At Parametric, our years of experience have taught us that markets can swing up and down quickly and without warning. Since no one can time these swings, we believe it's imperative to seek both loss harvesting and benchmark tracking simultaneously.

This year’s market turbulence has created excellent opportunities for harvesting tax losses. While volatility may help unlock tax benefits, it can also magnify pretax performance differences—reinforcing the need for strong risk controls. That’s why Parametric direct indexing has a dual mandate of effective tax management and disciplined index tracking.

With over 30 years of experience in tax managed direct indexing strategies, Parametric has guided clients through numerous volatile market periods—from the dot-com bubble to the global financial crisis to the COVID pandemic. We’ve seen time and time again the reversal risk that occurs after equity market downturns, when the worst performers with the greatest opportunity for loss harvesting become the best performers in the recovery.

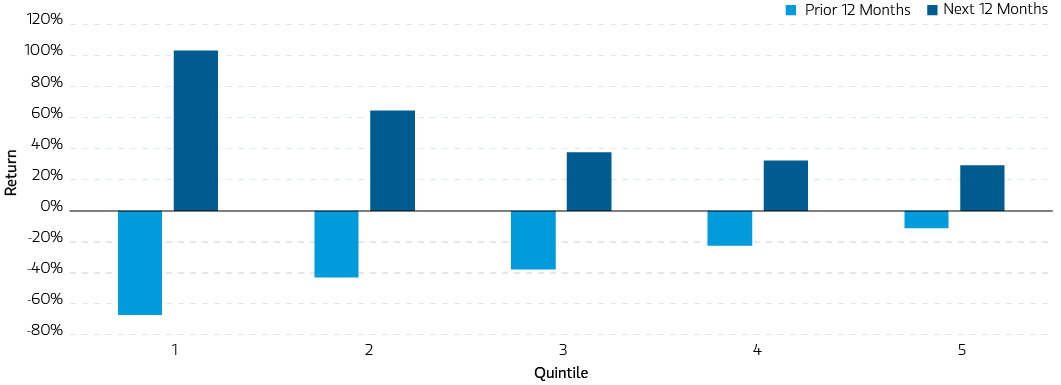

For example, during the global financial crisis, the bottom quintile of stocks in the S&P 500® in 2008 were the top performing quintile in 2009.

S&P 500® market returns, 2008–2009

Source: S&P 500® Index, data as of 2009. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses. Past performance is not indicative of future results.

Harvesting losses from the hardest-hit positions may result in underweighting the names that tend to outperform in the recovery, which leads to a portfolio underperforming its benchmark.

At Parametric, we’re always striving to improve client outcomes by enhancing our portfolio management process. In recent years, we’ve added two significant risk controls that help to address both market and stock-specific risk simultaneously and continuously, without negatively impacting the potential tax benefit of direct indexing.

Targeting market risk with systematic factors

Parametric has always been cognizant of market-level reversal risk following stock market crashes, including the pandemic-induced bear market in 2020.

Historically, our approach to managing this risk was to intervene by tightening risk controls across the board during periods of extreme market volatility, then resuming a standard posture once volatility subsides. We found two main drawbacks to this approach:

1. Broad-based tightening of risk management could reduce the portfolio manager’s latitude to capture available tax alpha.

2. Market timing during the volatility of a crisis could be particularly challenging.

To improve the risk controls without reducing potential tax alpha, our research team identified three systematic factors most associated with this reversal risk: beta, momentum and short-term reversal. While beta and momentum are common risk factors incorporated into most fundamental risk models, short-term reversal is a proprietary trading factor that we had to develop in house.

After extensive research and testing, our team determined that by incorporating the short-term reversal factor and increasing controls of the existing beta and momentum factors, we could potentially improve post-crash portfolio performance—without sacrificing tax alpha or increasing tracking error and turnover.

Consider the benefits of active tax management

Addressing stock-specific risk with increased controls

In direct indexing, it’s common to look at individual stocks for their loss harvesting potential and to focus on market-level forces like industry, sector or country for portfolio performance. Yet we’re finding that individual stocks are becoming more and more impactful on performance as market concentration continues to increase.

In particular, we’ve observed that individual stocks can have a material impact on portfolio performance when they have high volatility, and that impact increases as their weight in the index rises.

Suppose a stock with a large index weight has a big decline, which we seek to loss harvest. Although we have limits on the weight of the stock relative to the benchmark, we would likely be underweight this stock after loss harvesting.

If this stock rallies strongly, outperforming the rest of the index, that underweight position would cause the portfolio to lag the benchmark. The greater the underweight of the stock compared to the index and the greater the outperformance of that stock versus the benchmark, the worse the performance impact on the portfolio.

We saw this when some of the largest holdings in the S&P 500® experienced a notable decline in late 2022, then recovered quickly and steeply in the first quarter of 2023.

After that, Parametric implemented a method to increase controls on stocks with greater stock-specific risk. Essentially we’re trying to balance the benefit of loss harvesting a declining name with the risk that it might subsequently outperform the index and lead to portfolio underperformance.

After extensive research, we found an intuitive way to limit this risk: demand deeper losses from more risky stocks before loss harvesting. In practice, this method results in smaller underweights of the most risky names. Our portfolio management process also actively prioritizes buying these stocks back when they are out of the wash sale1 period—further reducing the underweights.

This is all implemented automatically during the portfolio construction process, with the risk controls maintained in the background. That allows portfolio managers to focus more on loss harvesting.

The bottom line

When markets are on the decline, investors tend to focus on maximizing loss harvesting. When markets rebound, however, no one wants to be left behind, and attention turns to how well portfolios are tracking the index on the upswing.

Our discipline of ongoing research and improvement has allowed Parametric to address many challenges that the market has thrown at us. With the certainty of uncertainty in today’s markets, this discipline has become more important than ever.

1 In a wash sale, the same security sold for a loss is purchased 30 days before or after the sale. If a transaction violates the rule against wash sales, the IRS can disallow the loss deduction and add the loss to the cost basis of the repurchased security, which can effectively defer the benefit of the loss.

Parametric and Morgan Stanley Investment Management do not provide legal, tax or accounting advice or services. Investors should consult with their own tax or legal advisors prior to entering into any transaction or strategy.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

06.16.2026 | RO 4579023