The next commodity supercycle could be bigger than any one country—even the world’s largest commodity buyer. There’s been more to the market over time and across the globe. Find out China’s true influence and what might drive the next stage of price growth for the asset class.

Commodity investors entered 2023 in an optimistic mood. China, the world’s largest consumer of most commodities, had just jettisoned its so-called zero-COVID policy, which was severely hampering its economy, and was back open for business. This would surely boost commodity demand at a time when supply of many key commodities remained tight. Unfortunately, China’s recovery has thus far progressed unevenly. On one hand, China’s economy expanded 4.5% in the first quarter versus a year ago, following an initial burst of activity. But momentum has slowed recently as retail sales, industrial output, and property investment have all come under pressure. The country’s official manufacturing PMI, a gauge of factory activity among large state-owned firms, slid to a five-month low of 48.8 in May, indicating contraction. Indeed, weakness in the Bloomberg Commodity Index results this year at least partially reflect investor concerns around Chinese growth.

Without a doubt, what happens in China can reverberate through global commodity markets. But a longer-term view of this relationship reveals that this narrative has really only been true more recently. Commodity prices respond to many different supply and demand conditions. We see good reasons to believe that even without a strong Chinese recovery, the global transition to a greener economy should give investors optimism about the asset class.

What impact does China have on the global commodities market?

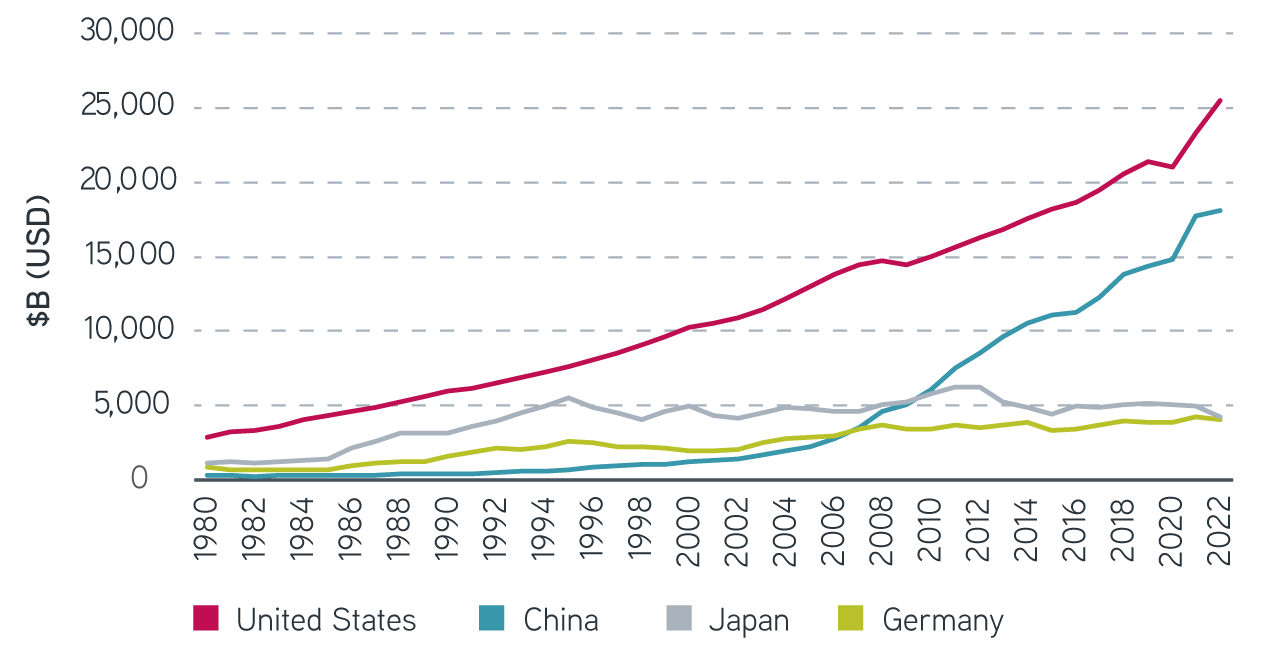

It’s hard to downplay China’s importance in influencing commodity prices over the past 20 years. At the start of this century, China’s GDP was less than an eighth of that of the United States, according to the IMF. Today it sits at over 70%, making China the world’s second-largest economy. China’s fast-paced assent was powered by massive amounts of spending on infrastructure projects, driving demand for concrete, metals, and almost every energy product imaginable. China became an influential commodity buyer and was a main source of the strong performance the asset class enjoyed from 2000 through the 2008 global financial crisis (GFC). This coincided with some of the first academic papers on the asset class, many arguing for the important value commodities can add to a portfolio, such as inflation protection and diversification.

GDP at current prices, 1980–2022

Source: IMF, 4/11/2023. For illustrative purposes only. Not a recommendation to buy or sell any security.

But the timing could not have been more unfortunate, in a way. For most investors, the China story has synced neatly with their own experience. Broad commodities provided an annualized return of 17% from the beginning of 2000 through their peak in 2008, while China’s economy more than doubled over this period. Following the GFC, both commodity prices and Chinese growth were on a downtrend. These anecdotes led many investors to believe that if China’s economy was on the mend, it would drive the asset class in 2023. But we need only recall the challenges of 2022’s high inflationary environment to see the story unravel. China’s growth that year was 3%, a far cry from the nearly 7% clip it maintained before the pandemic. Commodities were unbothered, rallying 18%.

Taking a step back, it’s important to point out that commodity futures trading has been around for well over 100 years, dating back to the 1870s in the US. Returns for a diversified commodity portfolio over this long history have been significantly positive. From 1900 through 2022, they came to roughly 9% per year, according to data from AQR, though certainly with a fair amount of volatility. China undoubtedly has played a role in more recent outcomes for the asset class and will continue to do so in the future. But China alone can’t possibly account for all the strong gains dating back a century or more. Many different themes throughout history have converged to drive commodity price expansion, including exogenous shocks, supply-side constraints, and new economic developments.

Will the renewable energy transition lead to a new commodity supercycle?

At present the world is facing a challenging transition to renewable energy, which will take shape over years and potentially decades to come. We have yet to see any significant supply-side response to recent price gains, leading to still abnormal levels of backwardation across the asset class, something we’ve written about before. We believe the confluence of structural demand growth from the low-carbon transition and suppressed supply-side forces may result in long-term support for commodity prices.

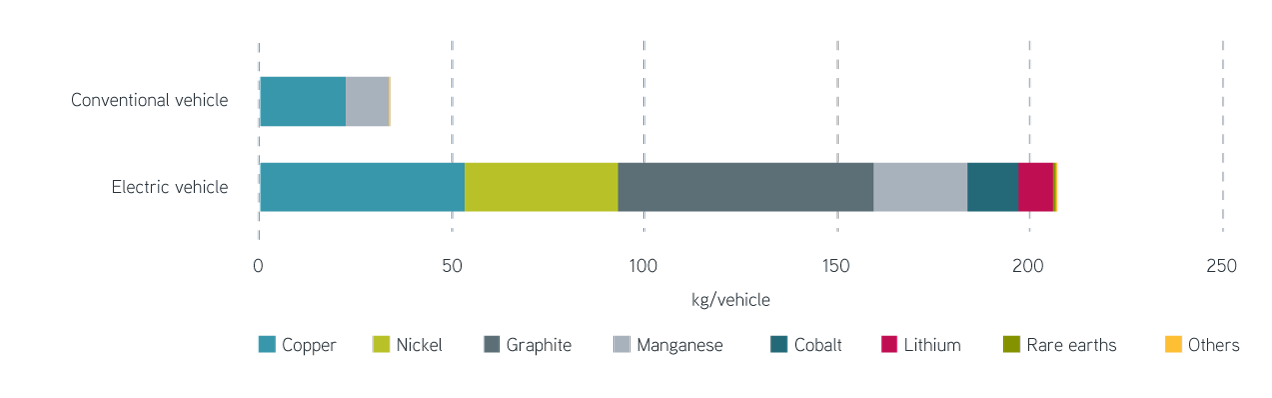

Maybe somewhat ironically, the move toward a more sustainable future will likely depend heavily on commodities. The resource requirements of a renewable-energy ecosystem differ profoundly from a fossil-fuel system. Take the transition from internal combustion engines to battery electric vehicles (EVs) as an example. Compared with a conventional vehicle, EVs require six times as many minerals—namely copper, nickel, and graphite—which are critical commodities for battery production.

Minerals used in the production of a single vehicle

Source: International Energy Agency, 5/5/2021. The values are for the entire vehicle including batteries, motors, and glider. Actual consumption can vary depending on battery technology choice.

In addition to commodity intensity, the speed of the transformation is crucial for estimating future commodity demand. Returning to the EV example, the adoption of EVs is booming, with the IEA expecting sales to leap 35% this year after a record-breaking 2022. S&P Global Mobility forecasts that EV sales in the US could reach 40% of total passenger-car sales by 2030. More optimistic projections call for EVs to surpass 50% worldwide by 2035.

Moreover, building the infrastructure associated with decarbonization could require additional use of fossil fuels and other traditional resources, at least in the short to medium term. In many ways, the path to clean energy will be dirty until a critical mass emerges. Altogether, capital spending on physical assets to reach net-zero emissions by 2050 could require over $9 trillion annually, according to McKinsey Global Institute. That’s significantly greater than the $2 trillion spent in 2021, and it dwarfs the infrastructure spending by China and other emerging market countries that helped propel the last commodity bull market.

The good news is that global reserves of critical resources appear likely to be large enough to cover the needs of the global low-carbon transition. The crucial question is whether natural resource producers can cope with this massive increase in demand over the next decade. Troublingly, some public companies have already started reducing their capital investments in favor of cash distributions to shareholders, in part due to investor preferences. Simply put, equity owners have demanded excess cash in the form of dividends and share buybacks, when companies could instead redeploy that cash into sectors of the economy that fit less well into the net-zero movement. This behavior reduces future supply in the marketplace, potentially too soon. Although the immediate situation isn’t yet so dire, even under the most conservative scenarios for demand growth in the coming years, many commodity markets are expected to be in short supply by the end of the decade. If policymakers implement more ambitious net-zero strategies, that timeline could easily compress.

The bottom line

Commodity investors have long thought their fate was tightly linked to Chinese economic growth. While periods of concert over the last two decades have added support to this theory, the truth is far more nuanced. Commodities have been traded for many years in the US and have delivered long-term value, though with a fair amount of volatility, irrespective of the triumphs and troubles of the world’s second-largest economy. In the end, global supply-and-demand dynamics dictate commodity prices, and both seem poised to support the asset class amid the secular shift to a more electrified world economy. Looking ahead, we see little reason to think the asset class won’t continue to offer value to strategic long-term investors.