Most investors still rely on one measure of inflation—but the Federal Reserve has spent the past decade using another. In a year marked by runaway price pressure, this difference matters.

Inflation is at the top of all investors’ minds these days. It spurs fears of currency devaluation, sharply rising interest rates, and drained liquidity through quantitative tightening. Concern about runaway inflation—the opposite of transitory inflation—is driving Federal Reserve officials to discuss openly how aggressive they’ll be in transitioning to a restrictive monetary policy, starting with next month’s Federal Open Market Committee (FOMC) meeting. Markets are already ahead of the Fed, pricing in six 25-basis-point (bps) rate hikes in 2022.

The best way to measure inflation is an interesting question to consider as we prepare to spend the balance of the year fighting it. There are two standard measures of inflation in the US: the Consumer Price Index (CPI) and the Personal Consumption Expenditures price index (PCE), both of which are updated monthly. The Bureau of Labor Statistics (BLS) produces the CPI, while the Bureau of Economic Analysis (BEA) publishes the PCE.

Most of us are familiar with the CPI as the headline measure of inflation. It’s the index used to adjust Social Security payments, and it acts as the reference rate on financial instruments like Treasury Inflation-Protected Securities (TIPS). However, at the January 2012 FOMC meeting, the Fed declared it would use the PCE as its primary measure of inflation, viewing it as a more accurate gauge of price pressure across the broad economy. This is important because these indexes are calculated differently, therefore yielding different measures of inflation.

Create a flexible, personalized portfolio for your clients

The change in the price of both indexes reflects the change in the price of a basket of goods and services. If the price of the basket goes up, the index goes up. The primary difference between the two indexes is that the baskets are not the same. The differences can be broken down into three major categories:

- Weight: The weight effect results from sourcing consumer expenditure data, such as basket price data, from different surveys. Expenditures in the PCE come from the BEA’s National Income and Product Accounts (NIPA) tables, which measure what businesses sell to consumers. CPI expenditures are sourced from the BLS’s Consumer Expenditure Survey, a combination of two surveys measuring what consumers buy from businesses.

- Scope: The scope effect results from the differing definitions of what the two indexes measure. The CPI considers only the urban population and out-of-pocket consumer expenditures. The PCE considers both urban and rural populations and includes all expenditures purchased on behalf of consumers, even by a third party such as an employer. For example, the CPI doesn’t include health insurance provided by an employer or through Medicare or Medicaid, but the PCE does.

- Formula: Categories with wide price swings, like gasoline, are more likely to impact the CPI. The PCE formula smooths out these price swings by assuming consumers will purchase less of a good or service if its price rises sharply relative to other goods and services in the basket. The CPI doesn’t allow for this type of substitution effect.

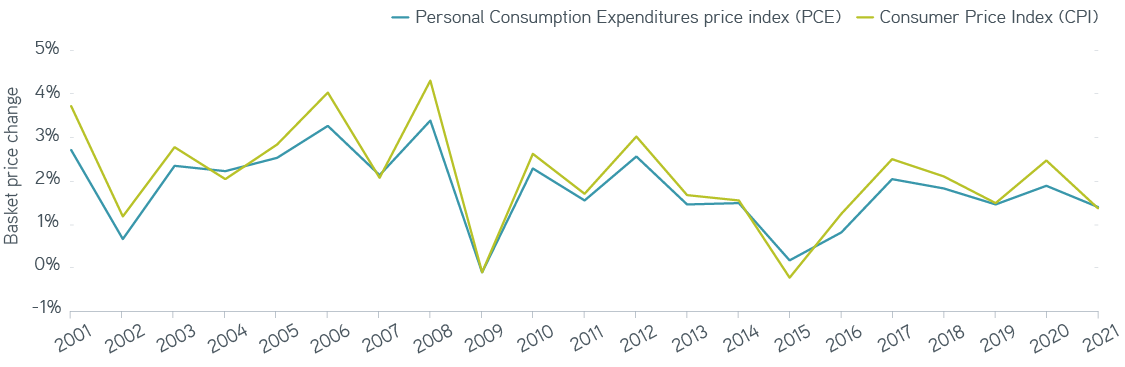

Year-over-year CPI vs. PCE

Source: FRED, Federal Reserve Bank of St. Louis. For illustrative purposes only. It is not possible to invest directly in an index.

So what’s the net outcome of all these differences? The PCE is generally less volatile than the CPI, registering more moderate price changes on the upside and downside. Over the last six months, as prices have risen sharply, the PCE has produced a year-over-year inflation estimate that’s 1.1% lower than the CPI on average.

The PCE may have the seal of approval from the Fed, but most observers still focus on the CPI. We can all look forward to many more conversations around inflation in 2022. But before engaging in those conversations, we should make sure all parties agree on how inflation is measured.