tailwind: Updated US regulatory requirements have created incentives for banks to reduce Additional Tier 1 (AT1) capital, which may point to modest preferred issuance in 2026, while the scarcity of new paper could support pricing and compress spreads for high-quality issuers.

• Fundamental strength across banks has enhanced the credit profile of preferreds, helping to keep Common Equity Tier 1 (CET1) ratios elevated, liquidity robust and credit costs contained across consumer and commercial portfolios. Deregulation and improved capital markets throughput have added to the constructive backdrop.

• Utility hybrids may continue to grow as a share of the preferred and hybrid universe, with increased issuance to cover their rising capital spending for grid modernization, as well as higher power demand from data centers. Despite higher supply, valuations have remained attractive relative to senior utilities debt.

• In our view, preferreds may offer high, tax-advantaged income, with starting yields well above their 10-year averages—providing attractive carry and the potential for solid total returns in 2026, driven primarily by coupon income and supported by an improving rate environment.

Past performance is no guarantee of future results. The returns referred to in the blog are those of representative indexes and are not meant to depict the performance of a specific investment.

Parametric and Morgan Stanley do not provide legal, tax, or accounting advice or services. Clients should consult with their own tax or legal advisor prior to entering into any transaction or strategy described herein.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

12.11.2026 | RO 5051867