As investors wait for inflation to settle down, diversification and rebalancing provide better protection than market timing. We explore the economic threats that make this protection necessary.

Inflation has turned into a harder beast to tame than many of us anticipated just 12 months ago. Not only are prices continuing to remain high, but there’s a real potential for above-target inflation persisting for the next few years. This outcome is possible in spite of Federal Reserve chair Jerome Powell’s recent warning that he's willing to accept slower growth and higher unemployment, if that’s what it takes to achieve price stability. At their meeting last month in Jackson Hole, Wyoming, central bankers from around the world agreed that interest rates might have to rise further and remain high for longer for just that reason.

Increasing government debt loads, worker shortages, a slow and choppy transition to renewable energy, and continued geopolitical tension may counterbalance the central bank’s ability to course-correct inflation back to its 2% target. Investors need to consider the very real possibility that inflation may remain a concern for the next several years. They can take steps today to protect their portfolios from this new inflation reality. Let’s look at some of them.

Inflation fighter #1: Boosting diversification

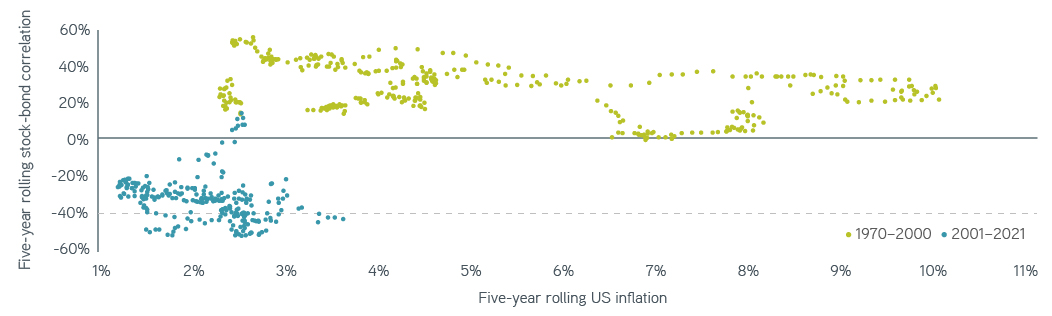

A key challenge that inflation poses to investors is its effect on the correlation between stock and bond prices, a fundamental determinant of risk for the traditional balanced portfolio. When economic growth drives asset prices, stock and bond returns tend to diverge from one another, allowing investors to take the traditional approach of relying on stocks for growth and bonds for income and diversification benefits. But when inflation drives asset prices, stock and bond returns tend to move in tandem.

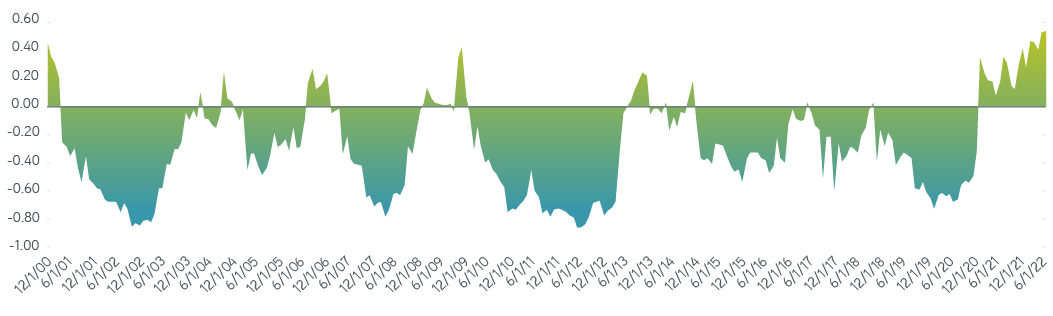

Low levels of inflation coupled with episodic periods of growth have resulted in stock–bond correlations hovering near -0.5 for most of the last two decades. This outcome produced a high level of diversification benefits and thus lower risk for a traditional portfolio. The asset class relationship changed in the first half of 2022: The S&P 500® dropped 20.6%, while the Bloomberg Treasury Index was off 9.1%. We witnessed similar changes to the stock-bond relationship during inflationary periods throughout the latter half of the 20th century.

Twelve-month stock-bond correlation, 1970–2021

Source: Morningstar Direct, 9/2/2022. For illustrative purposes only. Not a recommendation to buy or sell any security.

Twelve-month stock-bond correlation, 2000–2022

Source: Bloomberg, Barclays, 9/1/2022. For illustrative purposes only. Not a recommendation to buy or sell any security.

Investors could consider other asset classes as a way to gain further diversification for the traditional portfolio and protection from inflation. For example, an allocation to a broad basket of commodities has historically provided strong protection against above-consensus inflation and diversification versus stock and bonds. Commodity returns are especially sensitive to the Consumer Price Index (CPI)—the inflation measure that attracts the most attention—driven largely by demand for raw materials and food and energy consumption. A 5% commodity allocation can offer significant protection to a broader portfolio dominated by equity and bond risk. In the first half of 2022, while more traditional asset classes came under pressure, the Bloomberg Commodity Index went up 18.4%.

Boost diversification and fight inflation

Inflation fighter #2: Setting bonds in motion

As mentioned above, investors typically hold bonds for income and expected diversification benefits versus typical growth-oriented assets. However, an inflationary environment typified by rising rates poses a challenge to static bond investments. Fixed income mutual funds and exchange-traded funds (ETFs) can expose investors to interest rate risk and shifting returns, while individual bonds can lock investors into longer-dated maturities. This outcome will likely become even more worrisome if central banks follow through on their commitment to continue to tighten financial conditions until inflation reverts to the 2% target.

A laddered corporate or municipal bond portfolio consisting of evenly weighted maturities of bonds can help by moving alongside the markets. Laddered bonds regularly experience maturities or a cohort of securities rolling out of their target range, at which point they can be sold. In both cases the proceeds are reinvested at higher interest rates. The ladder structure also takes advantage of a bond’s natural movement down a positively sloped yield curve over time. A laddered fixed income portfolio can also benefit from thoughtful exposure to credit, be it municipal or investment grade. Most importantly, equal weighting should provide attractive long-term returns relative to most passive portfolios.

Inflation fighter #3: Embracing volatility

Inflation eats away at the value of a portfolio over time, requiring investors to earn a higher threshold return just to maintain purchasing power. For this reason, investors in inflationary environments need to seek out opportunities to add an incremental return to their portfolio that ideally exhibits a low correlation to their other assets. Ongoing or reoccurring inflation tends to coincide with increased equity market volatility as investors continually reevaluate a company’s ability to defend its profit margins in a rising cost environment. As volatility rises, so does the demand for protection from market volatility.

Harnessing the volatility risk premium (VRP) may provide one solution to this problem. The VRP is what investors are paid for providing protection against market volatility. Investors willing to bear this risk can add this diversifying and potentially material risk premium to their portfolio to offset some of the negative effects of inflation. The VRP can be introduced into a portfolio on its own or commingled with other assets. Individual investors will ultimately need to determine what solution works best for their needs.

The bottom line

Only the decisions of a few powerful individuals can ease price pressure on investors and consumers worldwide—and even those would need time to take effect. But investors don’t have to wait passively for those decisions to come. They should prepare their portfolios now to withstand continued inflation and other unexpected market events. A diversified, risk-managed, and regularly rebalanced portfolio is an investor’s best defense against whatever the future brings us.

The Bloomberg Commodity Index (BCOM) is formerly known as the Dow Jones-UBS Commodity Index. BCOM is a broadly diversified index composed of futures contracts on physical commodities.