Drawdowns in the bond market this year have left many scurrying for shelter. For investors with liquidity needs or a low tolerance for duration, the front end of the muni market could be just what they’re looking for.

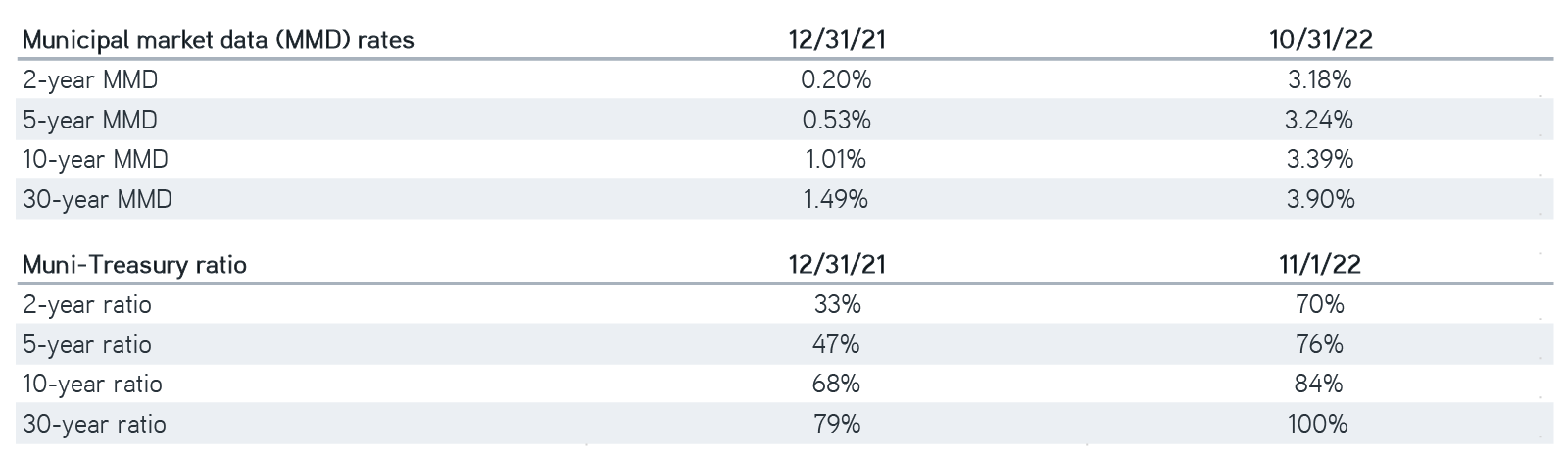

To date, 2022 has been a painful year for investors in most asset classes. However, the fixed income market—municipal bonds specifically—has suffered a drawdown in line with some of the worst in history. Stubbornly high consumer price inflation caused the Federal Reserve to quickly pivot from accommodative monetary policy to hiking six times, bringing the target range between 3.75% and 4%. This policy has contributed to a dramatic increase in nominal interest rates and a significant adjustment of municipal bond valuations.

Municipal valuations, year-to-date changes

Sources: Bloomberg and Thomson Reuters, 11/1/2022. For illustration purposes only. Not a recommendation to buy or sell any security.

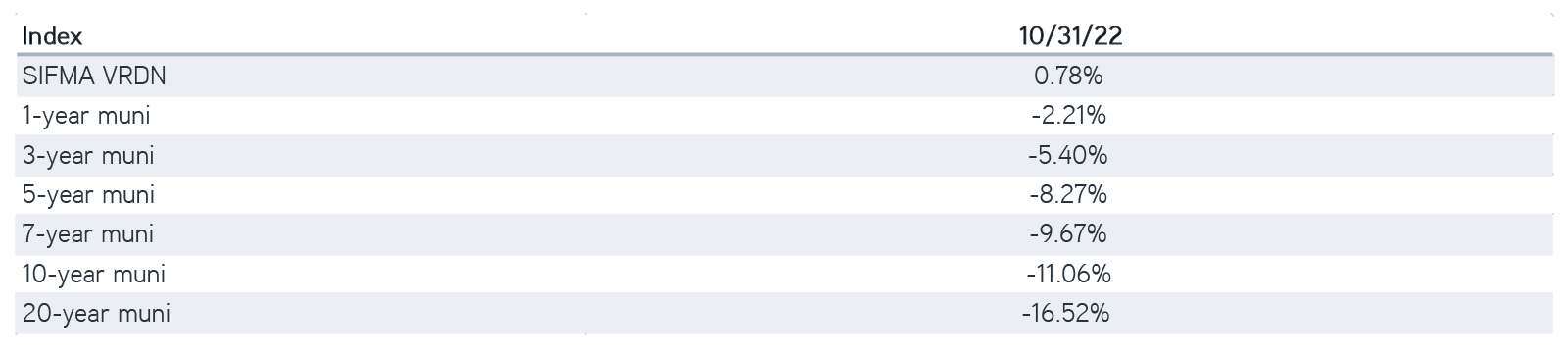

Faced with this situation, many investors may feel the need to ask, “Where can I hide”? The answer is the front end of the muni curve (generally seven years to maturity or shorter). The next chart shows the total return year-to-date for various parts of the investment-grade universe. This clearly displays front-end outperformance relative to other tenors of the muni curve. In fact, if an investor simply purchased weekly reset variable-rate demand notes (VRDNs) and held them throughout the year, they would have outperformed all other segments of the muni universe.

Variable-rate demand notes

Source: Bloomberg, 10/31/2022. For illustration purposes only. Not a recommendation to buy or sell any security.

Predictable income and capital preservation

Variable-rate demand notes

VRDNs are a unique type of municipal debt that allows investors to gain exposure to the tax-exempt market without taking on any duration risk. These instruments are often issued with long maturity dates and a standing option for investors to put them back at par either weekly or daily, depending on the note type. Remarketing agents earn their pay by accepting these tenders, then “remarketing” the bonds weekly or daily at a rate that clears the market. This allows the yield on these notes to float in response to changes in the market environment. The coupon is paid on a monthly basis and calculated by the sum of the coupon rates for the previous month. This causes VRDNs to have no price sensitivity to changes in interest rates, and they serve as an excellent option for investors with liquidity needs or those who want to hedge against rising rates.

Opportunities

The Securities Industry and Financial Markets Association (SIFMA) Municipal Swap Index is an average of all outstanding weekly-reset VRDNs. That average currently sits at 2.45%, a tax-free rate. That represents more than half the yield available by purchasing a 30-year AAA-rated 5% coupon municipal bond. For investors who anticipate sticky inflation and higher rates, a portfolio with a mix of short-fixed-rate paper and a meaningful allocation to VRDNs could produce a yield that picks up a healthy percentage of all the yield the curve has to offer, while providing some insulation from the pain of further interest rate increases. For those with known future liquidity needs, a customized portfolio with VRDNs that can be put back at par and fixed-rate bonds that mature on or right before the future cash outflow dates will add considerable value relative to other short-term options like tax-exempt money market funds.

Alternately, for investors without known liquidity needs but with a tolerance for a moderate amount of duration, a simple one- to five-year laddered portfolio represents an attractive short-term option. With an all-in tax-exempt yield north of 3% and a duration of approximately 2.5 years, such a portfolio would earn back the negative price performance associated with a 1% increase in rates in less than one year. If rates continue to rise, the structure of such a portfolio—with 20% maturing each year—provides a natural hedge against price declines by dollar-cost averaging approximately 20% of the portfolio annually into the higher yield environment. The defensive characteristics of a short ladder could mean the investor is rooting for higher yields.

Given the drawdown in the municipal market this year, many corners of the market offer attractive opportunities, with absolute yields not seen since 2007. Depending on the investor’s goals and objectives, many options present attractive total-return prospects. For those with known liquidity needs or a low tolerance for duration, look no further than the front end of the municipal market.