Backwardation and contango have captured the imagination of commodity investors, but we caution against overreacting to either condition. Let’s pull the thread and see what we unravel.

Commodity prices around the world have sagged recently, a reflection of reduced concern over Russian-influenced supply disruptions and growing concern that the global economy is headed for the gutters. That’s a stark contrast from earlier this year, when tight supplies of everything from oil to grains and metals sent raw-material prices to new records while also pushing markets into backwardation, a phenomenon where near-term supplies fetch a premium. With the commodity price rally cooling, we may quickly be approaching the opposite state, the dreaded contango.

Commodity investors frequently ask what impact backwardation or contango has on the return prospects of a commodity allocation. Indeed, perhaps no part of commodity investing causes more confusion or is more controversial than the causes and impacts of term structure on a commodity portfolio. Investors often believe that commodities will produce positive returns only if forward prices are downward sloping. To shed light on this misunderstood part of the commodity market, let’s first look at what it means to be in either backwardation or contango; then we’ll examine their impact on potential returns.

What is the term structure of futures?

Put simply, the price of a futures contract differs depending on the expiration date, similar to the yield curve observed in interest rates. Many factors determine the term structure of a commodity future’s price, such as supply-and-demand dynamics, storage costs, and even interest rates. A commodity whose futures price increases as time to maturity increases is in contango, while one whose prices decrease is in backwardation.

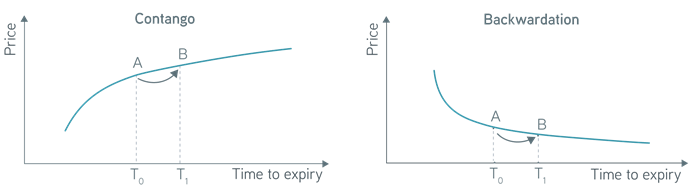

Contango and backwardation in commodities

Source: Parametric, 9/20/2022. For illustrative purposes only.

When investing in commodity futures, investors must roll the position—selling the maturing contract and buying a further-dated contract, shown by the curved arrows in the chart—before maturity to prevent taking delivery of the underlying commodity, which might be, for example, 5,000 bushels of corn or 1,000 barrels of oil. When an investor rolls the position, the term structure generates either a drag or boost to returns relative to the spot-price change alone. A forward curve in contango leads to a drag on returns for a futures investment compared to the spot price, whereas one in backwardation leads to a boost. Although we contend that the losses attributed to contango simply reflect costs avoided by not physically owning the commodity, many investors see this friction as something to avoid or minimize at all costs. Some investors avoid owning the asset class when forward prices are sloping upward, believing prices go up only when the market is in short supply of the physical material, as signaled by backwardation. We find little evidence to support such a drastic claim, however. The current level of contango or backwardation has historically been a poor predictor of future performance.

Does contango always mean negative returns?

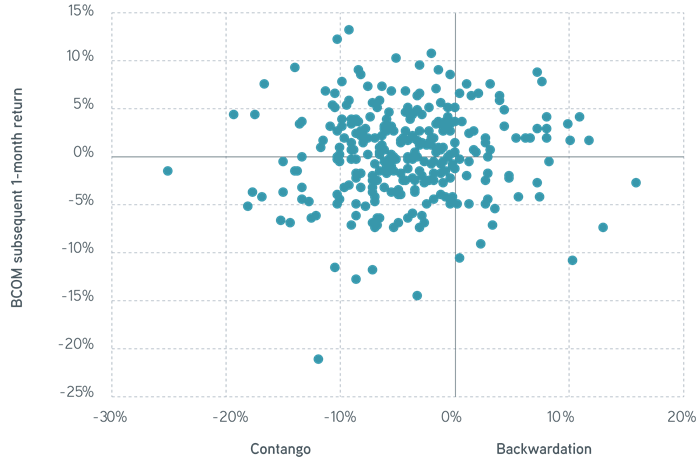

In reviewing data for the Bloomberg Commodity Index (BCOM) going back to 1997, we find no relationship that ties the average level of contango or backwardation among commodities—as measured by the annualized difference between the nearest-to-mature futures contract and the contract the index holds in one month—to how the index performed over the subsequent month.

Our Commodity Strategy can help defend against inflation

Average level of contango/backwardation vs. subsequent one-month return, October 1997–August 2022

Sources: Parametric, Bloomberg, 9/20/2022. For illustrative purposes only. Past performance is not indicative of future results. It is not possible to invest directly in an index.

If conventional wisdom was correct and commodities only produced a positive return in backwardation or a negative return in contango, we’d expect to see a linear pattern starting at the lower left and moving to the upper right. Historical return patterns simply don’t support this notion. In fact, given the market’s average state ahead of time, outcomes seem rather random. BCOM rallied following a contango reading 51% of the time, but 49% of the time it didn’t.

Understanding why is mostly straightforward. In general, the price of a commodity tends to rise when demand exceeds current supply. If demand remains robust and supply insufficient, prices will rise high enough to cause the forward curve to move into backwardation. To investors, this is a strong signal of a deficit in the physical market, which could mean prices continue to rise alongside demand or that prices fall as new supply becomes available. Timing these calls consistently is challenging, and relying on any signaling from contango or backwardation historically hasn’t given investors a leg up. Moreover, it could’ve meant they missed out on the holy grail in commodity investing: a supercycle, abnormally strong demand growth followed by a lengthy rally in prices. Commodity supercycles include periods of both contango and backwardation.

Riding the supercycle

Commodity markets tend to go through extended periods of boom and bust, with prices often moving significantly above or below their long-term trends. These periods can even outlive the business cycle and at times will persist for a decade or longer. The most recent supercycle lasted from roughly the late 1990s through the Global Financial Crisis. Rapid economic growth in China, India, and other emerging-market economies drove strong demand for raw materials and a subsequent broad-based rally in commodity prices.

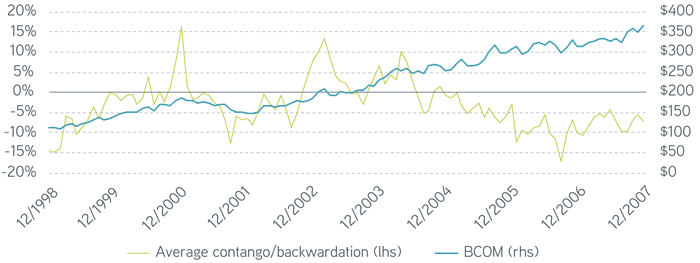

Between 1999 and 2007, returns for BCOM averaged 15% per year, but the index was in contango three-quarters of that time, as shown in the following chart. Nearly all of the last four years in this chart show commodities trading in contango, but index returns still averaged 12% per year. A portfolio that actively traded on these signals, buying when the market moved into backwardation and selling in contango, would’ve underperformed a static allocation by more than 8% per year.

BCOM price and level of contango (-) or backwardation (+), January 1999–December 2007

Sources: Bloomberg, Parametric, 9/20/2022. For illustrative purposes only. Past performance is not indicative of future results. It is not possible to invest directly in an index.

It’s striking how similar that period looks to today. Following a strong run-up in prices and a market that moved into heavy backwardation (1999 to 2000), prices pulled back in 2001, coinciding with a recession in the US during the spring. Demand for raw materials contracted, leading to excess supply and a market that moved into contango. Prices then rebounded and continued to move higher for the next six years. It’s possible that today, like the beginning of that period, we’re in the early stages of the next supercycle in commodities. If so, a potential near-term recession will have little success in derailing the long-term trend.

The bottom line

Though backwardation and contango have captured the imagination of many participants in the asset class, diversified commodity investors would do well to worry less about reacting to either condition. While an upward-sloping forward curve can be a drag on returns, future performance is inherently challenging to predict and not telegraphed by the level of contango or backwardation in the commodities market. Even periods of long-term growth for the asset class have come when contango was the normal condition of the market. Given the long-term benefits the asset class can provide, such as inflation protection and portfolio diversification, we believe adhering to a modest strategic allocation is the right approach.