Corporate pension funding continues to improve. Market moves over the last five years, both in yields and equity returns, have corporate pension plans at funding levels not seen since before the Tech Bubble.

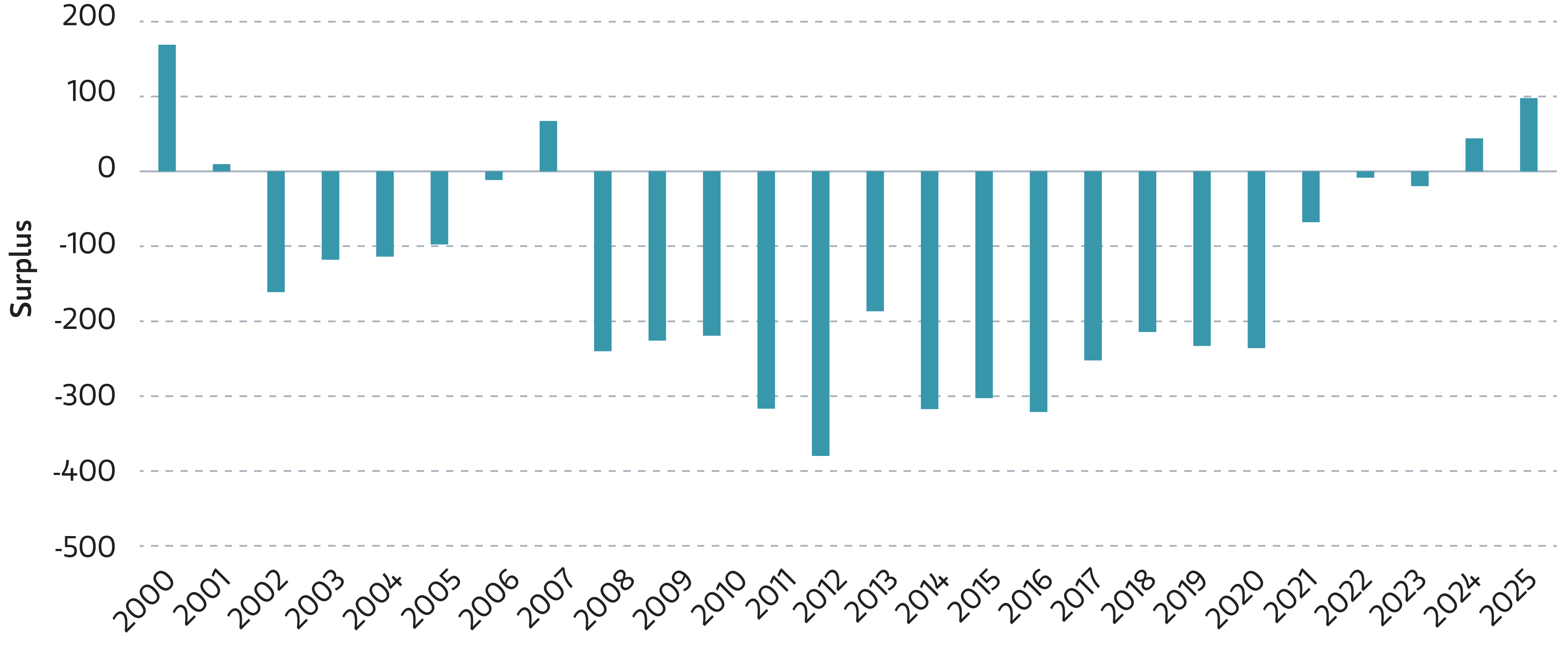

According to the Milliman 100 Pension Funding Index, the year-end funding ratio has climbed from 80.9% in 2016 and 103.6% in 2024, up to 108.1% in 2025.

Milliman 100 Pension Funding Index: Surplus improved again in 2025

Source: Milliman, 12/31/2025. Surplus = Assets (MV) – Liabilities (PBO), while Funding Ratio = Assets / Liabilities. For illustrative purposes only. Past performance is not an indicator of future results. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses.

Reviewing the environment for pension investing

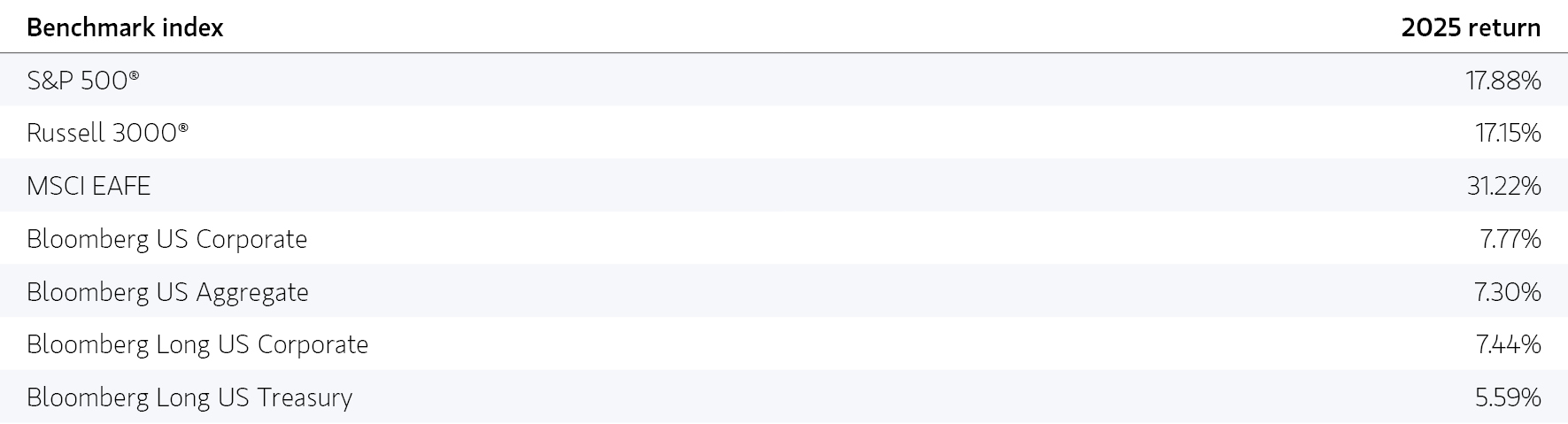

Equity market returns pushed funded ratios upward again in 2025, with returns in the high teens in the US and exceeding 30% in developed international markets. In the meantime, liabilities stayed around the same level. Steepening yield curves also helped funded ratios increase, as the long, volatile liability cash flows are discounted over longer periods and at higher rates than the shorter cash flows.

Given such robust equity returns, it might seem that funded ratios should be even higher, but we’ve reached a stage where many plans seek to take a smarter approach to managing the assets against the liabilities, rather than simply shooting for higher returns.

Benchmark index total returns in 2025

Source: S&P Global, Russell, MSCI, Bloomberg data as of 12/31/2025. For illustrative purposes only. Past performance is not an indicator of future results. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses.

Refine and enhance liability-driven investing strategies

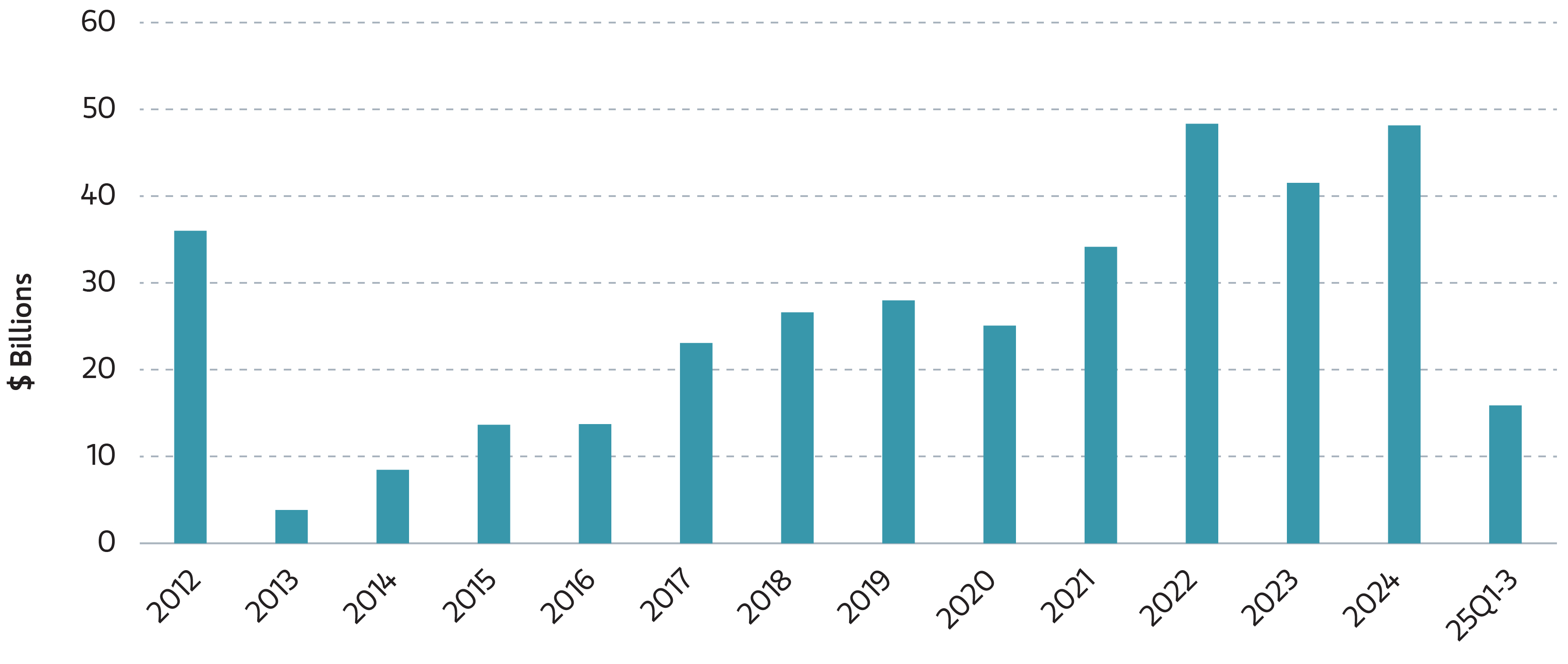

With better funded ratios, we might expect to see greater interest in Pension Risk Transfers (PRT), consistent with the trend we’ve observed in the past. Based on the data available through the third quarter, however, the 2025 numbers appear to buck that trend. According to LIMRA, corporate pension buyouts were less than half of the prior year in each of the first three quarters of 2025. Depending on fourth quarter numbers, last year’s total could be the lowest amount of PRT activity since 2016.

LIMRA pension buyout sales in 2025 on track to reversing long-term trend through Q3

Source: LIMRA data as of 9/30/2025. For illustrative purposes only. Past performance is not an indicator of future results. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses.

Avoiding past mistakes in pension management

Pensions have been here before and made mistakes that ended up costing them for years. How can we help them avoid the mistakes of the past?

Worth noting going forward is the reduction in buyouts, which has commonly been attributed to an increase in lawsuits brought forth by plan participants who contend that their benefits have been replaced at lower value though PRT annuity purchases. The argument is that PRT is akin to forcing a trade from an investment grade bond to a high yield bond that has the same cash flows but is less valuable.

Many of the lawsuits have been dismissed, and the Department of Labor (DOL) has recently filed briefs in several cases supporting annuity purchases. As other lawsuits progress through the courts, plan sponsors may want to consider whether they want to take on the risk of being tied up in litigation.

We could make additional arguments for hesitating with buyouts. The termination process takes time and effort, with the end result remaining uncertain until completion. In a volatile world, other matters might take precedence over this type of project. Unless the plan is fully terminated, the plan sponsor would still have a plan to manage—and that could be harder with fewer assets and more volatile liabilities. In other words, unanticipated problems may surface.

Investment strategies have been developed over the last couple of decades that can potentially lead to more efficient funding risk mitigation. A well-funded plan may be relatively easy to operate with good, transparent investment management, requiring little effort and less risk to the sponsoring organization over a long period. If there’s no harm in waiting, why rush into a buyout?

Buyout or no buyout, we think the most important thing to do with a pension surplus is avoid losing it. We’ve seen more than enough examples of well-funded plans becoming poorly funded to have learned that lesson. We believe plan sponsors should endeavor to invest intelligently and know every risk they are taking—not allowing themselves to be fooled by solutions that could expose the plan to new and unknowable basis risk.

Applying LDI strategies may help eliminate the possibility of falling below full funding by investing in assets that aim to behave in line with liabilities. Once a framework is in place that seeks to mitigate downside risk, then plan sponsors may take whatever risk they can accept to grow the surplus further. Unless the plan is open and expanding, and asset growth is needed to offset future accruals, then surplus growth can be secondary to maintaining full funding.

Seeking to mitigate pension funding risk

Markets giveth, and they taketh away. During past episodes of market turmoil—Tech Bubble, Global Financial Crisis and Sovereign Debt Crisis—pension funding was severely damaged to the point that many sponsors closed, froze or terminated their plans. Underfunding has been weighing on corporations’ financials for more than 20 years. But markets in recent years have provided a gift of full funding to most of those plans. How should sponsors respond?

We think the answer, above all else, is to avoid the mistake of letting full funding slip away. Most plans have indeed learned to manage their investments prudently, implementing more appropriate investment strategies using LDI that have allowed for the current level of funding. In recent years, many plans have chosen to offload all or part of plan liabilities to insurance companies to reduce the influence of pension liabilities on financial statements. As we’ve seen, that trend has slowed, at least temporarily, for good reasons.

The bottom line

With sensible strategies that have been developed over the last two decades, we believe a well-funded plan may continue for many years with little risk to the plan sponsor. The strategies require transparency and customization to help limit downside outcomes by investing in LDI assets that behave in line with pension liabilities. Now sponsors may lock an attractive lower bound and avoid unnecessary basis mismatches between assets and liabilities. Then they can try to grow the surplus, of course, but only as a secondary consideration to preserving a minimum funded status.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

02.03.2028 | RO 5182695