The once-reliable link between commodities and the US dollar has been upended in recent years. Why has the connection changed? We look into the possible reasons.

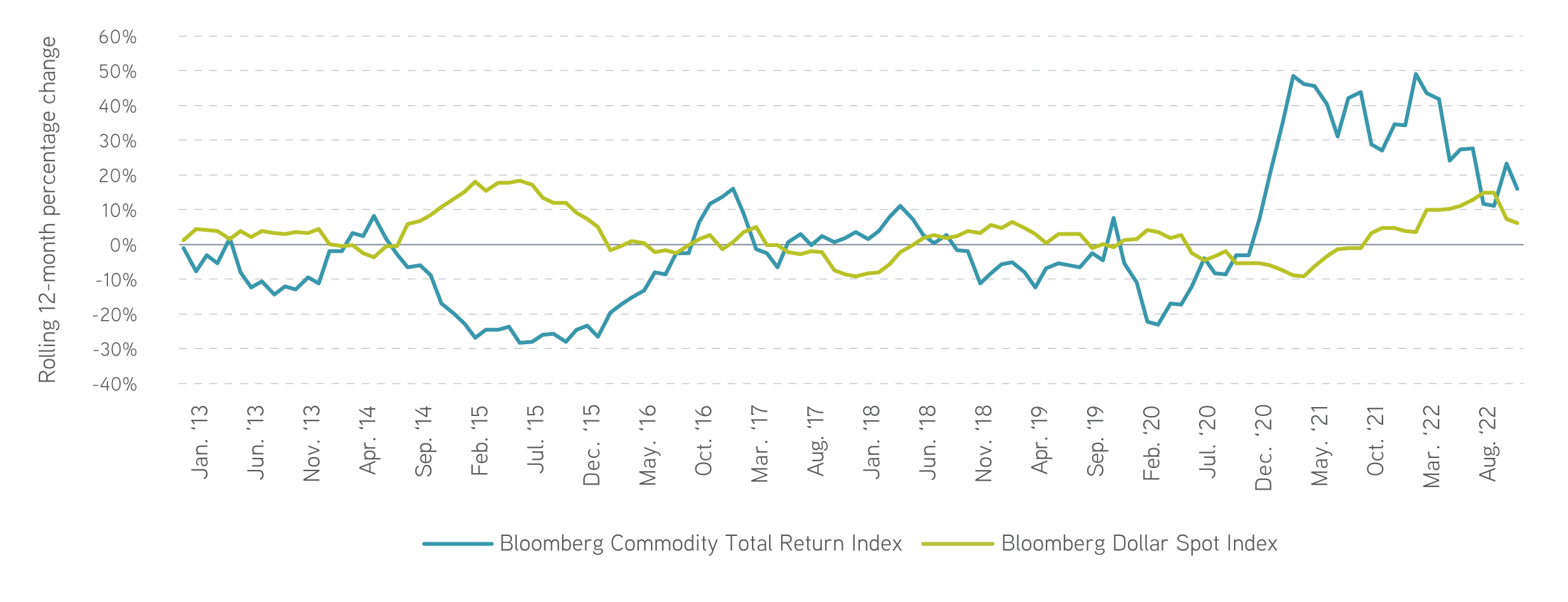

Although every commodity has its own distinct characteristics and price drivers, investors have time and again recognized a common link between the greenback and commodity prices. An inverse relationship typically exists between these assets, where a fall in the value of the US dollar is associated with a rise in commodity prices and vice versa. Consider the rolling 12-month performance of the Bloomberg Dollar Spot Index (BBDXY) and the Bloomberg Commodity Index (BCOMTR). While return patterns aren’t perfect mirror images of each other, they often move in opposite directions. All else equal, when the US dollar falls, commodity prices tend to rise, with the reverse occurring in periods of dollar strength.

Investors have been able to rely on this link in the past, but the pandemic upended this usually reliable behavior. Let’s take a look at what connects commodities to the dollar and why both have been rising recently.

Commodity index returns and dollar appreciation/depreciation, 2013–2022

Sources: Parametric, Bloomberg, 12/31/2022. For illustrative purposes only. Past performance is not indicative of future results. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index.

What connects commodity prices to the US dollar?

The root cause of this inverse relationship is open to debate, but there are several credible arguments. The dollar’s value tends to impact commodity prices because the US dollar is the most common pricing and settlement currency for commodities. When the dollar appreciates against other currencies, commodities become more expensive on the world stage, which can depress overall demand. As consumption falls, so do prices. Flip this dynamic on its head, and you can see that a fall in the greenback might stir prices higher.

Others argue that real assets like commodities have an intrinsic value, and as the value of the greenback fluctuates, this intrinsic value is repriced in dollar terms. So as the dollar becomes more valuable, it takes fewer dollars to purchase a commodity, and consequently its price needs to fall. It could also be that when the dollar rallies, exports of American-produced commodities are less competitive on the world stage. Dollar-based prices must then fall to match the effective price of global competitors in other currencies.

Regardless of the exact cause, the result is the same: dollar down, commodities up, or dollar up, commodities down. It’s been the case so often that most have taken it for granted. Many investors were therefore surprised to see both rally in the last few years.

How stable is the dollar-commodity relationship?

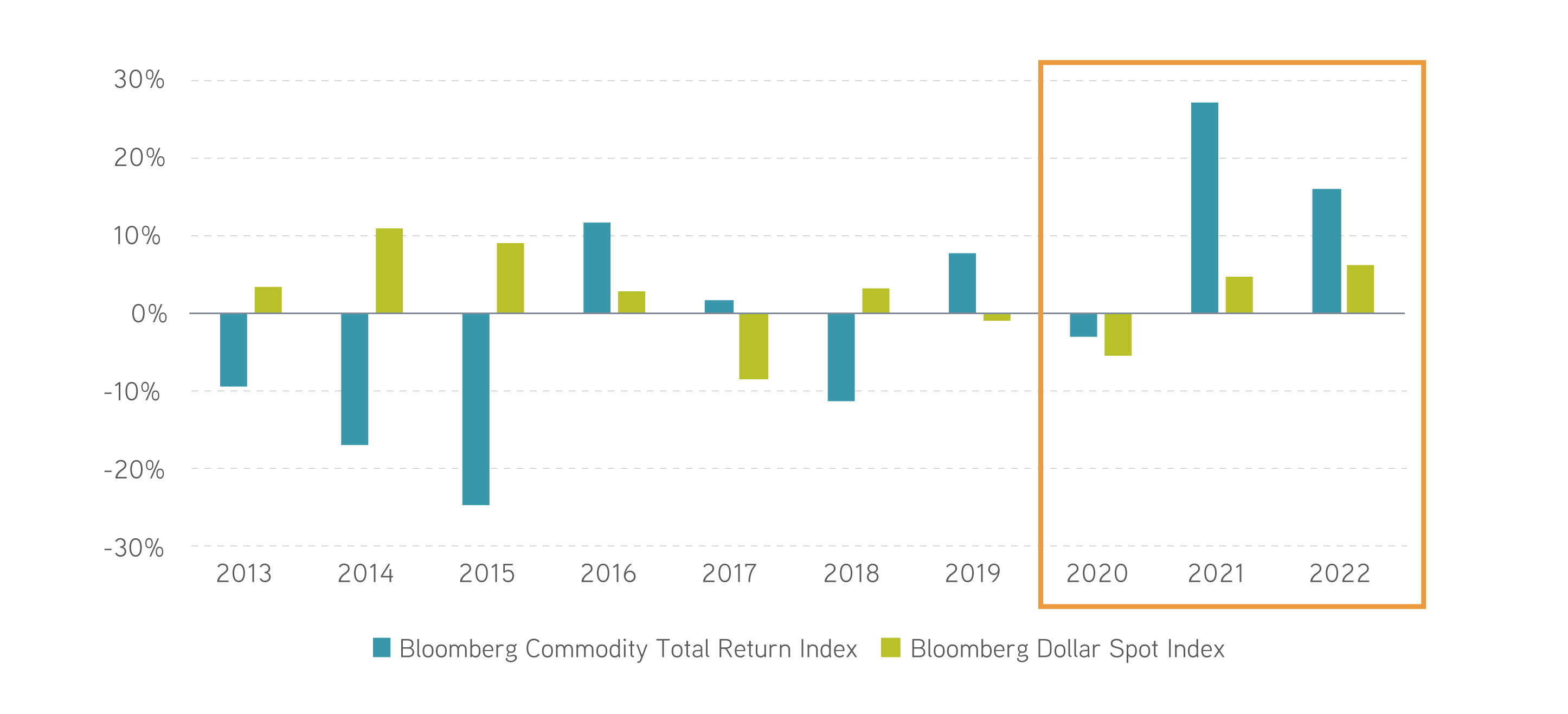

Truth be told, the dollar-commodity relationship behaves more as a rule of thumb than a law of nature. If the dollar falls by 10%, it doesn’t mean commodities will rise by 10%, and the strength of the correlation is time-varying. Simply isolating individual calendar-year returns reveals that the greenback and commodities moved in the same direction each of the last three years.

Commodity index and US dollar calendar-year returns, 2013–2022

Sources: Parametric, Bloomberg, 12/31/2022. For illustrative purposes only. Past performance is not indicative of future results. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index.

What might be driving the more recent breakdown? Why have commodities performed so well recently despite significant dollar strength? One cause was likely the path of Federal Reserve monetary policy: first cutting rates during the pandemic, then abruptly raising them to fend off inflation. Commodities are well recognized as an inflation-sensitive asset class, since they represent the basic raw materials that produce the goods in the Consumer Price Index. At least part of the recent strength in commodity prices can also be attributed to supply shocks, like those resulting from Russia’s invasion of Ukraine.

Rising US interest rates, on the other hand, are attractive to foreign investors who are on the hunt for higher returns. As capital pours into the US, it can drive up the value of the dollar. The recent strength in both assets strikes us as a natural outcome, given the common behavior of commodity prices rising with inflation and the US dollar appreciating when interest rates increase significantly. It’s challenging to say when this relationship will revert to its old ways. But investors should be aware that not all commodities are influenced by the dollar in the same way.

What happens at the individual commodity level?

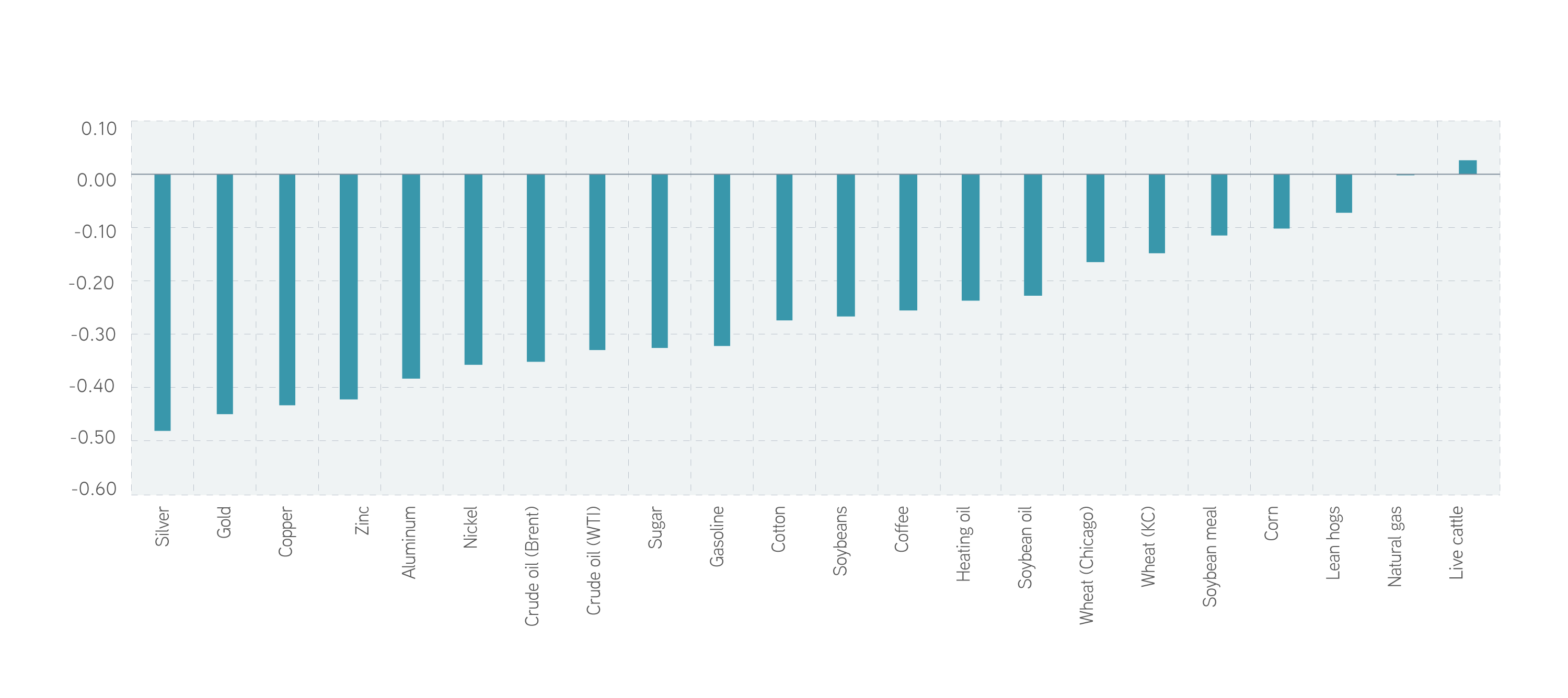

The degree to which this inverse relationship exists varies among individual commodities, and it typically weakens as other factors overwhelm the effect of currency movements. For instance, consider the fundamental differences between WTI crude oil and corn. The price of WTI crude oil is quoted in US dollars. It’s easily transported, has few substitutes, and has relatively constant demand. As a result, its price is tightly linked with movements in the dollar. But corn is affected by changing seasons, has several readily available substitutes, and is strongly influenced by weather patterns. The dollar-commodity relationship breaks down when we look at the price of corn.

We find a negative correlation for almost all individual commodities, reinforcing the notion of an inverse relationship between movements in commodity prices and the dollar. However, the magnitude of this correlation varies dramatically. Energy and industrial metals—which are transported globally and whose prices are traditionally quoted in US dollars—display the most striking relationship. In contrast, commodities that are most impacted by the weather, like livestock and grain, or that aren’t easily exportable to global markets, like natural gas, have the weakest dollar-commodity relationship.

10-year correlations between Bloomberg Dollar Spot Index and individual commodities

Sources: Parametric, Bloomberg, 12/31/2022. For illustrative purposes only. Past performance is not indicative of future results. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index.

The bottom line

Commodity prices have historically fallen in times of dollar strength and risen in times of dollar weakness. While the power of this relationship varies over time and by commodity, as a rule of thumb we see it come out in the data. It’s not easy to break out the exact magnitude of this relationship when explaining commodity price changes. However, it’s worth noting how strong commodities have performed over the past few years in the face of headwinds from the US dollar bull market. If the dollar eases up from here, it could provide another tailwind to commodity prices for investors.

The value of commodity investments will generally be affected by overall market movements and factors specific to a particular industry or commodity, which may include weather, embargoes, tariffs, health, political, and international and regulatory developments. Economic events and other events (whether real or perceived) can reduce the demand for commodities, which may reduce market prices and cause their value to fall. The use of derivatives can lead to losses or adverse movements in the price or value of the asset, index, rate, or instrument underlying a derivative due to failure of a counterparty or due to tax or regulatory constraints.