Taxes can have a major impact on the long-term growth of a portfolio. Find out how continuous, thoughtful tax management can help investors maximize their wealth.

How did your portfolio do after taxes? I suspect many investors have absolutely no idea. Everywhere we look, taxable investors seem to be focused on pretax returns. But at Parametric, we think it’s after-tax returns that matter.

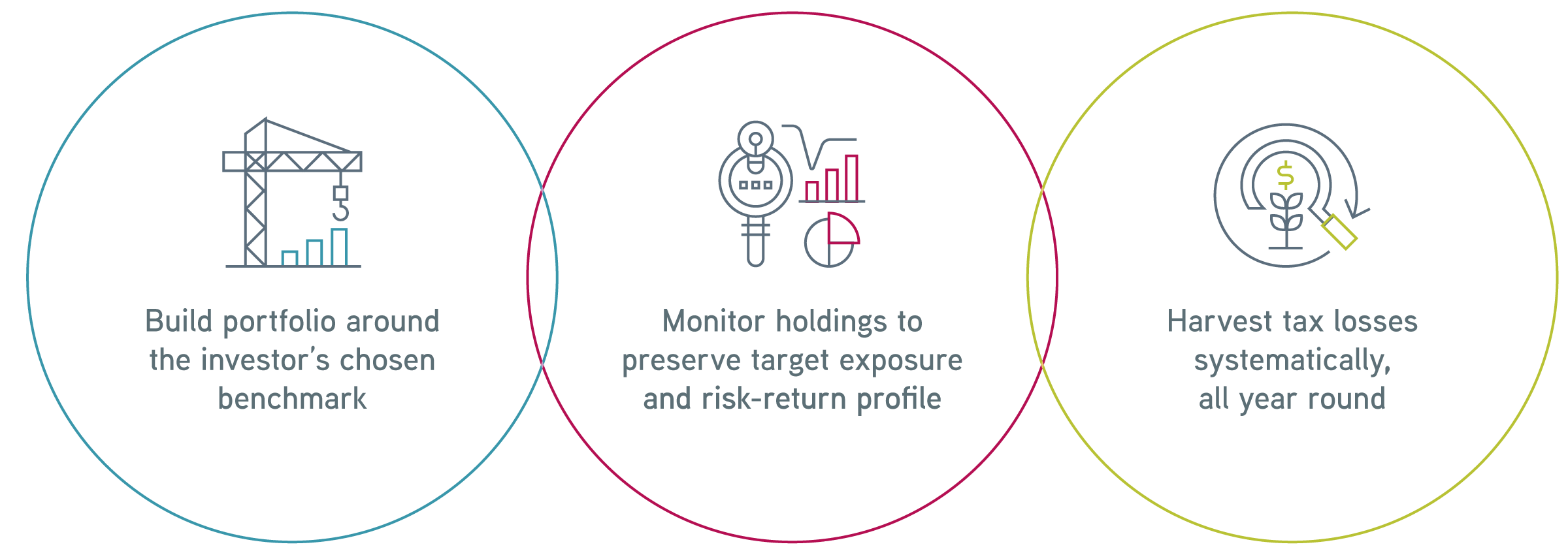

Tax management is a way to make sure that when investors pay taxes, they don’t give up more return than they have to. But not all tax management is the same. Let’s look at how this approach works in direct indexing portfolios.

What should investors know about taxes?

Just to review, here are some key features of the US tax code that may influence good tax management practices.

- Taxable event. Investors get a tax bill only if they sell a security for more than they paid for it. The tax is applied to the difference and owed in the tax year of the sale. Unrealized gains aren’t subject to tax.

- Tax-rate differential. Securities sold less than a year after purchase are taxed at a higher rate than those held for longer than a year.

- Treatment of losses. If an investor sells a security at a loss, they don’t get a check from the IRS, but they can use the loss to offset capital gains elsewhere in their holdings. Any excess losses can be carried over to future years.

Although these rules may be subject to change, they’ve endured over time. And they act in concert—that is, even if one rule evolves, the others still offer plenty of value to tax management.

What does tax management involve?

Tax management means being careful about realizing gains and strategic about realizing losses, using four primary techniques:

1. Holding securities long enough to qualify for a lower tax rate on long-term gains.

2. Selecting loss-maximizing or gain-minimizing tax lots for trades.

3. Moving securities into or out of a portfolio in kind, instead of liquidating.

4. Avoiding purchases that would disallow losses according to IRS wash-sale rules.

While not as exciting as trying to predict the price of oil or anticipating the next big tech stock, being savvy about the tax consequences of trading can help preserve wealth in a portfolio. This gives investors more dollars to put to work in the market, and that can really add up over the long run. Third-party research has shown that tax management may have the potential to add 1%–2% in after-tax excess returns.1

These techniques are available to any investor, yet they may be an afterthought for many—addressed only once a year, if at all. Tax management might be at odds with the alpha-seeking goals of the manager selected by the investor. Passive index-based mutual funds or ETFs may be relatively tax efficient, but they can’t produce any additional tax benefits for the investor. For that, we believe a tax-managed direct indexing portfolio could be the solution.

Consider the benefits of active tax management

How tax management works in direct indexing portfolios

In a direct indexing portfolio, an investor gets a core market exposure with an explicit focus on taxes. Not only is this portfolio inherently tax efficient, it can also produce excess losses, which can then be used to offset other gains among the investor’s holdings.

To understand why, let’s consider the key difference between direct indexing and index-based ETFs or mutual funds. In those vehicles, the investor holds a single security whose returns are based on a basket of underlying securities. But in a direct indexing portfolio, the investor owns the individual underlying securities directly—hence the term direct indexing. These securities are selected based on a benchmark chosen by the investor, which could be a custom benchmark or a blend of two or more popular benchmarks.

Owning hundreds of securities directly gives the investor more potential to execute the tax management techniques listed above. That helps make direct indexing a compelling choice for the taxable investor.

A direct indexing approach recognizes the tension between the dual goals of being the market and beating the market after taxes. To be the market, the investor needs to invest in securities that are similar in aggregate to the benchmark. To beat the market, the investor needs to be able to deviate from the benchmark. With hundreds or thousands of securities—and even more tax lots in the portfolio—the investor has greater flexibility to defer gains or harvest losses, while still getting market-like returns on an after-tax basis.

Direct indexing portfolios can also accept securities in kind and transfer them out without liquidating them. And most important, each security’s tax characteristics and trading patterns can be unique to the investor, who doesn’t have to bear the tax consequences of another investor’s trading and investment needs.

When tax management tends to work best

Tax management really boils down to paying attention to the tax consequences of each trading decision and using a disciplined process to balance the trade-offs. Here are some factors that can influence its success:

- Market conditions. As with any investment process, market conditions can be more or less conducive to the goal of tax management. Benefits tend to be greater in highly volatile markets and more muted in steady up markets.

- Tax conditions. Investors living in tax jurisdictions with high rates may find tax management even more compelling. Higher tax rates raise the value of deferring some gains and offsetting others with losses—particularly when losses can help to offset short-term gains.

- Investor needs. Each investor’s situation is unique. For those facing a significant taxable event, holding highly appreciated securities or investments that produce a lot of short-term gains, or planning charitable giving, tax management may be more valuable.

The bottom line

Direct indexing is uniquely positioned to serve the needs of taxable investors. In the right hands, it can be used to form a core market exposure within a broad portfolio that’s not only tax efficient in itself but can also be used to enhance the tax efficiency of the investor’s overall holdings. We believe this can be a boon for investor wealth over the long run.

1 Shomesh E. Chaudhuri, Terence C. Burnham and Andrew W. Lo, 2020. “An Empirical Evaluation of Tax-Loss-Harvesting Alpha,” Financial Analysts Journal 76:3, 99–108. This study did not involve Parametric or its clients. There is no guarantee that a tax management strategy will result in increased after-tax returns. Results will differ based on an individual investor’s circumstances.

Parametric and Morgan Stanley do not provide legal, tax or accounting advice or services. Clients should consult with their own tax or legal advisor prior to entering into any transaction or strategy.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

9.23.2027 | RO 4844058