Direct indexing is growing, and it’s important to know the benefits of different tax-management variables on portfolios. We discuss three vital factors that impact after-tax efficiency: index construction, turnover, and volatility.

Third party research has shown that tax management can add 1-2%1 in after-tax excess returns but there are many nuances between benchmarks that may impact tax management. Wondering what benchmark to target for your clients’ direct indexing portfolio? Investors should ask themselves: What type of regional, market capitalization, and style exposure best suits their needs? And how does a chosen exposure affect after-tax outcomes?

Direct indexing (DI) strategies have been growing rapidly in popularity—and for good reasons. The ability to own the individual stocks that comprise a benchmark makes DI an attractive option for investors seeking tax-efficient, passive equity exposure. Market exposure may be the primary motivation for index selection, but it’s also important for taxable investors to understand what value to expect from tax management. We explore how differences between indexes can affect tax management outcomes.

How do we measure tax management outcomes?

Tax alpha is our preferred way to measure the value of tax management. We calculate tax alpha as after-tax excess return minus pretax excess return. Active tax management entails deferring gains and realizing losses that investors can use to offset gains elsewhere in their portfolio, lowering the overall tax burden. By applying the two techniques and minimizing pretax return differences, an active tax manager can maximize the amount of capital an investor retains on an after-tax basis.

What determines tax management outcomes?

Index construction

Index construction has two main components: constituent selection and distribution type. Constituent selection refers to an index provider determining which companies get added to an index and when. One provider may be purely rules-based, and another may allow for more discretion over the selection. The difference between these selections means two indexes that track roughly the same market segment can have significant differences. For example, consider a company that experiences tremendous market-cap growth that satisfied the rules for inclusion in the rules-based index much earlier than for the discretionary index. From a tax-management perspective, both scenarios present an opportunity for a DI manager to add value. For portfolios that hold the company longer, deferring unrealized gains can be more valuable. For portfolios where the company is a newer addition, the cost basis can be higher, so loss-harvesting opportunities are more likely to present themselves.

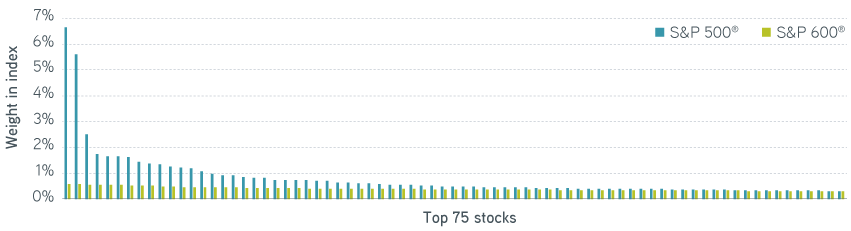

The distribution of an index describes the concentration of weights among its constituents. The figure below compares the weights of the top 75 holdings between an index with a standard distribution, the S&P 500®, and an index with a flat distribution, the S&P 600®. A standard distribution is asymmetric, with a small number of holdings representing a large portion of the index. The holdings of a flat distribution are more evenly distributed.

Figure 1: Distribution of holdings by weight

Source: Refinitiv, 2/28/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index.

The tax-management impacts on portfolios that track flat indexes aren’t universally positive or negative. A flat index distribution means even the top holdings are assigned a small weight relative to a standard-distribution index. As a result, accounts tracking flat indexes tend to hold greater percentages of the constituents to maintain a low tracking error. A greater number of holdings provide more potential loss-harvesting candidates. There is often built in gain realization for indexes constructed of benchmarks with flat distributions. This can be for multiple reasons. In the case of the S&P 600®, the positions that perform the best graduate out of the small-cap benchmark into the mid-cap and large-cap benchmarks. Those positions must be sold at a gain to salute the benchmark changes and maintain small-cap exposure. The S&P 500® Equal Weight Index is rebalanced on a quarterly basis to maintain the target exposure of roughly 20 bps per position. Gain realization is often necessary to maintain the flat distribution.

Consider the benefits of active tax management

Turnover

Turnover measures the percentage of assets bought or sold within a portfolio over a specific period. Indexes periodically buy and sell stocks to maintain consistent market exposure during the index reconstitution, which creates turnover. Appreciated stocks that graduate out are inherently larger in weight than depreciated stocks that fall out for indexes that target a specific market cap. These gains may outweigh the losses on net. New additions to an index tend to be at the lower end of the market-cap spectrum. The index turnover, including new additions, may require gains but it can also refresh the basis of the portfolio and increase future tax management due to new securities with a high-cost basis.

The amount of turnover tends to determine the type of value a DI portfolio adds. Large- and broad-cap indexes, such as the S&P 500® and Russell 3000, tend to have relatively low turnover. Small-cap indexes and equity-style indexes, such as the S&P 600® and the Russell 1000 Value, tend to have turnover that is many times higher. Portfolios tracking low-turnover benchmarks typically have more abundant loss-harvesting opportunities, but gain deferral is a more critical component for portfolios tracking high-turnover benchmarks.

All else equal, we expect tax alpha to be roughly equivalent for low- and high-turnover benchmarks. Whether a benchmark has high or low turnover, realizing losses tends to be the larger component of tax alpha early in the life of an account. Deferring gains tends to become the larger component as the account appreciates.

Volatility

Volatility can present opportunities for tax-loss harvesting throughout the year. Small-cap and emerging-market stocks tend to have higher volatility than large-cap and developed-market stocks. But the timing of volatility is also important: Consider a recently incepted, cash-funded account versus an equivalent account incepted several years prior. The former account will have a higher cost basis and therefore greater potential for loss harvesting once volatility strikes. Even when tax managers harvest losses systematically, a lack of volatility during an account’s early years means subsequent volatility has to be much greater to harvest losses for highly appreciated stocks.

The bottom line

The outcomes of tax management can differ for portfolios that track different indexes, and investors will get different value out of each. So it’s important to understand the circumstances that determine after-tax outcomes. Armed with these rules of thumb, investors can develop realistic after-tax expectations for their chosen benchmarks.

1 For more information, see Shomesh E. Chaudhuri, Terence C. Burnham, and Andrew W. Lo, “An Empirical Evaluation of Tax-Loss-Harvesting Alpha.” Financial Analysts Journal 76:3 (2020): 99–108. This study did not involve Parametric or its clients. There is no guarantee that a tax-management strategy will result in increased after-tax returns. Results will differ based on an individual investor’s circumstances.

“Russell®” and all Russell Index names are trademarks or service marks owned or licensed by Frank Russell Company (“Russell”) and London Stock Exchange Group plc (the “LSE Group”). This strategy is not sponsored or endorsed by Russell or LSE Group, and they make no representations regarding the content of this material. Refer to the specific provider’s website for complete details on all indexes. S&P Dow Jones Indices are a product of S&P Dow Jones Indices LLC (“S&P DJI”) and have been licensed for use. S&P® and S&P 500® are registered trademarks of S&P DJI; Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); S&P DJI, Dow Jones, and their respective affiliates do not sponsor, endorse, sell, or promote the strategy(s) described herein, will not have any liability with respect thereto, and do not have any liability for any errors, omissions, or interruptions of the S&P Dow Jones Indices.