Fighting inflation is a lot like battling a wildfire. Taming it before it gets out of control is key; the greater it grows, the harder it is to stop. If you’re a homeowner, wildfires are a large risk you might have to contend with, though improvements in building codes, materials, and construction techniques mean houses built today have a greater chance of surviving a fire than those just 30 years ago. The same may not be true for investors who seek to protect their portfolios from high inflation, particularly if they haven’t made improvements in portfolio construction.

When building an inflation-protected portfolio, we often find one important asset class missing: commodities. This can be a material misstep for investors seeking to maximize long-term growth, especially when the end goal is to either maintain or increase the purchasing power of their assets. On the surface, this means that a portfolio must grow equal to or faster than inflation. For most common assets this isn’t a problem, because part of their expected return is directly tied to compensation for expected inflation. The trouble starts when inflation exceeds anticipation and investors are hit with a one-two punch: Their purchasing power is eroded, and the investments in their portfolio may decline in value. Indeed, the recent bout of high inflation in the US has placed this concern top-of-mind for investors. Over the past year, consumer prices have shot up 8.6%, stocks have pulled back roughly 20% from recent highs, and bonds have dropped more than 10%.

Although many investors and economists are expecting inflation to soften over the next couple years because of recent and potential future policy decisions by the Federal Reserve, it never hurts to be prepared for the unexpected. Our analysis indicates that an allocation to diversified commodities has historically provided the best protection against periods of above-consensus inflation, which are devilishly difficult to foresee. Equally challenging is the fact these episodes can occur when overall inflation is near the Fed’s 2% target or when it’s exceptionally high, as it is today. But all is not lost. Given the high sensitivity of commodity returns to the Consumer Price Index (CPI), we find that a small allocation to the asset class can go a long way toward protecting an entire portfolio.

Performance during unexpected inflationary periods

Over the past two decades, we’ve identified nearly 20 quarters with unexpectedly high inflation and found that owning a diversified basket of commodities performed very strongly when inflation came in above consensus (see table). The reason for this is two-fold: First, higher-than-expected inflation is often associated with strong underlying growth in the economy, which drives demand for raw materials and puts upward pressure on commodity prices. Second, food and energy consumption is a large component of CPI, so it follows that rising prices in those items will be reflected in corresponding futures contracts.

Real estate investment trusts (REITs) also held up pretty well during these periods because higher interest rates—and thus mortgage rates and rents—were passed on to investors, though they did exhibit the highest degree of volatility of any asset class considered. On average US equities modestly outperformed inflation, which may partly reflect expectations for higher future cash flows offsetting a rise in the discount rate. In contrast, rising rates proved discouraging for US fixed income returns, which experience a price decline when yields increase. Finally, Treasury Inflation-Protected Securities (TIPS) performed only modestly better than the CPI, which isn’t unexpected. This is best understood by recalling that the nominal yield on TIPS is made up of two components: actual inflation as measured by CPI and the real yield in the marketplace. TIPS prices have benefitted only slightly from declines in real yields during periods of unexpectedly high inflation, meaning that TIPS returns haven’t seen strong rallies, on average.

Helping investors fight inflation through disciplined portfolio construction

Performance in quarters of unexpectedly high inflation, April 2002–March 2022

Notes: For our analysis, we classified each quarterly period as a positive or negative surprise by looking at the value of the Citi Inflation Surprise Index, which is an accumulation of headline CPI, PPI, and wage surprises relative to median expectations of professional forecasters. A positive reading means that releases have been better than expected, while a negative reading means that releases have been worse than expected. Next, we defined each period as having unexpectedly high inflation if the positive surprise fell within the top 50% of quarterly observations, which was roughly 20% of the time over this period.

Sources: S&P Dow Jones, MSCI, FTSE Russell, Bloomberg, and Parametric, as of 5/24/2022. Diversified commodities represented by S&P GSCI Equal-Weight Select Index, US equities represented by MSCI USA Gross Return USD Index, US fixed income represented by Bloomberg US Aggregate Bond Index, TIPS represented by Bloomberg US Treasury Inflation-Linked Bond Index, REITs represented by FTSE Nareit All Equity REITs Total Return Index. For illustrative purposes only. Past performance is not indicative of future results. It is not possible to invest directly in an index.

Commodities outpunch their weight when it comes to inflation protection

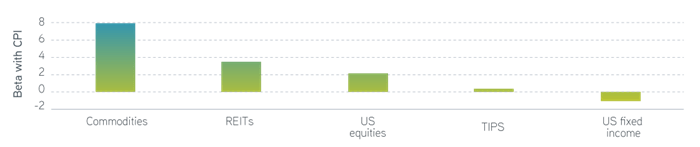

An important consideration when adding inflation-sensitive assets to a portfolio is how much protection you’re getting. A common technique to assess this is to estimate an asset’s beta against the CPI, which measures how much returns for the asset change with a one-unit change in inflation. For example, a beta of one would indicate that if inflation was 1%, the asset would produce a return of 1%. When it comes to inflation protection, a higher beta is better because it translates into greater protection across the entire portfolio. The following chart contains beta estimates for common asset classes versus CPI over the past 20 years.

Quarterly beta against CPI for selected asset classes, April 2002—March 2022

Sources: S&P Dow Jones, MSCI, FTSE Russell, Bloomberg, and Parametric, as of 5/24/2022. Commodities represented by S&P GSCI Equal-Weight Select Index, US equities represented by MSCI USA Gross Return USD Index, US fixed income represented by Bloomberg US Aggregate Bond Index, TIPS represented by Bloomberg US Treasury Inflation-Linked Bond Index, REITs represented by FTSE Nareit All Equity REITs Total Return Index. For illustrative purposes only. It is not possible to invest directly in an index.

Commodities have a well-earned reputation for their high degree of inflation sensitivity, which has some important implications when it comes to considering how much to include in an overall portfolio. For most investors seeking broad protection, a useful starting point is to consider how much of the portfolio has a low beta to inflation. An allocation to commodities can help plug this gap. For instance, if 40% of the portfolio is in fixed income, which has a low inflation beta and generally underperforms when inflation hits, a 5% allocation to commodities could do the trick. That’s because commodities would be expected to outpace inflation by a factor of eight, offering protection on up to 40% of a portfolio (5% × 8). A portfolio with fewer inflation hedging assets may require a modestly larger commodity slice, and vice versa.

The bottom line

Most portfolios already carry allocations to more traditional assets like stocks, bonds, and cash but may lack exposure to assets that do well during periods of unexpectedly high inflation. In this inflation environment, however, an investor’s portfolio may be most vulnerable. Not only can its purchasing power be eroded by higher-than-expected inflation, but its market value may also be eroded by falling stock and bond prices. Investors looking to hedge this risk can be best served by increasing their exposure to asset classes with a positive expected return when unexpectedly high inflation hits. Historically, commodities have served this purpose well, outperforming other asset classes when inflation has been unexpectedly high. Given the asset class’s high sensitivity to inflation, a modest allocation in a diversified portfolio is often all that’s needed to mitigate this risk.