With an economy exceeding $1.1 trillion and a proven record of conservative budgeting, New York City stands apart as both a global capital and a dependable municipal credit. Let’s look at 10 reasons why we believe NYC’s fiscal health and credit strength may continue.

New York City has weathered every type of economic storm—fiscal crises, recessions, terrorist attacks and a global pandemic. Any one of these could be enough to bring a city to the brink, yet NYC remains a vibrant cultural and economic hub that has attracted human and financial capital to drive the economy and ultimately support its outstanding debt. The city has maintained a rating of at least AA– for nearly two decades, underscoring its resilience through every major downturn. NYC is still one of the highest-rated municipal credits in the country, with General Obligation (GO) bonds rated AA (S&P) and Aa2 (Moody’s) in 2025—reflecting both structural safeguards and exceptional revenue durability.1

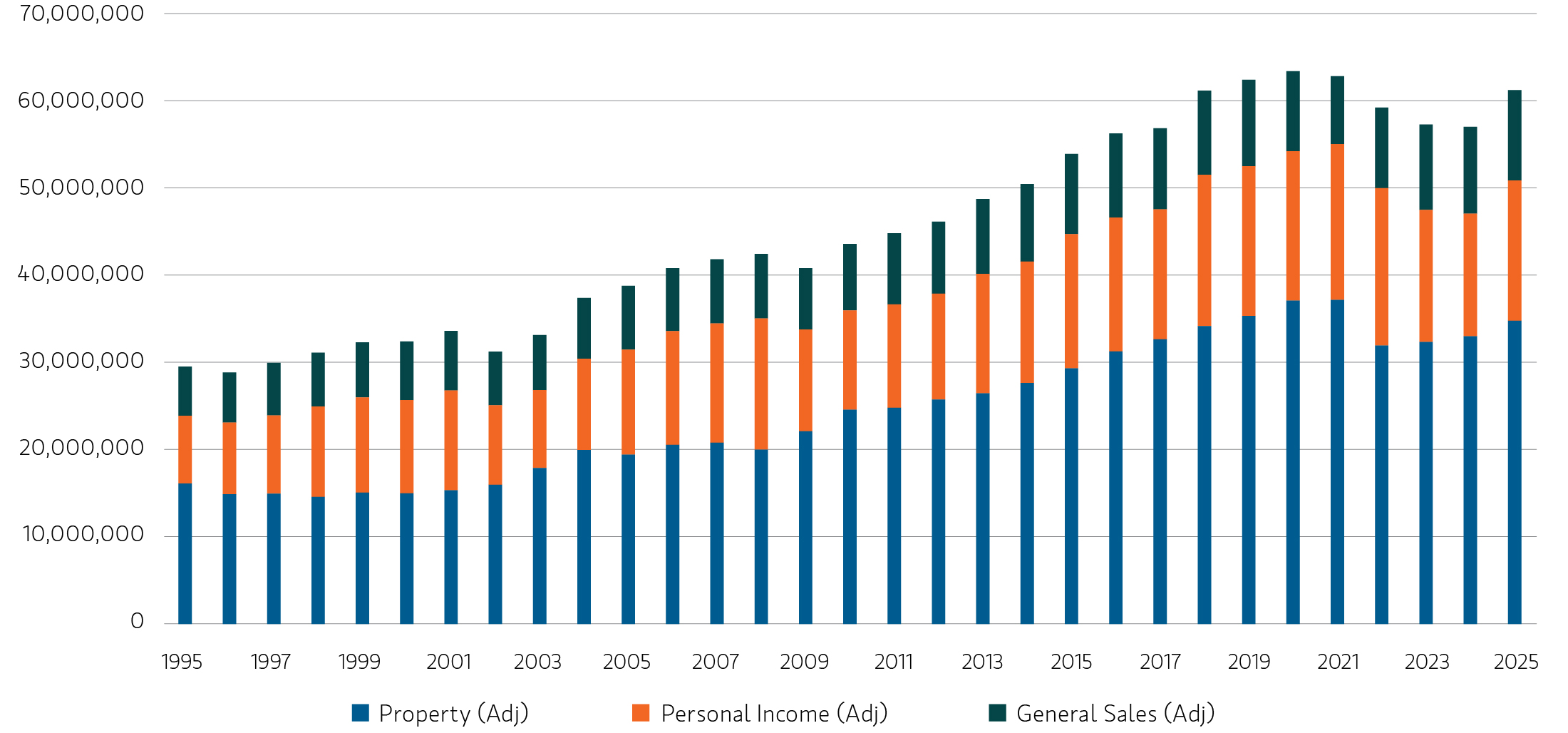

Look no further than the robust levels of tax revenue collected by the city in fiscal year 2025 as evidence. In inflation-adjusted terms, NYC’s tax collections have grown at an average annual rate of 2.5% over the past 30 years. That steady upward trajectory underscores the scale and diversity of the tax base.

NYC Inflation-Adjusted (2024$) Tax Collections ($millions), 1995–2025

Source: NYC Annual Comprehensive Financial Reports (ACFR) as of 06/30/2025. For Illustrative purposes only.

Here are our top 10 reasons why NYC’s fiscal position has remained so resilient for so long.

1. Structurally prioritized debt service is a manageable burden

NYC’s two primary borrowing vehicles, GO bonds and the Transitional Finance Authority (TFA) represent 40% and 48%, respectively of total debt outstanding. Both sources are legally secured:

• GO bonds issued by NYC are repaid from a dedicated General Debt Service Fund, with the city budget legally required to include appropriations for upcoming debt service payments.

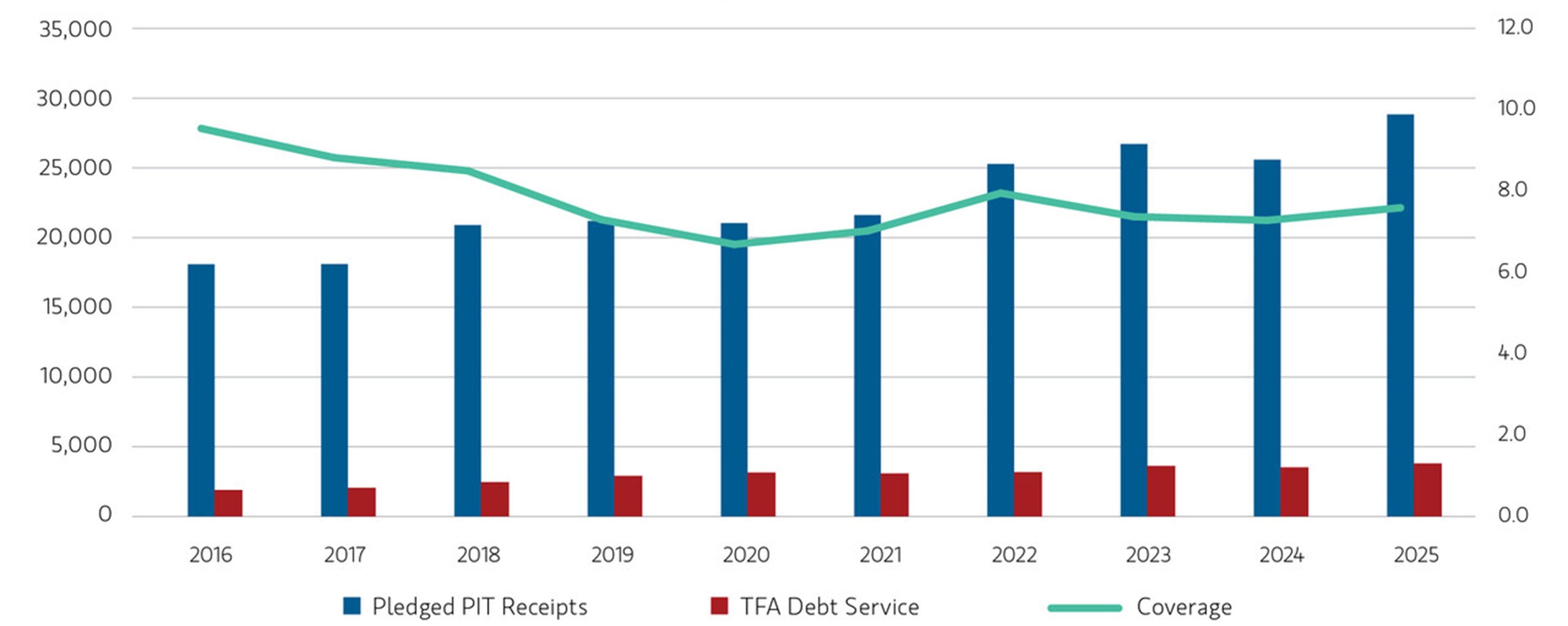

• By law, TFA bonds are secured by state-intercepted NYC personal income tax (PIT) receipts before reaching the city’s General Fund. Coverage on outstanding PIT-secured debt has averaged 7.8 times over the last 10 years.

Transitional Finance Authority Pledged Personal Income Tax Receipts versus TFA Debt Service

Source: NYC Annual Comprehensive Financial Reports (ACFR) as of 06/30/2025. For Illustrative purposes only.

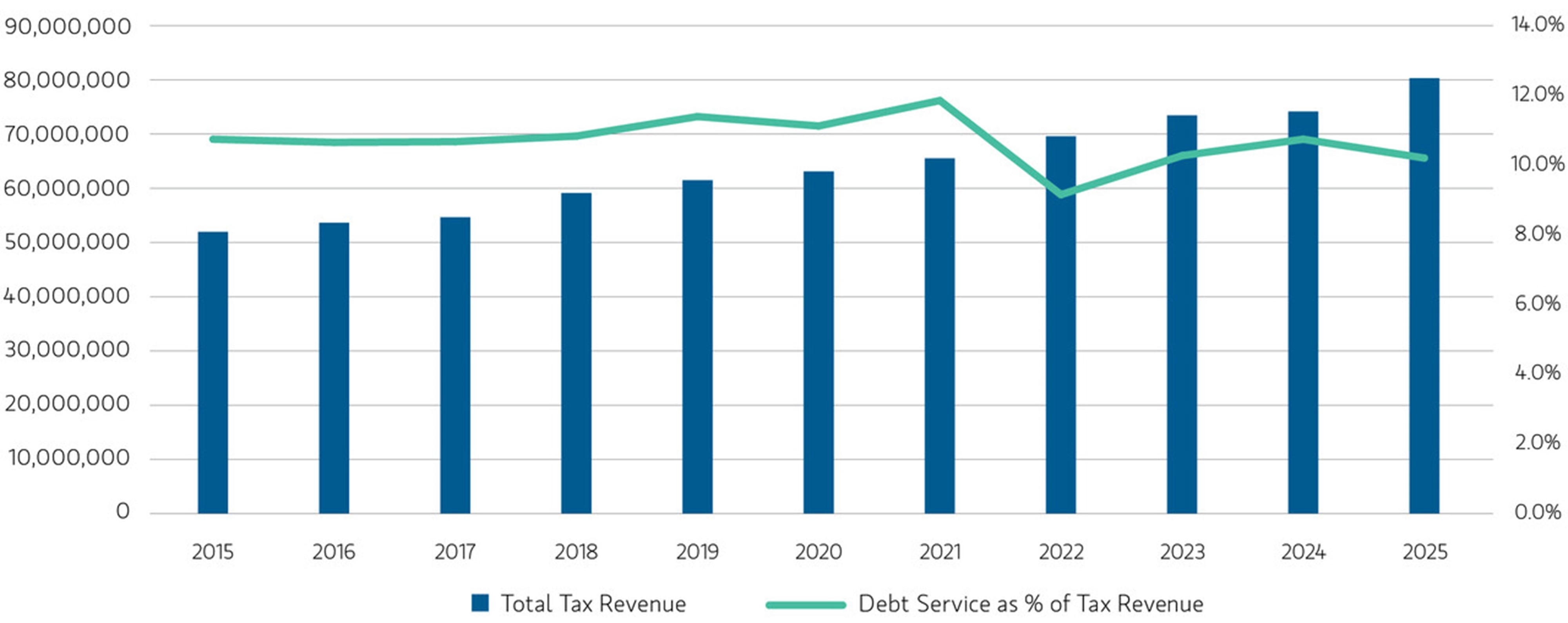

Total debt service payments represent a manageable 10.6% of tax revenues.

Transitional Finance Authority and General Obligation Debt Service as a Share of Tax Revenue

Source: NYC Annual Comprehensive Financial Reports (ACFR) as of 06/30/2025. For Illustrative purposes only.

Total debt service payments represent a manageable 10.6% of tax revenues.

2. NYC has a balanced budget requirement

By law, NYC must pass and maintain a generally accepted accounting principles (GAAP)-balanced budget annually, which forces any mismatches of expected revenue and expenses to be reconciled and addressed.

The city is also required every year to prepare a four-year financial plan, mandating responsible long-term financial planning and conservative budgeting.

3. The mayor has no unilateral authority to increase taxes

By city law, tax changes to alter income, sales or corporate tax rates require state authorization. This structure limits policy volatility and helps maintain predictable tax and credit conditions for residents and businesses.

In 2014, for example, Mayor Bill de Blasio’s proposal to raise PIT on high earners to fund universal pre-K was rejected by Albany.

4. Debt limits are constitutional

Deficit spending is legally prohibited under the Financial Emergency Act, as is overleveraging the city by issuing additional debt.

GO debt is capped at 10% of NYC’s five-year average property value. TFA debt is similarly capped by statute and subject to state review and approval. These caps ensure debt growth remains in line with underlying asset values and tax capacity.

5. New York state provides oversight via the Financial Control Board

The Financial Control Board (FCB) was created after the 1975 fiscal crisis to oversee NYC’s finances, providing the state with legal authority to reassert control over the city’s finances before serious credit concerns arise.

Although largely dormant today, the FCB retains legal authority to reassert control if NYC fails to pay debt service, ends a year with a GAAP deficit greater than $100 million or deviates from its four-year financial plan.

6. Federal funding is formula-driven

NYC receives roughly $8 billion to $10 billion in federal aid annually, representing 6% to 9% of the city’s budget. Most of this funding for education, housing and healthcare is formula-driven, so it cannot be cut unilaterally by the executive branch.

Past attempts to defund cities—such as 2017’s sanctuary-city orders—were blocked by federal courts for exceeding executive authority.

Discretionary Federal funding for large-scale capital projects such as the Gateway Tunnel and the 2nd Avenue Subway extension can be (and have been) delayed with minimal credit impact.

7. New York state needs NYC to succeed

NYC accounts for roughly 46% of New York state’s $2.3 trillion gross domestic product (GDP), or about $1.05 trillion in annual output. The city contributes about 45% of all state PIT collections—the state’s single largest revenue source.

Recognizing that a financially stable NYC is critical to the state’s fiscal health and credit profile, the state government in Albany has a proven record of supporting NYC during periods of stress.

8. Commercial real estate has been resilient

Post-pandemic fears of a permanent office exodus were overstated. Major firms appear to be doubling down on NYC, with JPMorgan Chase & Co recently opening a new $3 billion headquarters. Showing clear signs of recovery, office leasing activity reached 11.4 million square feet in early 2025 according to Colliers—the highest since 2019. And CRE Daily reported that NYC office foot traffic in July 2025 was 1.3% higher than in July 2019.

9. Tourism and tax revenues are recovering

Tourism, one of NYC’s largest economic drivers, has rebounded sharply since the pandemic. The city welcomed about 61 million visitors in 2024—roughly 95% of 2019’s record levels. Upcoming global events, including the 2026 World Cup, are expected to further boost tourism and economic activity.

Sales tax receipts climbed to $9.3 billion, up 8% year over year and nearly 20% above FY 2019 levels. Wall Street profits exceeded $60 billion in FY 2025, driving finance-related taxes of roughly $6.7 billion—about 8% of NYC’s total tax revenue.

10. The property tax base is strong

City-wide property values have more than recovered from pre-pandemic levels, rising to $1.49 trillion in 2025 from $1.37 trillion in 2021. Property tax comprises 45% of local tax revenue and is not capped under New York state law.

Assessed value has risen from $267.7 billion in FY 2019 to $315 billion in FY 2025, supporting long-term revenue growth.

Residential demand remains robust, with rents continuing to rise. Manhattan’s median rent now averages around $4,500, up from roughly $3,000 in 2019.

The bottom line

By many measures, New York City’s finances in 2025 are stable, and the economy is healthy. NYC continues to attract global interest and investment from individuals and firms, which in turn generate tax dollars to fund its operations and service its debt. We believe the legal protections safeguarding NYC’s fiscal and debt management policies reinforce its standing as not only a resilient city, but also a resilient credit.

A version of this Insight, Top 10 Reasons Why New York City's Credit Strength Has Endured, was published by Eaton Vance on Nov 6, 2025. Co-author Colin Shaw, CFA is a member of the Municipals team, one of the largest municipal bond-focused teams in the industry.

1 Ratings represent the opinions of the rating agency as to the quality of the securities they rate. Ratings are relative and subjective and are not absolute standards of quality. The portfolio’s credit quality does not remove market risk.

All data sourced from the New York City Independent Budget Office, the Offices of New York City and State Comptrollers, and the New York State Departments of State, Taxation and Finance, unless otherwise noted.

Parametric and Morgan Stanley do not provide legal, tax or accounting advice or services. Clients should consult with their own tax or legal advisor prior to entering into any transaction or strategy.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

11.30.2026 | RO 4965663