It’s hard to believe we’re already halfway through 2023, but that means it’s time to offer our midyear outlook for liability-driven investing (LDI). Given uncertain market conditions, plan sponsors should stay vigilant and watch for opportunities.

To understand where opportunity may lurk in the LDI world, let’s look first at what’s happened so far this year. Some plans may have already clamped down on surplus volatility and are in effect hibernating, running with nearly no risk until prices make sense for annuitizing all benefits (as opposed to a partial plan transfer). Other plans might have very effective total-plan LDI strategies in place without truly hibernating. Still others aren’t as far along as they would like to be.

In any case, plan sponsors should keep an eye on what the market is offering and look for opportunities to continue to refine and enhance their plan’s LDI solutions. Going forward, pension plans need to consider how LDI can be used to react to higher yields than we’ve seen in years, an inverted yield curve, liquidity needs, and credit spread levels. Like with so much else in life, there are a lot of moving pieces.

What does recent index performance mean for LDI?

At the end of last year, pension plans breathed a sigh of relief. Market returns in 2022 were terrible, and asset levels dropped significantly. But on the other side of the coin, liabilities had dropped even more because discount yields had risen so much. The net result was that pension plans became better funded than they had been in years, as we discussed at the beginning of the year.

Since then, we’ve seen stronger-than-expected equity returns, with S&P 500® returns of 16.89% and MSCI EAFE returns of 11.67% year-to-date (YTD) through June 30. Bonds have also chipped in positive returns, with Bloomberg US Corporates returning 3.21% and Bloomberg US Long Treasury bonds returning 3.72%.

Source: Parametric, 6/30/2023. For illustrative purposes only. Past performance is not an indicator of future results. It is not possible to invest directly in an index.

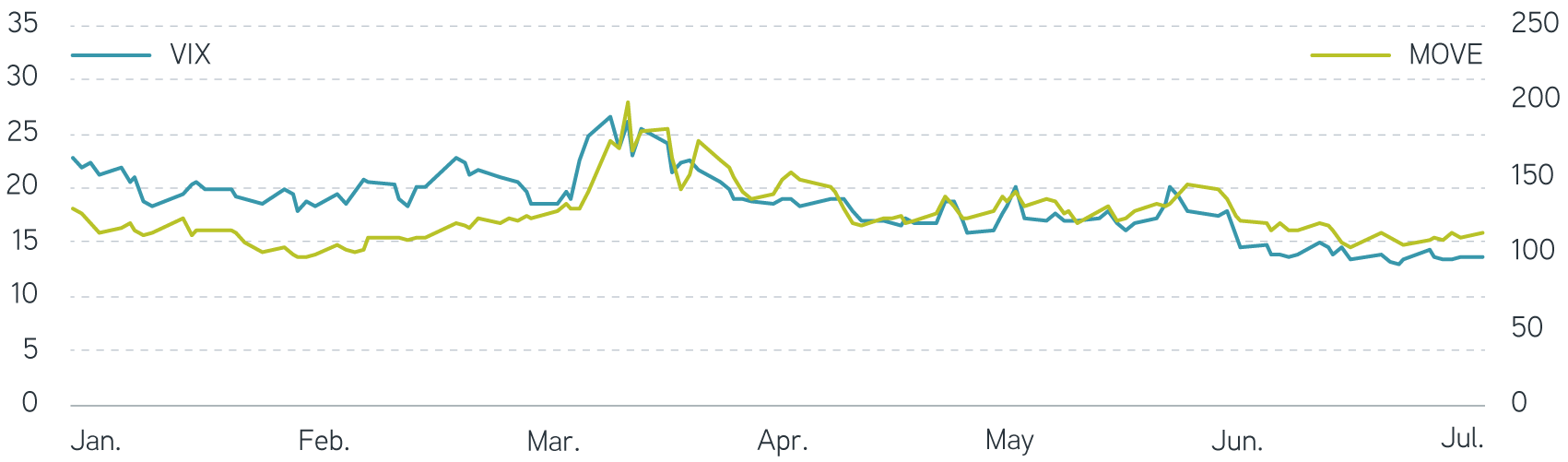

We did see some elevated equity and fixed income volatility near the end of the first quarter, as measured by the Chicago Board Options Exchange’s (CBOE) Volatility Index (VIX) and the Merrill Lynch Option Volatility Estimate (MOVE) Index following regional banking events. Markets have largely shrugged off these concerns, however. All things considered, given the market uncertainty we outlined at the beginning of the year, those market returns aren’t too shabby.

Volatility indexes, year-to-date

Sources: CBOE, Merrill Lynch, 7/3/2023. For illustrative purposes only. Past performance is not an indicator of future results. It is not possible to invest directly in an index.

Where has all that left pension plans? The Milliman 100 Pension Funding Index started the year at 101.9%, hit a low of 99.6% in April, and finished May at 100.7%. Beginning 2023 with improved funded ratios, plans generally invested more in LDI, causing assets and liabilities to perform similarly YTD, leaving plans’ funded ratios in line with levels at the beginning of the year.

Refine and enhance liability-driven investing strategies

How should plan sponsors navigate the inverted yield curve?

In our midyear fixed income outlook, we discussed why we see the market entering a peak-rate hold period, which has historically been a favorable environment for fixed income investors. Some plan sponsors have taken a gradual approach to LDI over the better part of two decades, expecting rates to go up. Over the past 18 months, rates finally have risen—and rapidly—as the Fed attempts to tackle inflation. Now it appears we’re nearing the end of that battle, and historically yields have worked their way back down a bit after such a peak.

That’s great for bond returns, but for pension plans that means liabilities increase in tandem. Higher discount yields have helped pensions overcome 2022’s poor returns on assets, and in most cases, pensions were fortunate for once to be underhedged. However, being underhedged when rates go down has a negative impact. As risk managers first, we don’t rely on forecasts of where yields will go from here. Instead we try to mitigate uncompensated risks and narrow the range of unexpected funded status outcomes, thus preventing untenable surplus loss.

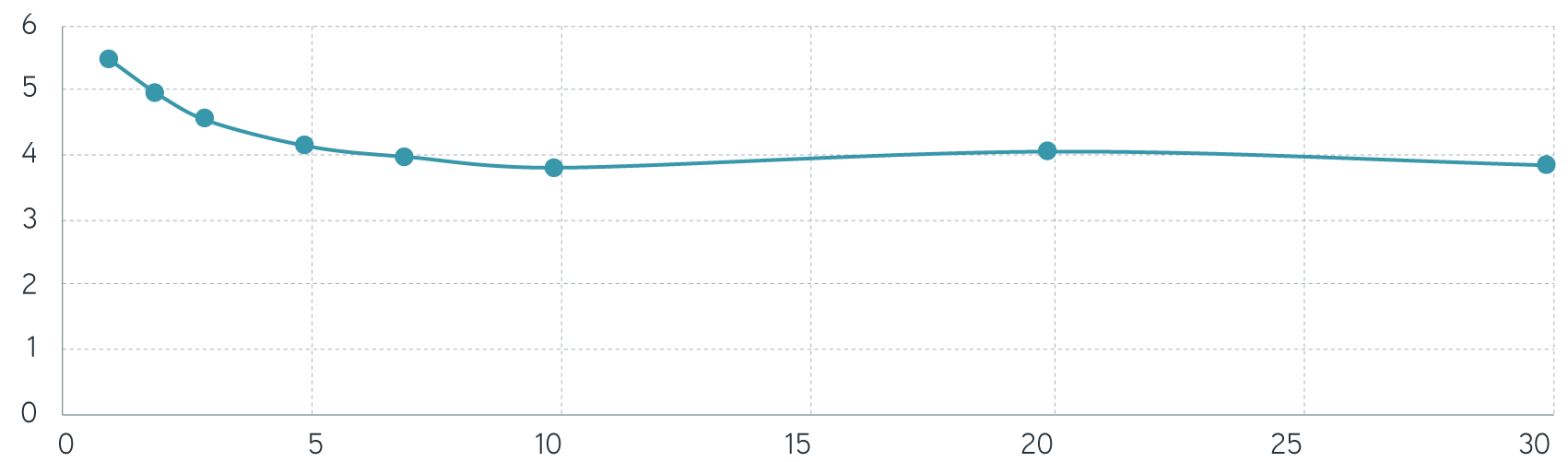

Our midyear fixed income outlook also shows something interesting about the inverted yield curve. The current inversion, as measured by the spread between 10- and two-year US Treasury yields, is at a level not seen in more than four decades. From an asset-only perspective, short rates are relatively attractive, but we prefer extending duration to lock in rates as recession risks begin to mount. From an LDI perspective, longer duration is good for hedging long-duration liability exposures too. However, it might be worth considering where and how across the yield curve plan sponsors are taking risks, a topic we discussed earlier this year.

Inverted yields may benefit pension plans further in some cases. For example, matching near-term liability and bond cash flows allows a plan to take advantage of higher short-term yields without having to worry about reinvestment risk, because positions simply mature to pay benefits out of the plan. This strategy could also reduce liquidity pressure by allowing the plan’s assets to weather volatile markets without having to liquidate at low prices to fund benefit payments.

US government benchmark yields, 6/30/2023

Source: Refinitiv, 6/30/2023. For illustrative purposes only. Past performance is not an indicator of future results. It is not possible to invest directly in an index.

How might credit spreads affect plan funding?

Finally, let’s consider credit spreads. Right now pensions are pretty well funded in general. Many plans have target allocation glide paths in place that shift assets from return-seeking to liability-hedging as funding improves. Plans take less risk because they no longer need it as the plan becomes better funded. As plans move more assets to fixed income, pension plans will likely no longer need more exposure at the long end of the yield curve, since that’s already been covered. We should see a shift to increase the intermediate fixed income allocation to hedge across the entire curve.

Currently intermediate credit spreads appear favorable relative to long duration. Demand for bonds at different maturities has resulted in long bonds being priced relatively rich, while intermediate bonds are priced relatively cheap. As of the end of June 2023, spreads on the ICE BofA 10+ Year AAA-A US Corporate Index were 123 basis points (bps), while spreads on the ICE BofA 1-10 Year AAA-A US Corporate Index were 93 bps, compared to 10-year averages of 138 and 80 bps, respectively. To the extent needed or desired, plans can restore and refine any duration shortfalls caused by investing in lower-duration corporate bonds through interest rate overlays.

The bottom line

Remember, LDI is a risk-mitigation strategy. We like to say “LDI is everything,” meaning sponsors should look at the plan in total—all assets, all liabilities, and how they interact—to completely understand and address plan exposures. Whether a plan has arrived at stable funding levels and is in hibernation or isn’t as far along as sponsors would like, they should take advantage of opportunities to continue refining and enhancing their LDI approach.