As 2021 saw greater focus on environmental, social, and governance (ESG) issues, ESG-labeled bonds played an important role across various sectors of fixed income markets. Fund inflows into ESG-focused funds seem likely to continue growing, and responsible investors should expect issuance of green, social, and sustainability bonds to follow suit.

Along with increasingly serious implications of climate change—from extreme flooding across the Midwest and Eastern Seaboard to prolonged drought conditions in the West—2021 saw a growing affordable housing crisis in many US metropolitan areas. In addition, addressing social issues related to diversity and equity continues to be an important responsible investing theme. Capital markets can help address the critical environmental and social challenges in front of us.

2021: The year sustainable bond issuance surpassed $1 trillion

In fixed income markets, bonds used to finance projects designed to improve environmental and social outcomes are known as sustainable bonds, which include the following:

- Green bonds issued to fund projects with a positive environmental or climate-aligned purpose

- Social bonds funding projects intended to achieve positive social outcomes

- Sustainability bonds funding a combination of environmental and social projects or activities

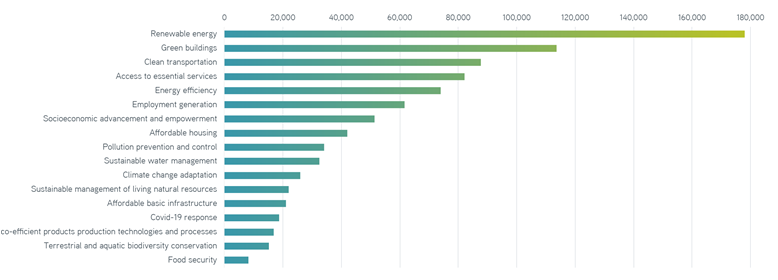

Sustainable bonds—bonds with a green, sustainability, or social label, either as self-declared by the issuer or verified by a third party—passed the $1 trillion mark in annual global issuance for the first time in 2021. The $1.036 trillion in issuance was a 71% increase over 2020 and comprised all fixed income sectors, including corporates, agencies, sovereigns, sub-sovereigns, supranationals, and private entities.

In the US corporate credit market, total issuance of sustainable bonds grew to $123 billion in 2021, a 126% year-over-year increase. In the high-yield corporate bond space, ESG bond issuance totaled $23 billion, a 323% year-over-year increase. Green bonds made up a majority of total ESG-labeled bond issuance with $67 billion, followed by sustainability and social bonds. Some green bonds in the corporate market are issued by banks to finance loans to clients for construction of Leadership in Energy and Environmental Design (LEED)–certified residential and commercial buildings or to finance renewable-energy projects.

A major US bank recently released its social bond framework outlining the eligible uses of proceeds for bonds issued under the label, including economic development for financing loans to small businesses, affordable housing, and access to health care and education in low- to moderate-income communities. Its first social bond was issued in 2021 to finance the construction and rehabilitation of 223 affordable housing units across 36 states. ESG-labeled investment-grade (IG) corporate issuance remains heavily concentrated in the financial, utility, and real estate sectors, but we may see diversification into more sectors as sustainability-linked bonds grow.

The municipal bond market saw another record year for sustainable bonds in 2021, with $46 billion in issuance across the three categories, totaling 9.7% of overall municipal bond issuance for the year. This was an increase of 71% over the $27 billion in ESG-labeled issuance in 2020. To a large extent, affordable housing projects drove the growth in these labeled bonds. Housing bonds in the social and sustainability bond categories showed $11 billion in total issuance, surpassing mass transit as the largest sector of ESG-labeled bonds in the municipal market.

The green bond category, which covers a range of issuers and sectors, continues to expand, including bonds issued for environmental and climate-focused projects like sustainable building, wastewater management, renewable energy, and climate-adaptive infrastructure. There’s growing overlap between socially and environmentally focused projects, with issuers in the health care and higher education sectors issuing more green bonds for LEED-certified building projects and public school districts issuing green bonds for solar panels on school buildings. The largest issuing state continues to be California, with $13 billion in sustainable bond issuance in 2021, followed by New York and Washington.

Construct a portfolio aligned with your principles

Source: Environmental Finance Bond Database, 2022

Investor appetite for ESG-labeled bonds is growing along with supply. ESG bond funds saw positive inflows in January 2022, while non-ESG bond funds saw outflows both domestically and globally. According to Bank of America Global Research, global inflows into ESG funds amounted to $7 billion, while non-ESG funds saw negative outflows of $31 billion. While US-based ESG bond funds represent a small percentage of total AUM in US bond funds, US ESG assets grew by 76% in 2021 to $100 billion, significantly outpacing non-ESG assets, which grew 9.2% over the same time period.

What’s next for ESG fixed income markets?

S&P Global predicts global issuance of sustainable or ESG-labeled bond issuance will surpass $1.5 trillion in 2022, equating to 17% of total projected bond issuance for the year. Based on current growth projections for labeled bonds in the municipal bond market, issuance could grow to $60 billion this year, which would equate to about 12.3% of total projected annual issuance for that market. As the municipal market funds a significant number of projects and entities closely aligned with the goals of impact investing, the amount of labeled bonds should continue to climb, as should the ratio of ESG-labeled issuance compared with non-ESG-labeled issuance.

Passage of the Bipartisan Infrastructure Law in November 2021 could spur issuance of more ESG-labeled bonds. This legislation included $550 billion in total spending for initiatives that may be financed through the municipal bond market, such as clean water, removing lead pipes from outdated water systems, energy efficiency improvements to buildings, clean energy, climate-resilient infrastructure, and funding for mass transit systems.

With issuance of ESG-labeled bonds continuing to see consistent growth year over year, there will be greater pressure from investors to maintain the integrity of sustainable debt markets, requiring more transparency and better disclosure practices from issuers. Global standard-setting bodies like the Sustainability Accounting Standards Board (SASB) could help address some common obstacles to establishing standard disclosure practices. Data is critical to ESG investing, and investors will look for ESG-related disclosures from issuers around important ESG themes like climate and diversity. There will also be heightened scrutiny regarding around the potential for greenwashing, or misleading investors on the environmental benefits of a bond issue or environmental practices of an issuer.

Finally, the potential for a “greenium” or price premium on these labeled bonds will continue to draw interest from the market. The corporate bond market has seen a slight premium on corporate ESG-labeled bonds. According to the Morgan Stanley 2022 Global Sustainability Report, when controlling for ESG versus non-ESG bonds from the same issuer, ESG-labeled bonds are trading about five basis points (bps) higher than non-ESG bonds.

Conversely, there’s currently no price premium for ESG-labeled bonds compared with non-labeled bonds from the same issuer in the municipal market. This could change in the future as investor demand for ESG-labeled bonds increases. The potential performance upside in impact bonds may pique interest from investors.

The bottom line

Significant growth in ESG-labeled bond issuance is likely to persist, along with investor interest in this segment of the fixed income markets. In addition, as fund flows toward ESG and sustainable funds continue to grow and impact bonds comprise a bigger share of overall bond issuance, investors will likely look for better disclosure practices from issuers, as well as due diligence from investment managers to avoid issuers engaged in greenwashing. Overall, impact bonds should continue to play an increasingly important role.