We expect the US economy to remain resilient through the second half of 2026, sustained by AI-driven business investment, ongoing fiscal stimulus and a stable labor market. Downside risks persist—the prolonged conflict with Iran, higher energy prices and uncertainty around Federal Reserve policy—yet strong fundamentals and elevated yields continue to support a constructive outlook for fixed income.

When investors face a wider range of potential market outcomes, active management becomes increasingly important in our view. The flexibility to make decisions about duration, yield curve positioning, credit exposure and security selection may help investors navigate volatility and capture opportunities that passive strategies could miss.

What are we seeing in the current environment?

The US economy has been remarkably resilient despite heightened geopolitical uncertainty and rising interest rates. GDP growth slowed to an annualized rate around 1.6%, supported by business investment and government spending. Persistently higher energy prices and borrowing costs could weigh on consumer spending and economic growth in coming quarters, however.

Inflation running above the Fed's target has reemerged as a key concern for markets. Headline inflation rose to 4.2% year over year in May, while core inflation climbed to 2.9%—the fastest pace in more than three years. Gasoline prices have climbed nearly 40% over the past three months, and the longer inflation remains elevated, the greater the pressure on household budgets and consumer sentiment.

The labor market, however, continues to provide an important source of stability. Recent payroll reports have pointed to improving hiring trends, and the unemployment rate has held steady at 4.3%. Compared to a year ago, labor market conditions appear sufficiently healthy to reduce the urgency for monetary easing, allowing policymakers to focus squarely on inflation risks.

How have fixed income markets responded?

As investors reassessed the prospects for inflation and monetary policy, fixed income yields moved sharply higher during the second quarter. Two-year US Treasurys have repriced more than 60 basis points (bps) year to date as rate-cut expectations have faded considerably. With the market now contemplating that policy may tighten later this year if inflation persists, elevated government debt levels and larger budget deficits have also renewed focus on fiscal sustainability—prompting investors to demand greater compensation for holding longer-maturity Treasurys.

The Fed’s leadership transition adds another layer of uncertainty, with Kevin Warsh becoming the new Chair in a challenging environment of above-target inflation, higher global bond yields and a more hawkish policy backdrop. While advocates argue that AI-related productivity gains could ultimately support stronger growth without inflation, today’s substantial capital expenditures appear more inflationary than disinflationary in the near term.

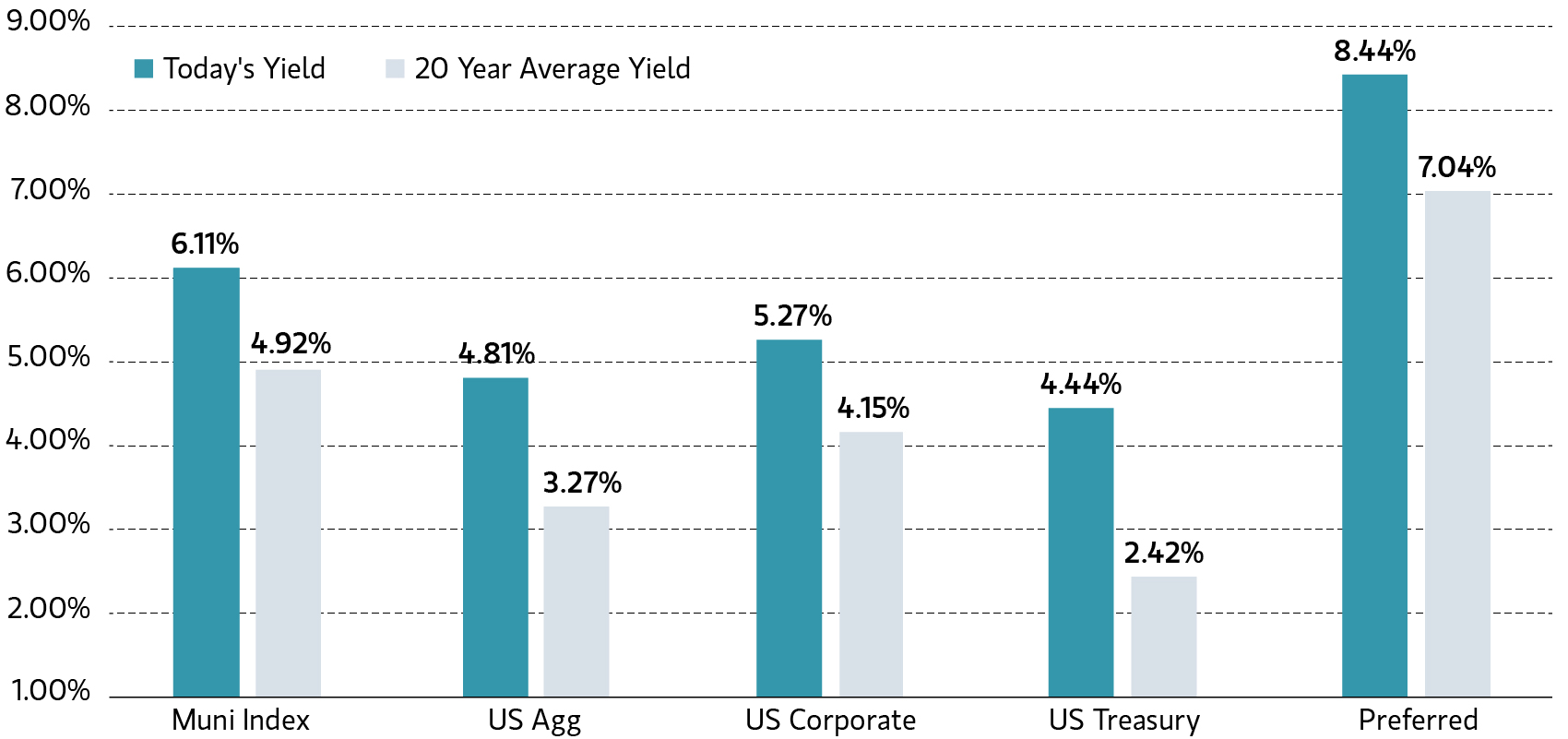

The good news: Yields across most fixed income sectors are near decade highs and above long-term averages

Past performance is not indicative of future results.

Source: Bloomberg, ICE data as of 6/9/2026. Index yield-to-worst for Bloomberg Municipal Bond Index (LMBITR), Bloomberg US Aggregate Index (LBUSTRUU), Bloomberg US Corporate Index (LUACTRUU), Bloomberg US Treasury Index (LUATTRUU) Index, ICE BofA Fixed Rate Preferred Securities Index (P0P1). Muni index yield grossed up to a tax-equivalent yields assuming a 40.8% Federal tax rate. Preferred index yield grossed up to a tax-equivalent yield assuming a 23.8% Federal tax rate. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees and expenses. All investments are subject to risk, including the risk of loss.

Our outlook: Higher yields create opportunity

Higher starting yields have historically been a strong predictor of future fixed income returns and can also provide a cushion against volatility. In our view, today's yield environment strengthens the case for fixed income to play a larger role in diversified portfolios.

Our outlook is that long-term rates should be restrained by the Fed's policy credibility, emerging labor market slack and a slowing pace of global economic activity. We believe high-quality bonds can offer attractive income, return potential and diversification benefits—particularly when equity valuations remain more elevated and macroeconomic outcomes are becoming less certain.

The path forward for markets may depend heavily on developments in the Middle East. The economic impact of the recent oil price shock is likely proportional to the conflict’s duration and severity. Should geopolitical tensions ease, much of the energy-related inflation impulse could gradually fade.

Beyond the current conflict, several structural forces may keep interest rates elevated relative to the past decade. AI-related capital expenditures, fiscal stimulus and persistent deficits could support economic growth while also contributing to higher inflation and term premiums. That’s why we continue to expect a higher and steeper rate environment than investors experienced after the Global Financial Crisis.

If energy markets stabilize, we believe the most likely outcome would be a return to modest expansion, supported by a healthy consumer, a stable labor market, tax cuts and business investment. Corporate fundamentals remain solid, credit spreads are tight and equity markets continue to trade near all-time highs. Taken together, these conditions suggest that monetary policy may not have been meaningfully restrictive before the recent rise in energy prices.

For that reason, we don’t expect the Fed to return to aggressive easing or to shift immediately toward rate hikes. Rather, we think the more probable path may be a patient, data-dependent approach. May’s positive employment surprise underscores the ongoing economic reliance and potential inflationary pressures away from energy. Policymakers need greater confidence that inflation is moving back toward their target before considering additional accommodation.

Solutions for today’s complex interest rate environments

The bottom line

We believe fixed income investors stand to benefit from one of the most attractive yield environments in more than a decade. Macro and policy crosscurrents may create volatility, but elevated yields should provide meaningful income and stronger return potential than during the low-rate era. High-quality municipal bonds and investment-grade corporate credit offer compelling income and diversification benefits if risk assets come under pressure.

In our view, volatility can be a source of opportunity as well as risk. Active management provides the flexibility to adjust duration, reposition along the curve, add credit exposure selectively and identify relative-value opportunities when market conditions change. In an environment of policy uncertainty, geopolitical risk and shifting rate expectations, active fixed income management may become an increasingly important differentiator.

Midyear outlooks for municipal bonds, investment-grade corporates and preferred securities

Municipals

- Bloomberg’s BVAL AAA Muni Yields followed US Treasury yields 15 to 25 bps higher year to date. Yields remain near decade highs and above long-term averages; over the past 10 years, the Bloomberg Municipal Index yield has been above current levels only 10% of the time.

- Tax-exempt yields of 3% to 4.25%—key bogeys for Muni buyers—are driving solid demand. For investors in high tax brackets (assuming a 40.8% Federal tax rate), those equate to tax-adjusted yields of 7% to 9%, offering compelling value compared to other fixed income sectors and equities.

- Muni issuance has maintained a record pace. According to Bloomberg, total issuance hit a record $560 billion in 2025, 30% above the five-year average. Year-to-date through May 31, new issue volume has exceeded $230 billion, up 10% year over year and potentially on pace for another record.

- Despite record issuance, reinvestment capital and strong inflows have supported valuations. In LSEG Lipper Global Fund Flows data through June 5, muni fund inflows have reached $45 billion—the second-strongest start to a year on record. Long-term funds have captured 60% of flows, highlighting the appetite for duration. Strong seasonal reinvestment flows should support the market over the summer.

- The municipal curve is much steeper than the Treasury curve, offering attractive compensation for extending maturities. For investors moving out of cash and preparing for the next stage of the rate cycle, moderate extension along the curve may increase income while helping to mitigate reinvestment risk.

- Municipal credit remains strong. State and local governments have healthy balance sheets, and solid reserves could help absorb Medicaid cuts with limited ratings impact. With spreads stable in a solid economy, upgrades continue to outpace downgrades, though at a slower pace than in recent years.

- Favorable fundamentals, yields near decade highs and meaningful tax advantages should keep tax-exempt bonds a core holding for investors in high tax brackets.

Corporates

- Higher rates have lifted corporate bond yields this year, with intermediate- and longer-duration investment-grade bonds approaching 5%. Resilient fundamentals and attractive all-in yields have supported demand and helped the market absorb heavy issuance. Spreads have narrowed modestly; energy and basic materials have outperformed, while technology and nonbank financials have lagged.

- Capital investment remains the primary driver of issuance. Bloomberg reports that year-to-date US investment-grade supply has reached roughly $1 trillion as of June 9—about 25% ahead of last year's pace. AI infrastructure and data center financing have been major contributors, with hyperscalers issuing more than $100 billion through May 31. Full-year issuance could reach a record as companies fund growth and acquisitions.

- Fundamentals remain supportive. Earnings growth has accelerated across much of the market, and Bloomberg consensus estimates call for S&P 500® earnings growth above 20% this year. Balance sheets remain healthy, leverage is generally stable and rating upgrades continue to outpace downgrades. Within sectors, banks should benefit from improving capital markets activity, while utilities stand to gain from AI-driven electricity demand.

- Geopolitical tensions and higher energy prices may delay Fed rate cuts, but the investment-grade credit backdrop remains constructive. Growth, profitability and investor demand continue to support valuations, even as supply reaches record levels. We expect spreads to remain near historically tight levels, with elevated issuance limiting further compression.

- Income should remain the primary driver of total returns. Current yields are attractive relative to recent history, and yield-oriented demand could support the asset class. Investment-grade corporates remain positioned to deliver attractive risk-adjusted returns, even with a more modest excess-return outlook.

Preferreds

- The ICE BofA Fixed Rate Preferred Securities Index returned 0.36% through May 31. Institutional $1,000 par preferreds outperformed retail $25 par preferreds by more than 100 bps. First-quarter volatility and higher May Treasury yields weighed on retail preferreds, while institutional issues benefited from strong demand and favorable technicals.

- Unlike investment-grade corporates, preferred issuance remains subdued. Bank preferred issuance has slowed materially, resulting in negative net supply year to date. Recent adjustments to regulatory capital requirements have reduced the need for some banks to keep additional tier 1 capital outstanding, limiting new supply and supporting valuations.

- Corporate hybrid issuance has expanded as utilities and other capital-intensive issuers seek efficient funding for infrastructure and power investment. Although spreads have narrowed along with broader credit markets, preferred and hybrid securities still offer more than twice the spread of senior investment-grade corporates, providing a meaningful income advantage.

- Along with attractive valuations, fundamentals are still strong in key preferred sectors, including financials, utilities and energy. Earnings trends are favorable, balance sheets are generally healthy and most preferred issuers remain investment grade.

- We continue to see attractive value in preferred securities for investors focused on after-tax income. Limited net supply, strong demand for income assets and attractive spreads relative to senior corporates should support the market. For taxable investors who benefit from Qualified Dividend Income (QDI) treatment, preferreds can complement traditional fixed income.

Past performance is no guarantee of future results. The returns referred to in the blog are those of representative indexes and are not meant to depict the performance of a specific investment.

Parametric and Morgan Stanley do not provide legal, tax, or accounting advice or services. Clients should consult with their own tax or legal advisor prior to entering into any transaction or strategy described herein.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. All investments are subject to the risk of loss. Diversification does not eliminate the risk of loss. Fixed income securities are subject to the ability of an issuer to make timely principal and interest payments (credit risk), changes in interest rates (interest rate risk), the creditworthiness of the issuer and general market liquidity (market risk). In a rising interest-rate environment, bond prices may fall and may result in periods of volatility and increased portfolio redemptions. In a declining interest-rate environment, the portfolio may generate less income. Longer-term securities may be more sensitive to interest rate changes. Please refer to the Disclosure page on our website for important information about investments and risks.

06.29.2027 | RO 5561006