From financials to IT, the way we sort equities into sectors is changing. Investors seeking diversification will welcome the shift—as long as they’re not too concentrated already. We show how rebalancing now can help investors’ risk profiles later this year.

As the calendar flips to spring, many of us experience the overwhelming urge to clean and organize the seemingly chaotic areas of our lives to introduce a more calm, harmonic balance. In that spirit, the firms overseeing the Global Industry Classification Standard (GICS) have channeled their inner Marie Kondo this year to declutter and better categorize a significant swath of equities. We don’t expect the next evolution to grab as many headlines as 2018’s addition of the communication services sector. But the official changes implemented on March 17, 2023, are worth discussing for their potential impact on all equity investors.

What is GICS, and how is it changing?

Way back when Prince’s legendary track “1999” was in high rotation, industry power players S&P and MSCI created the GICS framework, which organizes equities into a series of broad (sector) and narrow (subindustry) classifications. Virtually all market participants—including investors, institutions, analysts, and the financial media—have used GICS ever since. Besides the obvious benefit of categorization, these standards helped spawn a cottage industry of sector-specific investment vehicles that have only grown in size and importance. As an example, sector ETFs from the four largest US providers had a collective AUM exceeding $425B as of January 31, 2023, not an insignificant sum and highly GICS-dependent.

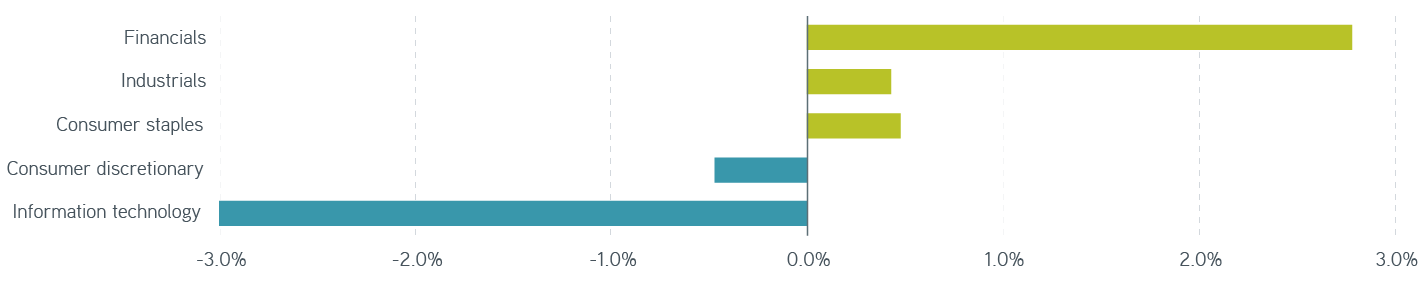

Before this year’s changes, the GICS structure comprised 11 sectors, 69 industries, and 158 subindustries. The most recent updates add five industries and five subindustries, which probably doesn’t sound very extensive considering the previous lengths of those lists. However, the changing weights of certain S&P 500® constituents tell a different story. Just under 10% of the index’s total market cap is pulling a George Jefferson and movin’ on up, as you can see in the below chart. A collective change of this magnitude will undoubtedly cause a ripple effect across passive and active equity investing.

S&P 500® sector weighting change

Sources: Parametric, FactSet, 1/31/2023. For illustrative purposes only. It is not possible to invest directly in an index.

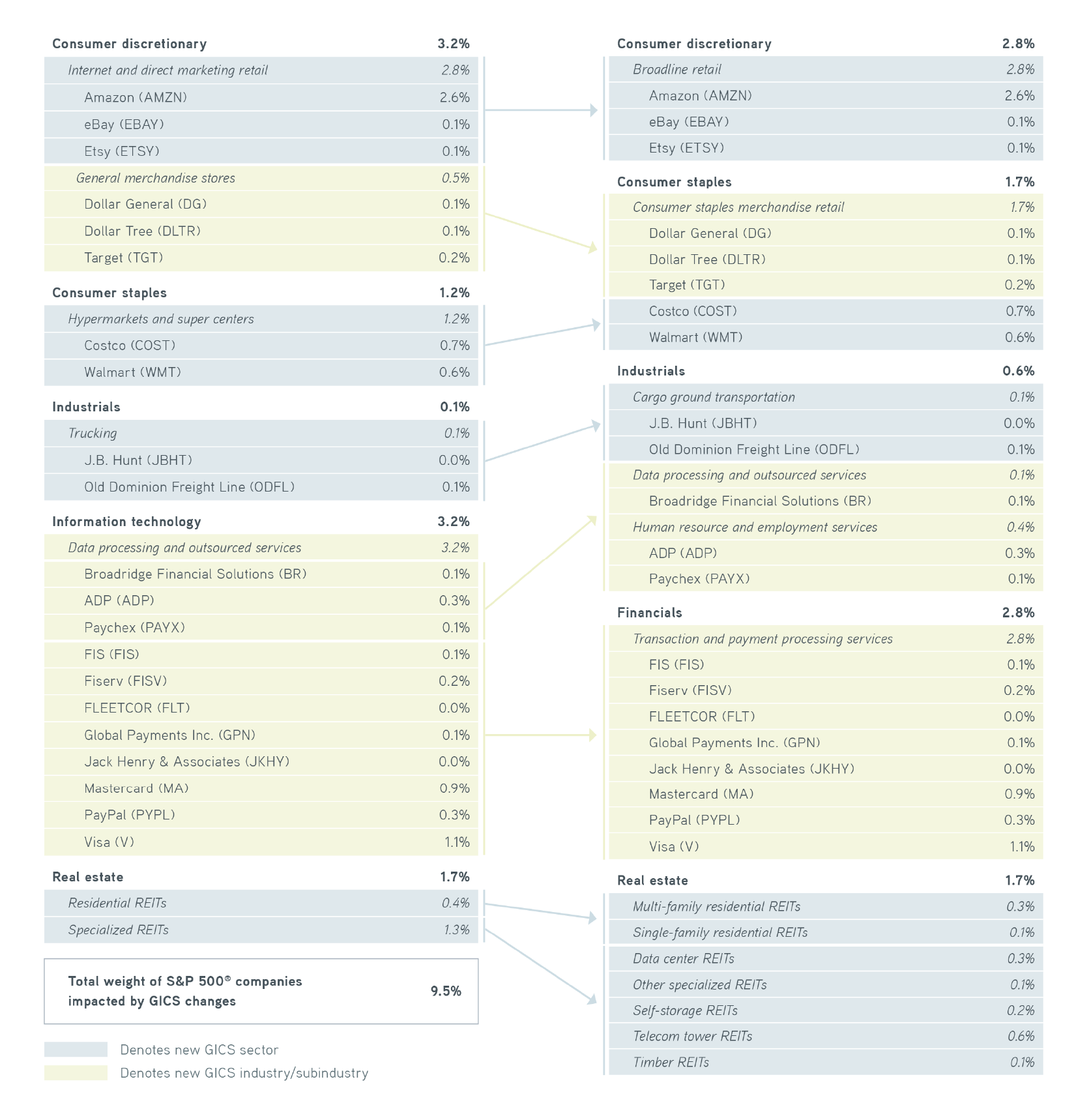

Investors may be surprised to discover some notable firms changing sectors. We start again with the migration of 5% of the stocks in the consumer discretionary sector to consumer staples. Target (TGT), Dollar Tree (DLTR), and Dollar General (DG) are headed to the newly created consumer staples merchandise retail subindustry. More than anything else, legacy may have contributed to those three companies residing within discretionary. Target was once the discount arm of department store conglomerate Dayton-Hudson, making it a reasonable fit in the previous sector. Before it acquired Family Dollar, Dollar Tree generated a majority of revenue from variety and seasonal items rather than the food and consumables categories that proliferate within staples. Dollar General has spent the past decade or more becoming the de facto grocery and general store for thousands of small communities across the country, essentially filling the gaps between Walmart locations. The flyover-country factor is certainly prevalent in this delayed but long-deserved sector shift.

Among the 12% of stocks moving out of the information technology sector, the common theme is hands-on involvement with money. From financial services and payroll to credit card processing and payments, the companies are intimately ingrained in the process of money movement. The two largest worldwide payment networks, Visa (V) and Mastercard (MA), plus their peer-to-peer cousin PayPal (PYPL), are among the most notable movers. Lesser known but also important are companies that issue credit cards and facilitate the backbone of e-commerce and banking, such as FIS (FIS), Fiserv (FISV), and Global Payments Inc. (GPN). As a result, the massive IT sector shrinks and becomes slightly less diversified. In contrast, the financial sector becomes a better representation of the entire ecosystem rather than just a heavy concentration of banks and insurers.

Get diversified and durable dividends

Equities changing GICS sectors in 2023

Sources: Parametric, FactSet, 1/31/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index.

How should investors respond to GICS changes?

Equity investors holding individual securities or concentrated portfolios will likely experience increased volatility levels from the involved stocks, especially those changing sectors. For example, a cursory review of the 2018 GICS changes indicated that many stocks in the new communications services sector—including Verizon (VZ), AT&T (T), Electronic Arts (EA), and Alphabet (GOOGL)—saw unseasonably high volatility in a relatively narrow window around the official change date. We know index-tracking vehicles like ETFs and open-ended mutual funds employed a transition period rather than ripping off the Band-Aid, and we can only assume prudent active managers used similar strategies.

Contrarily, event-driven market movement and idiosyncratic risk are severely blunted for investors in direct indexing and systematic solutions, which eschew many of the pitfalls of concentrated holdings. The irony of these recent changes isn’t the typical reactionary response of an asset manager. GICS has become more diverse by reducing sector concentration, notably in information technology. Net-net, the industry is moving ever closer to Parametric than the other way around.

The bottom line

Many investors will likely see little impact on their portfolios from 2023’s GICS changes. However, those with concentrated positions in the above stocks or holders of sector-specific investment vehicles might experience near-term price volatility as institutional asset managers rebalance portfolios that track newly weighted passive benchmarks. GICS sectors, industries, and subindustries are now better representatives of their underlying constituents and slightly less concentrated than the previous iteration. This means these changes should be a welcome development for investors seeking to build diversified portfolios.

References to specific securities and their issuers are for illustrative purposes only and are not intended to be and should not be interpreted as a recommendation to purchase or sell such securities. Any specific securities mentioned are not representative of all securities purchased, sold, or recommended for advisory clients. Actual portfolio holdings vary for each client, and there is no guarantee that a particular client’s account will hold any or all of the securities identified. It should not be assumed that any of the securities or recommendations made in the future will be profitable or will equal the performance of the listed securities.