Every year offers important lessons for investors if they’re paying attention. How can 2022 help us plan for the year ahead?

In what world could annual returns of -19.5% in the equity market (CRSP Total Market) and -25.6% in the fixed income market (Bloomberg Barclays Long Corporate) be considered a success? The answer is the US corporate pension world in 2022. Pension outcomes are better measured by surplus and funded status values and funding ratios than they are by absolute returns. That’s why most pension plans invest their assets in an effort to reduce funding shortfalls while avoiding overall surplus risk. Liability returns in 2022 were even more negative than the asset portfolios supporting them. Funding ratios were therefore higher at the end of 2022 than they were at the beginning, and funded status has improved. From a pension investor’s perspective, plan sponsors should be happy.

Over the course of any year, the beginning and ending values seldom tell the entire story, and so it went with 2022. There’s usually a lesson along the way that all too often gets lost in the shuffle or completely ignored. The lessons of 2022 have been slow to develop and relatively mild. It was a fairly steady progression toward higher funding levels through October, only slightly faltering in June and July. Rates just kept increasing, along with Fed increases in interest rate targets, inflation, and quantitative tightening, among other things, while widening credit spreads increased discount yields further. From early November to early December, however, discount yields lost 60 to 80 basis points (bps) from their 2022 increase, significantly reducing funded status and funding ratios. The lesson is that yields can shift back and gains can be lost. Yields did increase again over the remainder of the year, but they didn’t return to the levels of late October and early November. It’s nearly impossible to time the exact moment to lock in winnings, so taking available winnings is still worthwhile. Removing interest rate risk while being well funded is a prudent strategy.

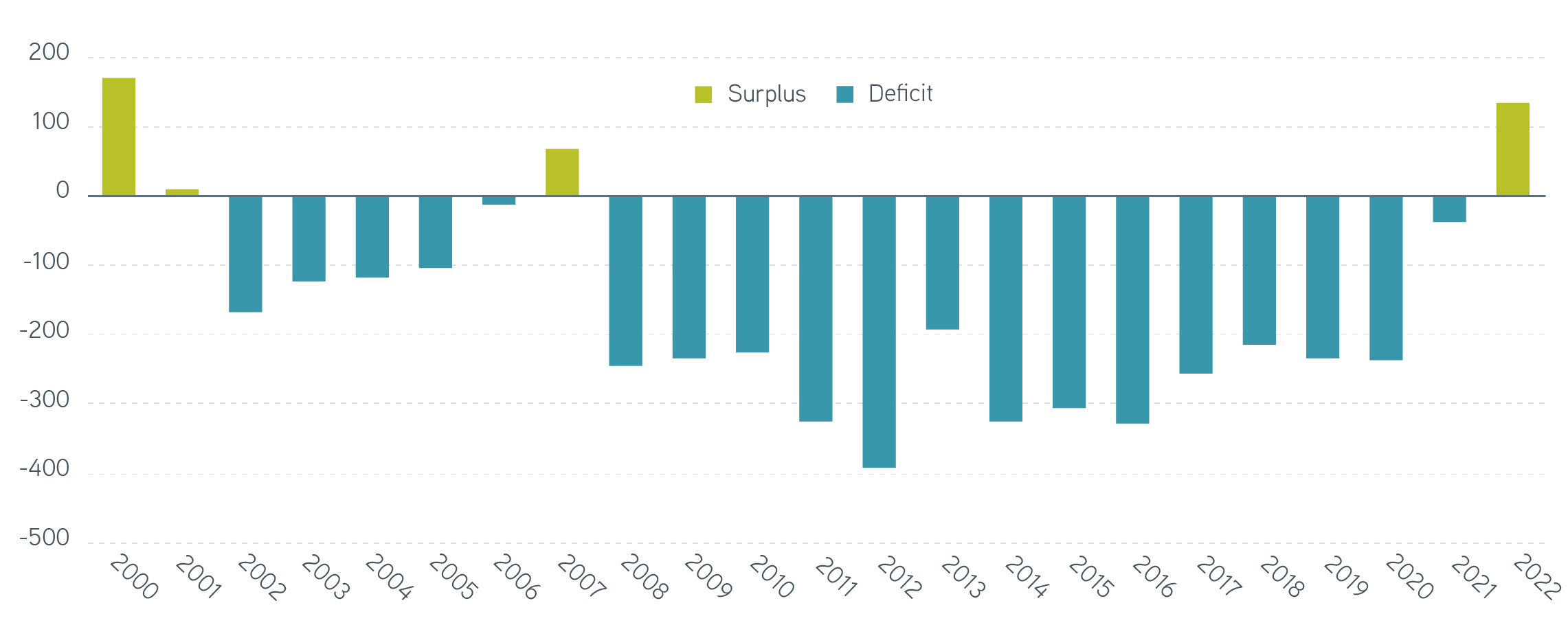

The Milliman 100 Pension Funding Index updated for December 2022 shows funded status and funded ratio at the end of 2021 as -38,572 and 97.9%, respectively. Through early December, those values improved to 133,418 and 110%.

Milliman 100 Pension Funding Index pension funded status

Source: Milliman, 12/7/2022. For illustrative purposes only. Past performance is not an indicator of future results. It is not possible to invest directly in an index.

Other lessons to be learned

The United Kingdom provided another lesson in late September. Gilt yields climbed in a seemingly unstoppable manner, driven by previously unforeseen circumstances. The UK government unveiled an unexpected economic policy framework on September 23, bringing such a sudden shock to the gilts curve that pensions found themselves stranded in a harmful feedback loop. Increasing gilt yields created margin calls, but this time there weren’t enough liquid assets available, leading to forced sales of gilts and fueling ever-increasing yields.

The cruel irony of this situation is that while pension liquidity was rapidly deteriorating, funded ratios may have been improving. By September 28 the Bank of England had to step in to buy gilts, in a move contrary to its quantitative tightening program, in order to stabilize markets and save pensions. In matter of a few days, 30-year gilt yields experienced a round trip of over 100 bps.

While the circumstances around that crisis can’t really happen in the United States, it still offers a lesson for constructing a plan to maintain sufficient liquidity to support a pension investment strategy if one isn’t already in place. Everyone benefits from understanding what exposures might exist in a total plan investment strategy.

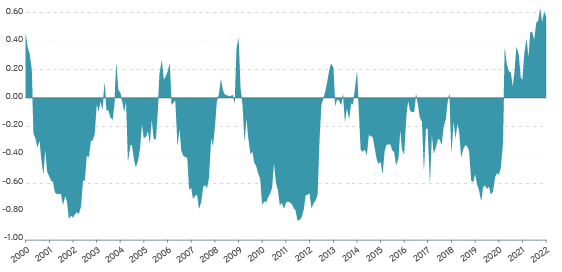

One last lesson is that diversification isn’t guaranteed. 2022 could have been an even better year for pensions had equities not performed as horribly as bonds. It also could have been a disaster if yields had not risen and equity returns hammered funding ratios. Of course, conditions like inflation and market volatility changed the correlation between equities and bonds, but they certainly were more positive than we’ve seen in years. Will that relationship hold going forward? Not forever, because correlations are distributional rather than static. There’s a benefit to removing unnecessary risks, particularly if plan funding has recently improved significantly. Improved funding reduces total funded status risk, and the plan becomes primed to benefit from asset classes that are less expensive than they were a year ago.

Twelve-month stock-bond correlation, 2000 through 2022

Source: Morningstar Direct, 9/2/2022. For illustrative purposes only. Not a recommendation to buy or sell any security.

The bottom line

Going forward, we’re once again faced with uncertainty. Our 2023 Investment Outlook outlines where the economy and markets might be headed. From an LDI perspective, in this environment, it’s important to have learned the market’s lessons and to implement total plan strategies. Those strategies should aim to reduce or eliminate unnecessary risks like those associated with interest rate movements while accepting appropriate expected levels of risk to close any remaining funding gaps. It’s equally important to accept funding-level gains and adjust to the new reality of a well-funded plan, so that future market uncertainty will have less impact on plan outcomes.

Ensure the right balance in pension plan funding