Quality is an alluring factor, particularly in times of turmoil, and yet consensus on what it means remains elusive. Let’s discuss some quality strategies readily available to investors and how to find the one that best fits their objectives.

One of the most common observations about the quality factor is that there’s no consensus on its definition. This could be said about a lot of things in investing, but the definition of quality across investment vehicles is especially varied, in terms of both what investors consider its markers and how we quantify those markers. Because these choices can make a big difference in portfolio performance, navigating the quality landscape may seem daunting. We recommend a simple checklist to help investors find their bearings.

What do we mean by quality investing?

Quality investing targets companies with enduring, sustainable business models expected to withstand challenging conditions and help grow and preserve capital over the long run. Even if opinions vary about the characteristics defining quality, three themes are common: profitability, earnings quality, and capital structure.

Profitability goes to the heart of what it means to be a successful enterprise. As one might expect, most quality factor strategies include some measure of profitability. Profitability summarizes what remains for shareholders after expenses, and we can measure it in multiple ways, such as gross margins, return on equity, return on assets, or return on invested capital. Research has found that more profitable companies tend to earn an excess return relative to less profitable companies.

Earnings quality is another angle on quality investing, one that takes into account the variability of realized earnings. Quality investors tend to view less variability and steadier growth more favorably. They may also scrutinize accruals, which represent earnings that are booked but may not be fully realized. Accruals could be a sign of intentional earnings management, where revenues are pulled into the current quarter at the expense of later quarters. However, accruals could simply be a sign of overly optimistic sales projections and associated inventory buildup. Either way, avoiding companies with a large gap between earnings and cash flow can complement profitability criteria and help investors select companies with more persistent earnings.

A third quality theme is capital structure. Quality investors typically evaluate capital structure by leverage measures, but some might also consider equity or debt issuance or even dividend payout ratios. Higher leverage can be beneficial to equity holders during an expansionary part of the business cycle, then work against them during contractionary periods, pushing the company into distress in strong downturns. For this reason, quality investors might prefer companies with less leverage as a mitigation against downturns and to enhance their portfolio’s defensive positioning. Metrics such as debt or equity issuance and dividend payout can provide clues to manager discipline. Quality investors tend to prefer constrained issuance and steady, non-zero payout ratios.

How is the quality factor measured?

While some investors may satisfy their quest for quality by selecting a quality-focused active manager, others prefer a more transparent, rules-based approach. There are a number of indexes and associated ETFs for those investors. Still, transparent and rules-based aren’t the same thing as consensus-driven, and investors should make sure they understand the approach a given strategy takes to pursuing quality. To illustrate how different these approaches can be, let’s take two of the most popular US-based quality indexes viewed from the perspective of associated ETF assets: the MSCI USA Sector Neutral Quality Index and the S&P 500® Quality Index.

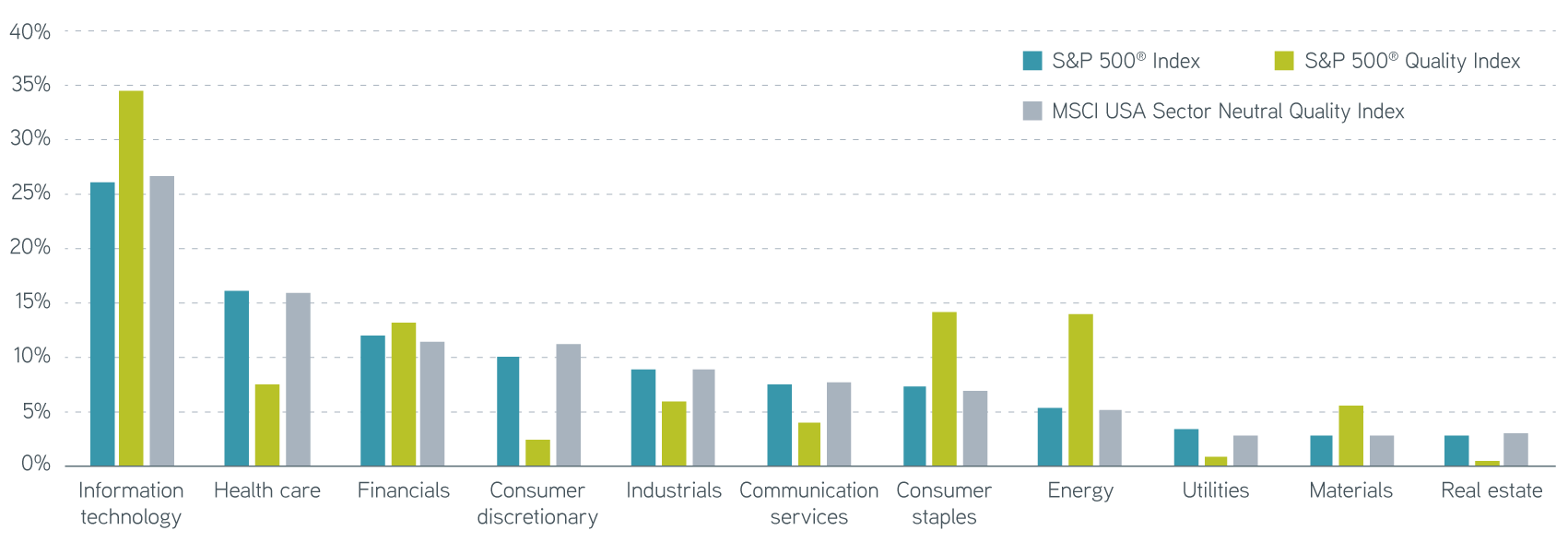

One of the biggest differences between the two is that the S&P 500® Quality Index selects the 100 constituents from the S&P 500® with the highest proprietary quality score, regardless of industry. By contrast, the MSCI USA Sector Neutral Quality Index evaluates quality within sector and constructs a more sector-neutral portfolio. Both indexes weight the constituents by combining the quality score and the passive market-cap weight.

These approaches result in different sector exposures. In particular, as of the end of 2022, the S&P 500® Quality Index was overweight to information technology, consumer staples, and energy by more than 5% each and underweight to health care and consumer discretionary by more than 5% each compared with the S&P 500® Index. The following chart shows December 2022 data, for which March 2023’s Global Industry Classification Standard (GICS) reclassification didn’t skew sector composition.

Get risk-controlled access to factor strategies

GICS sector exposure by market capitalization as of 12/31/2022

Source: S&P and MSCI via FactSet, 12/31/2022. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

In addition to the difference in sector methodology, a key difference between the two quality indexes is in the definition of quality itself. At first glance, they may seem quite similar. Both indexes include measures for profitability, earnings quality, and capital structure, and both equally weight the three themes. In the case of profitability and capital structure, they happen to use identical measures. Both measure profitability by return on equity, and both view capital structure from the perspective of leverage and measure it by debt to equity. However, they differ in their measure of earnings quality: The MSCI Quality Indexes use earnings variability, and the S&P 500® Quality Indexes use a balance-sheet-based accruals ratio.

Quality factor definitions by index

Sources: MSCI Quality Indexes Methodology, May 2022; S&P® Quality Indices Methodology, 10/1/2022. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index.

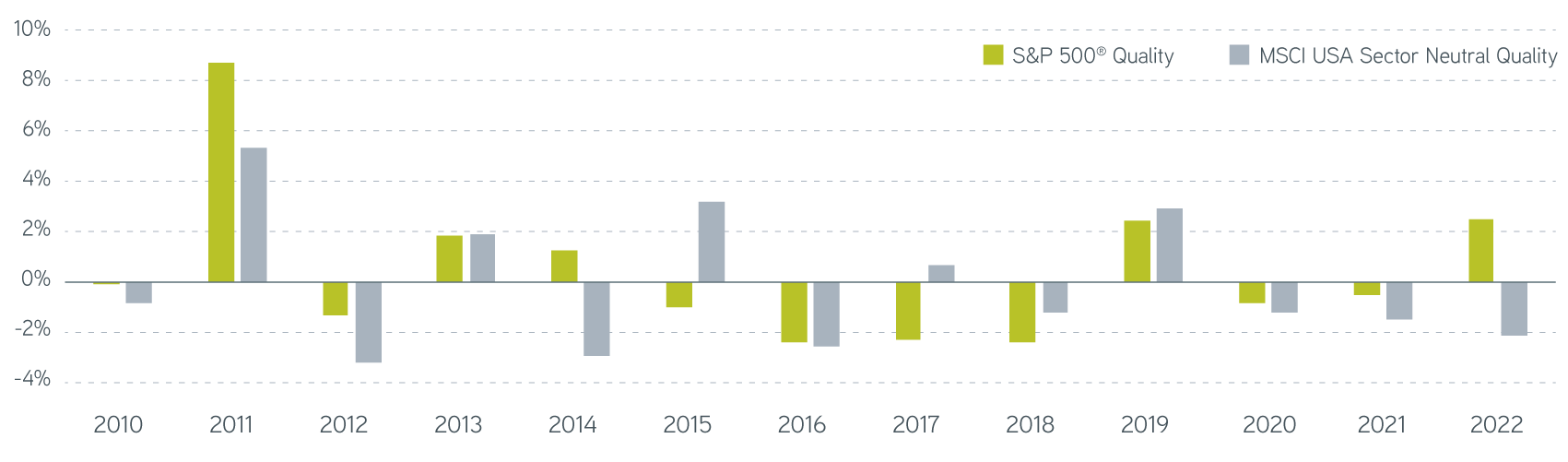

Unsurprisingly, as a result of the differences in sector methodology and the definition of quality, along with other choices such as selection universe and reconstitution timing, returns for the two indexes can be quite different from one another during any given year.

Annual excess quality index return vs. S&P 500®

Source: S&P® and MSCI via FactSet, 12/31/2022. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index.

How should investors choose a quality approach?

The discussion above is intended to reflect the kind of diversity that can be present in a given quality strategy and what investors might want to look out for. To put a finer point on it, here’s a checklist investors could use when selecting a quality portfolio:

- Definition of quality: What kind of themes are considered, and how is each measured?

Should the portfolio include a broader set of measurements or a more limited set?

Should the portfolio place greater emphasis on some of these themes than others? - Method of incorporation: How should the portfolio balance the quality characteristics with other characteristics, such as sector or country representation or other factors? Is the portfolio taking unintended bets on characteristics that have nothing to do with quality?

- Selection universe: What geographic or market cap representation should a quality portfolio include?

In our own work with investors seeking quality portfolios, we tend to include metrics for all three of these themes, but we place greater emphasis on profitability and include a variety of metrics for each theme. We also control for unintended tilts on other characteristics, such as beta and price-to-earnings ratio, to avoid taking on tracking error from risk factors other than quality.

The bottom line

Those striving to invest in durable businesses that are prepared to weather downturns may find it overwhelming. Investors must first decide what truly constitutes a quality stock. Those willing to dig under the surface may be able to find transparent, risk-efficient strategies that emphasize the quality characteristics they care most about.

Special thanks to investment engineer Supriya Bharati for her significant contributions to this post.