Despite recent struggles, emerging markets can be a valuable part of a diversified portfolio. We believe in emerging market equities as a means of diversifying portfolios across markets, minimizing risk, and maximizing growth opportunities.

Historically, we’ve pointed to long-term demographic and economic trends as key motivations for investing in the emerging markets asset class. Specifically, the developing world’s percentage of global population is growing and, with it, its share of economic activity. These trends provide compelling evidence that, in the long term, there are powerful tailwinds to the returns available in emerging market equities.

However, recent performance has some investors on edge. Emerging market stocks took a drubbing in the second quarter, with the MSCI Emerging Markets Index falling 11.4%. That was the worst quarterly performance since the pandemic started, and the asset class now sits 17.6% lower than at the start of the year. If prognosticators are proved correct, the next couple of quarters won’t be much better. Global growth is expected to slow substantially as consumers react to both surging food and energy prices and a global tightening of financial conditions. Adding to these risks are the war in Ukraine, the enduring pandemic, and a slowdown in China. There’s plenty to worry about, and many investors are wondering if they should stay in the asset class now, with little consideration for longer-term trends. The way we see it, there are three important arguments for sticking with the emerging markets or, if not currently invested, why an investor might consider now to be an opportunity to add exposure.

Unconscious underweight

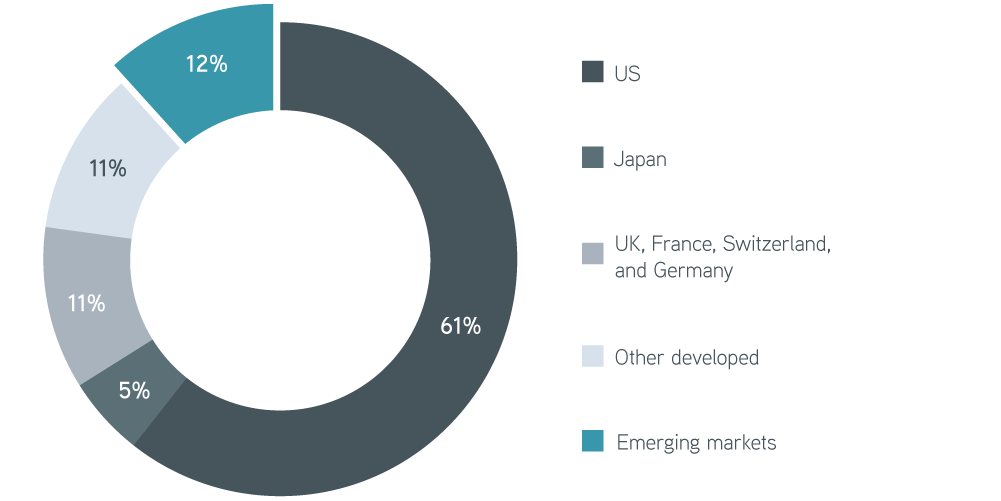

Emerging markets have collectively grown to a point where they’re too big to ignore when allocating capital. If we use market capitalization as a frame of reference, excluding EM stocks represents a material underweight from a neutral position. Shares in EM countries represented 11.7% of the MSCI ACWI Index at the end of the second quarter. For an investor not to hold any emerging market stocks would imply they despise the asset class so much that a nearly 12% underweight is desirable relative to an unbiased position. In conversations with clients, we rarely find a level of conviction that rises to the magnitude of taking on such a large bet.

MSCI ACWI country weights, as of 6/30/2022

Sources: MSCI, Bloomberg, Parametric, 7/18/2022. For illustrative purposes only. It is not possible to invest directly in an index. Not a recommendation to buy or sell any security.

Removing EM shares from a portfolio would create twice as large a gap as excluding all of Japan and one similar in size to removing France, Switzerland, Germany, and the UK. Most investors would consider these latter examples irrational; we would view excluding emerging market equities from a diversified portfolio as equally reckless.

Tapping into emerging markets

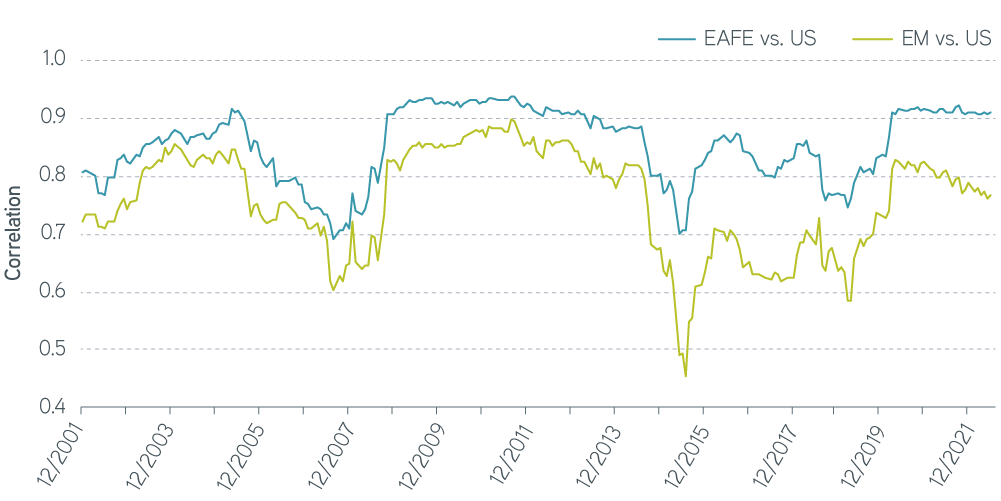

By moving beyond their home countries, investors can tap into markets that might provide different return patterns and opportunities to diversify their portfolios. Emerging markets can play a key role here because they aren’t as integrated into the global economy, since local industries are more internally focused. Aside from the largest developing nations, the stock markets of these countries are driven more by local events and their individual dynamics and are less influenced by global goings-on. This leads to equity markets that are less correlated with the equity markets of the developed world. Indeed, we’ve seen consistently that EM stocks have had a lower correlation to US markets than international developed stocks have.

Diversification, growth, and volatility capture

Sources: MSCI, Bloomberg, Parametric, 7/18/2022. For illustrative purposes only. It is not possible to invest directly in an index. Not a recommendation to buy or sell any security.

Lower correlations are useful when it comes to portfolio construction. They give investors a chance to piece together a set of assets that should have a lower level of expected volatility and possibly a higher level of expected returns. Portfolios that include EM companies are positioned to benefit from this diversification.

That brings to the fore the recent experience in emerging markets, which may raise the question of why an allocation even exists. EM stocks are roughly flat over the prior couple of years, while US stocks have risen (July 2020 through June 2022; MSCI EM Net TR Index: 5.3%, MSCI USA Net TR Index: 23.2%). However, we view this as evidence the asset class remains a solid diversifier, as the very nature of diversification means that one asset zigs while the other zags.

Valuations

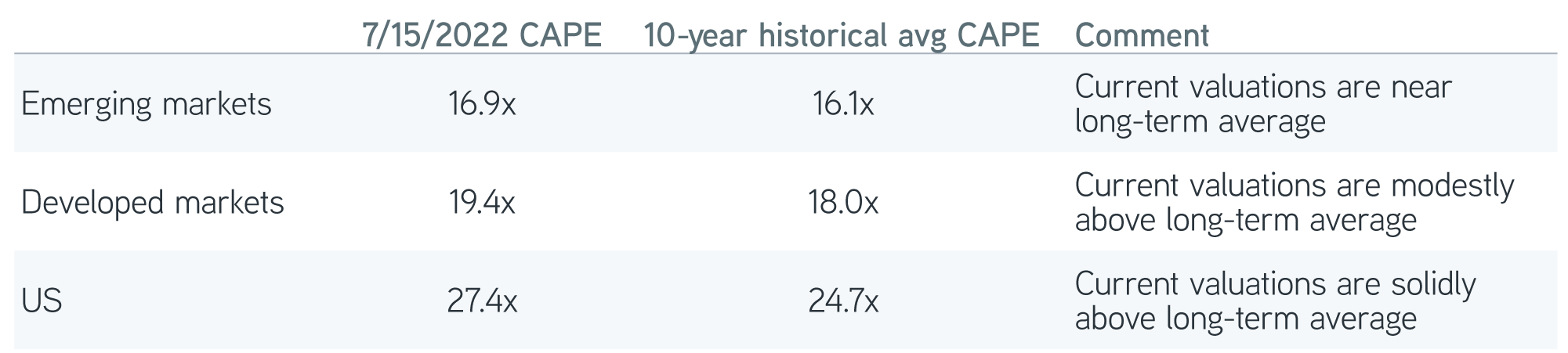

Valuation metrics are used to gauge whether a stock or group of stocks is over- or undervalued relative to its own history and its peers. Investors often put forward the cyclically adjusted price-to-earnings ratio (CAPE), developed by American economist Robert Shiller, as providing a reasonable assessment of valuation for equities. The ratio divides the current price by average earnings over the prior 10 years, both adjusted for inflation. Average earnings are used to help smooth business cycle variability, which can distort the standard price-to-earnings measurement at various points in time. We agree this is a reasonable approach to assessing valuations and provide CAPE ratios for emerging markets, developed markets, and the US below.

CAPE ratios for emerging markets, developed markets, and the US

Sources: MSCI, Bloomberg, Parametric, 7/18/2022. Emerging markets represented by MSCI Emerging Markets Index, developed markets represented by MSCI EAFE Index, and US represented by MSCI USA Index. For illustrative purposes only. It is not possible to invest directly in an index. Not a recommendation to buy or sell any security.

From the table, we suspect that most valuation-sensitive investors would find the emerging markets attractive on an asset-class relative basis (lower than developed markets and the US), as well as reasonably priced versus its own history (16.9x currently versus a historical 16.1x). That leaves us puzzled about why many investors are now considering ditching the asset class or exchanging it for US equities, neither of which is supported by the data.

The bottom line

Recent weakness in the emerging markets and fears of further struggles have left many allocators questioning the usefulness of including the asset class in an overall portfolio. While Parametric doesn’t focus on forecasting future performance, we believe there remain several solid reasons for owning emerging market equities. With respect to the global opportunity set, EM stocks represent a material exposure, the exclusion of which would require a high degree of conviction and would be similar in size to excluding the four largest European nations. The asset class remains a strong diversifier for an investor’s portfolio and, from a generally accepted valuation perspective, is reasonably priced compared to its historical average and remains cheap compared to developed peers. Investors in search of higher returns will inevitably encounter periods of heightened volatility, as we’ve witnessed so far this year. The best remedy remains to diversify across markets to both minimize risk and maximize growth opportunities.

“MSCI” and MSCI Index names are service marks of MSCI Inc. (“MSCI”) or its affiliates. The strategy is not sponsored, guaranteed, or endorsed by MSCI or its affiliates. MSCI makes no warranty or bears any liability as to the results to be obtained by any person or any entity from the use of any such MSCI Index or any data included therein. Please refer to the specific service provider’s website for complete details on all indexes.