Volatility Risk Premium

For institutional investors

The volatility risk premium (VRP) is the compensation earned by investors for providing protection against unexpected market volatility. Parametric’s VRP solutions are a suite of strategies that seek to capture this unique and diversifying risk premium through the systematic sale of call and put options.

![]()

The VRP can be a persistent source of return over time that may allow investors to access attractive risk-adjusted returns and increase overall portfolio diversification.

Investing in an options strategy involves risk. All investments are subject to loss. Learn more.

Explore more VRP solutions

Capturing the VRP effectively and consistently

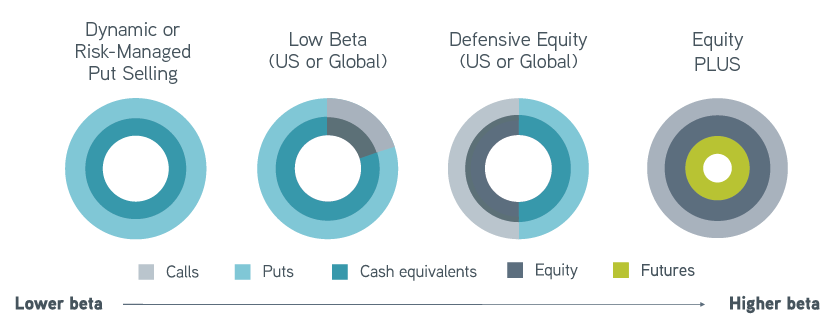

Equity index options may be thought of as financial insurance contracts, and investors pay a premium for insurance-like protection against unfavorable outcomes. The size of the VRP is driven by a range of behavioral, structural, and economic factors that may lead to an imbalance between buyers and sellers of index options.

A defensively structured portfolio can capture the VRP by selling fully collateralized options without introducing leverage. Our rules-based solutions favor diversification, accessibility, and transparency.

Using different combinations of collateralized equity index put and call option positions, your institution can access VRP strategies across a range of equity market betas.

Which VRP solution is right for you?

Why choose Parametric?

More to explore

How Corporate Bond Ladders May Help to Hedge Volatility

by John Hemingway, Vice President, Portfolio Manager

April 28, 2025

With corporate bond ladders, maturities reinvested at higher rates have the potential to benefit the portfolio.

As Tariffs Cloud Outlook, Municipal Bonds May Offer Opportunity

by Jonathan Rocafort, Managing Director, Head of Fixed Income Solutions

April 8, 2025

With growth concerns emerging following tariff announcements, here’s why we see potential opportunity in stepping out of cash, adding some duration and locking in yields near a decade high.