The first half of 2023 has brought some reprieve from the dollar’s one-way march higher, to the delight of many emerging market equity investors, but what will the second half bring? Let’s look at a couple of themes that may shape its path forward for the remainder of 2023.

At a G10 meeting many decades ago, the then US Treasury secretary John Connally famously quipped to a room full of his counterparts, “The dollar may be our currency, but it’s your problem.” For emerging market (EM) investors, it’s been a bigger nuisance than normal lately. Since the end of 2020, the greenback has gained nearly 10% against a basket of leading global currencies, even double that at one point in late December 2022. The catalyst has been a combination of things: higher US interest rates, diverging global growth conditions, and a general preference for safety amid heightened geopolitical tensions.

For US-based investors in EM stocks, the dollar’s strength has been unwelcome. Not only can it affect the return prospects for stocks listed in EM countries through higher inflation and interest rates, for example, or by inducing greater fiscal stress on their economies as the cost to service dollar-denominated debt rises. A strong dollar creates a more direct headwind to performance as many foreign currencies lose value to the greenback, which translates into lower returns for investors.

When will the Fed stop hiking interest rates?

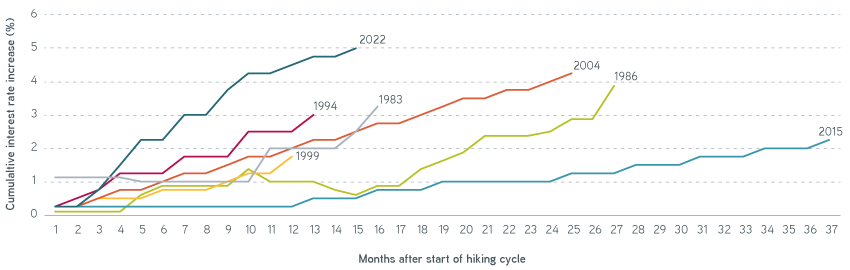

The Fed‘s interest rate policy has been a major source of the dollar’s gains. Since March 2022, the Fed has hiked the federal funds rate—the rate at which banks borrow cash held at Federal Reserve Banks from one another—an astonishing 10 times, desperately trying to bring down the overall rate of inflation. These moves have pushed the rate from near 0% in early 2022 to more than 5% today, the fastest increase since the great inflationary episode of the 1970s and early ’80s. This has driven marginal flows into the dollar, bidding up its price as international investors have sought out the highest returns they can find.

Cumulative change in federal funds target rate (midpoint of range)

Sources: Bloomberg, Federal Reserve, 5/23/2023. For illustrative purposes only.

Having acted aggressively, the Fed now finds itself in a bit of a pickle. US inflation has come off the boil but still sits uncomfortably high relative to the Fed’s long-term target of 2% average inflation. It’s well known that policy moves take effect with long and variable lags, meaning the cumulative impact of interest rate hikes is likely yet to take effect in earnest. And with the regional banking crisis still on the minds of many, it seems probable the Fed might take a breather from rate increases for a while. The market seems to have reached the same conclusion: Pricing in the fed funds futures market suggests that interest rate cuts could be in the cards later this year, undoubtedly a reflection of some concern that economic activity may wane.

On the other hand, recent economic data remains strong. The economy continues to add jobs at a robust pace, picking up an average of 330,000 per month over the past 12 months. Unemployment remains near a 50-year low, and unit labor costs have continued to run above average, which could put pressure on inflation going forward. The Fed has its work cut out for it. Regardless of where the economy goes from here, it seems unlikely that the recent pace of interest rate hikes will continue, which could lead the dollar to meet some selling pressure in the near term.

Access the growth potential of emerging markets

How will geopolitical risk affect the dollar?

Some have said that the dollar has a smile. What they mean is that the dollar tends to appreciate in times of both great financial stress (thus its safe-haven status) and great investor enthusiasm, but it sags during the in-between periods. As we witnessed when Russia invaded Ukraine, turbulent geopolitical events tend to drive the dollar up as investors clamor for the currency’s stability. In the immediate days following Russia’s initial attack, the greenback traded higher by as much as 7% against some EM currencies, well outside its typical range. Though the war is ongoing, its impact on the dollar has subsided as other events have taken center stage.

As we peer into the rest of 2023, the most obvious area of geopolitical risk is a bilateral affair between the US and China. China’s economy has come a long way since its ascent into the World Trade Organization in 2001, with widespread reforms in the 1990s paving the way for meaningful per-capita income increases and the country becoming the world's second-largest economy. China’s growth hasn’t come without pains, however, as the country’s rapid export growth has affected various sectors and industries in Europe and the US, stoking trade tensions.

More recently, major trading partners have questioned the growing role of the Chinese state in domestic and international markets, with unease over the transfer of technology and the reach of state-owned enterprises drawing strong concerns. Tensions between the US and China reached new levels in July 2018, when the US imposed 25% tariffs on $34 billion of Chinese imports, setting off an immediate response from China and many tit-for-tat retaliations since. The most recent of these saw the US expand the fight to semiconductors and green energy by limiting exports of critical equipment in an attempt to block China’s advancement in those sectors. Whether a result of escalating trade tensions or other disagreements between the world’s top two economies, where this relationship goes from here could shape the dollar’s future for some time to come.

The bottom line

The dollar’s recent strength has been notable, though it comes as little surprise given postpandemic global dynamics. For US-based investors in EMs, a rising greenback has led to headwinds for performance as foreign currencies haven’t fetched as much value when translated back into USD. We believe the dollar's strength could be fading as themes supporting the greenback lose momentum. In particular, a slowdown or pause in interest rate hikes by the Fed or a period of relative calm in global geopolitics could both derail the dollar's might. For investors seeking to limit the greenback’s impact, one possible long-term solution is to diversify across EM countries, which can help minimize any outsized impact from a single currency in the portfolio.