Global Low Beta VRP

Parametric’s Global Low Beta Volatility Risk Premium (VRP) strategy seeks consistent incremental returns by selling fully collateralized equity index options against a conservatively structured base of US Treasuries and global equity.

![]()

![]()

This strategy is suited to investors seeking an alternative to hedge funds; it is designed to deliver more predictable returns, better liquidity, greater transparency, and lower fees.

Investing in an options strategy involves risk. All investments are subject to loss. Learn more.

Explore more VRP solutions

A strategy that

adapts to the market

Global Low Beta VRP employs a rules-based, systematic approach that avoids forecasts and market timing but remains responsive to changing market conditions through the use of dynamic strike prices. Implied volatility drives the determination of strike price, and strike prices move further out of the money in higher-volatility environments. Frequent expirations mitigate risk and allow for the capture of mean reversion in volatility.

Due to economic, behavioral, and structural factors, options buyers are willing to pay a premium to sellers to hedge against the risk of drawdowns and volatility. Global Low Beta VRP capitalizes on this tendency for index options to trade at higher implied volatilities than realized volatility.

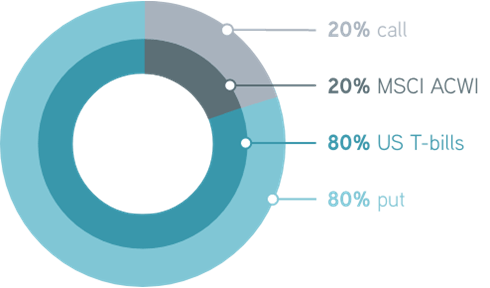

Portfolio construction

Model beta: 0.3

Intended benefits of Global Low Beta VRP

Absolute returns

Learn more >>

Global Low Beta VRP aims to produce total returns above those of US Treasury bills.

Consistency

Learn more >>

Investors gain access to the volatility risk premium, offering the potential for long-term diversification benefits compared to traditional risk premiums.

Systematic

Learn more >>

A stringent rules-based process eliminates behavioral biases and market timing.

Hedge fund alternative

Learn more >>

Global Low Beta VRP is designed to deliver better liquidity, greater transparency, and lower fees than hedge funds.

More to explore

Why Portfolio Overlays Matter in Uncertain Market Environments

by Richard Fong, Managing Director, Overlay Solutions

August 4, 2026

Discover how portfolio overlays help investors manage risk, stay aligned with long-term goals and navigate changing market conditions with confidence.

Fixed Income Midyear Outlook 2026: Higher-Yield Opportunities

by Jonathan Rocafort, Managing Director, Head of Fixed Income Solutions

June 11, 2026

Discover how higher yields are reshaping fixed income in 2026, creating opportunities across bonds as investors navigate volatility, inflation and policy risk.

Factor Investing Endures Despite Tough 2025 for Quality Stocks

by Gregory Liebl, Director, Investment Strategy; Jeff Wagner, Senior Investment Strategist

June 1, 2026

A tough year for quality stocks challenged investors in 2025. Explore why factor investing remains relevant and how multifactor strategies may help.