Are money market funds the best place for institutional collateral? With Treasury yields on the rise, it’s time for institutions to reevaluate their cash positions. Find out why separately managed accounts may serve overlay investors better.

Zero-bound short-term interest rates are gone, which means cash is now earning a meaningful return. The six-month US Treasury bill yield surpassed 5.3% in May, a level not seen in over 17 years. Investors should take this opportunity to evaluate their existing investments, namely money-market funds, and compare alternatives.

One particular area where overlay investors should rethink their portfolios is the collateral posted to their separately managed accounts (SMAs). We often find that investors can move collateral resting in money market funds to more efficient products. Let’s discuss the limitations of pooled money market funds and the potential benefits of a customized SMA: incremental yield, lower costs, and increased capital efficiency.

What are the drawbacks of money market funds?

Overlay investors are required to use collateral, often in the form of cash, to partially fund their derivatives positions. They use this collateral to meet their overlays’ initial and daily mark-to-market variation margin needs. Managers then work with investors to determine the appropriate amount of collateral needed to support their overlay positions. The analysis considers the volatility of the positions, the leverage employed, and the ease by which the investors can raise additional funds. Under most market conditions, the overlay doesn’t require use of much of this cash collateral, the excess of which remains with the custodian. Most often this excess cash is swept into a money market mutual fund, but the default solution isn’t necessarily best for all investors.

Money market managers are often legally required to manage funds conservatively for maximum liquidity. The SEC requires 2a-7 funds to meet daily and weekly liquidity thresholds and maintain a portfolio-wide weighted average maturity (WAM) of 60 days or less. Individual securities also must not exceed 397 days to maturity at time of purchase. Furthermore, the investible universe can be highly restrictive, often limited only to US government–issued securities. Money market alternatives, like derivatives and longer-dated securities, are prohibited. These rules exist to protect money market investors in the event of adverse market conditions and extreme redemption events across many investors. Money market funds can survive without breaking the buck (falling below $1 in net asset value), even when daily redemptions are very large.

A typical SMA overlay investor doesn’t face nearly the same liquidity requirements. An SMA manager can customize the portfolio’s liquidity profile to the needs of each investor. Redemptions are potentially smaller and more manageable, and the investor often has other sources of liquidity to draw on in a pinch. This means the SMA overlay investor can trade some amount of liquidity for more flexibility and potentially better returns.

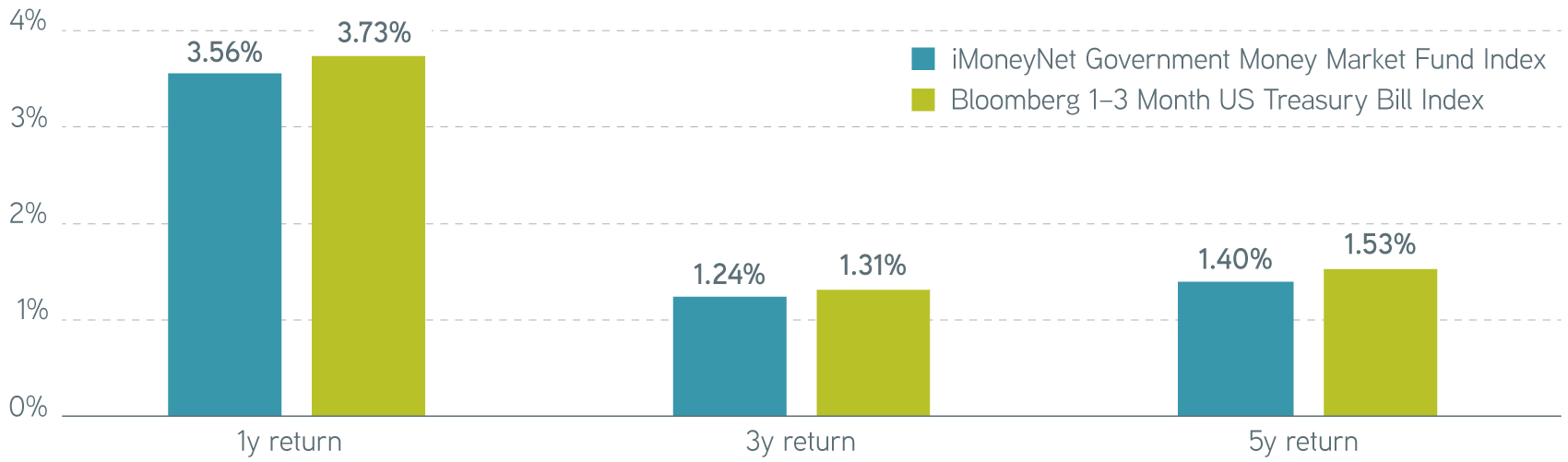

All money market investors bear the costs of these restrictions, despite their varying liquidity needs. Add in typical money market fees for institutional investors of 15 to 25 basis points, and we see rather pedestrian returns over time. Many funds struggle to keep up with a simple Treasury index net of fees. For example, if we observe the average of all institutional government money market funds, we see them failing to keep up with a simple portfolio of T-bills over time.

Money market fund index vs. Treasury index returns

Sources: iMoneyNet, Bloomberg, 06/30/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses.

How can overlay investors allocate excess cash more efficiently?

Investors can consider keeping their cash collateral in an SMA, with no other investors taking distributions. They can then reallocate the funds as needed in a manner customized to the overlay’s target risk profile and their own unique return needs. Customization also makes it possible to add duration or credit risk and take advantage of other money-market alternative investments. For example, SOFR futures combined with overnight repurchase agreements to create longer-term repo can at times be an attractive alternative to bills.

Investing excess cash in an SMA has another advantage. Initial margin requirements can often be more than 5% of the overlay’s notional value. A variety of income-generating instruments, not just cash, can be posted to meet these requirements. For example, Treasuries or other bonds in an SMA cash management account can serve the dual purpose of initial margin and return generation.

The bottom line

With short-term rates climbing well above 5%, it makes sense for overlay investors to weigh all the available options for their cash collateral. The liquidity that money market funds provide can come at the expense of high fees and limited ability to customize exposure. Managing cash in an SMA gives investors more control, potentially reducing fees while providing a better fit to their risk tolerance and income needs.

Risk management solutions for uncertain markets