As we near the end of the Federal Reserve’s interest rate hikes, fixed income investors may find themselves wondering what approach to take when it comes to municipal bonds. History tells us it might be best to play the long game.

After the most extreme period of interest rate increases in more than 40 years, we’re approaching the federal funds rate peak for this cycle. According to the federal funds futures markets, investors are expecting overnight rates to finish 2024 at 4.25%. The Federal Open Market Committee dot plot calls for the fed funds rate to finish the next calendar year at 4.625%, according to its Summary of Economic Projections from June 14.

Whether you put more faith in the market or in the Fed, both agree that by next year’s end we’ll likely see a lower fed funds rate than the current 5.25%–5.5% range we’re operating in. So what does that mean for fixed income investors?

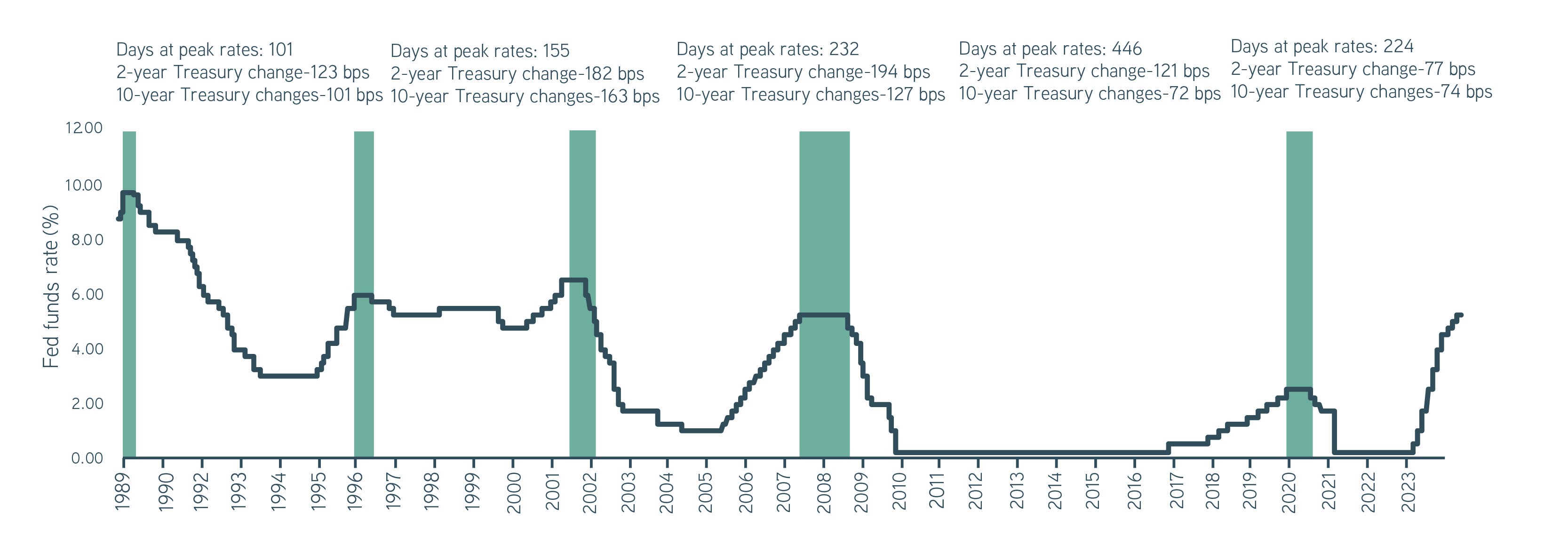

How have long-term bonds performed after peak rates?

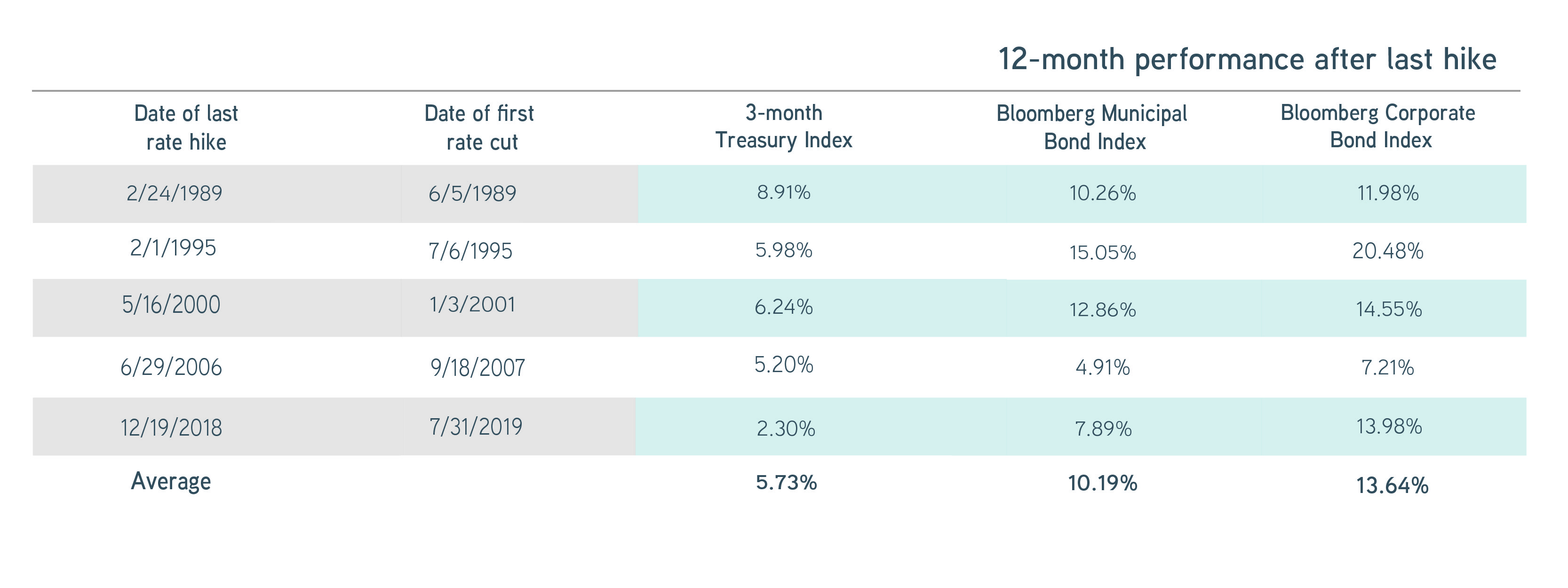

History would suggest that fixed income investors can benefit from taking on longer-term exposure rather than short-dated treasuries before the Fed shifts its posture and begins cutting interest rates. Looking at the last five rate-hiking periods, the Bloomberg Municipal Bond Index has returned an average of 10.19% for the 12-month period following the most recent Fed rate hike. As measured by the Bloomberg Corporate Bond Index, corporate bonds have returned an average of 13.64%. Three-month Treasuries returned 5.73% over the same period. Being in longer-duration bonds rather than cash alternatives has historically shown value when a hiking cycle ends.

How have long-term bonds performed after peak rates?

Source: Bloomberg, 6/30/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

Fixed income index performance during and after interest rate hold periods, 1989–2019

Source: Bloomberg, 6/30/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

Timing the market and confirming the end of a hiking cycle is notoriously difficult and can only truly happen in hindsight. It’s possible that the Fed will increase their overnight rate more from here. However, with slowing job growth, the Fed’s June pause, and inflation heading downward, there are growing indications that we’re getting closer to or have arrived at the end of the current hiking cycle.

Flexible fixed income solutions for turbulent times

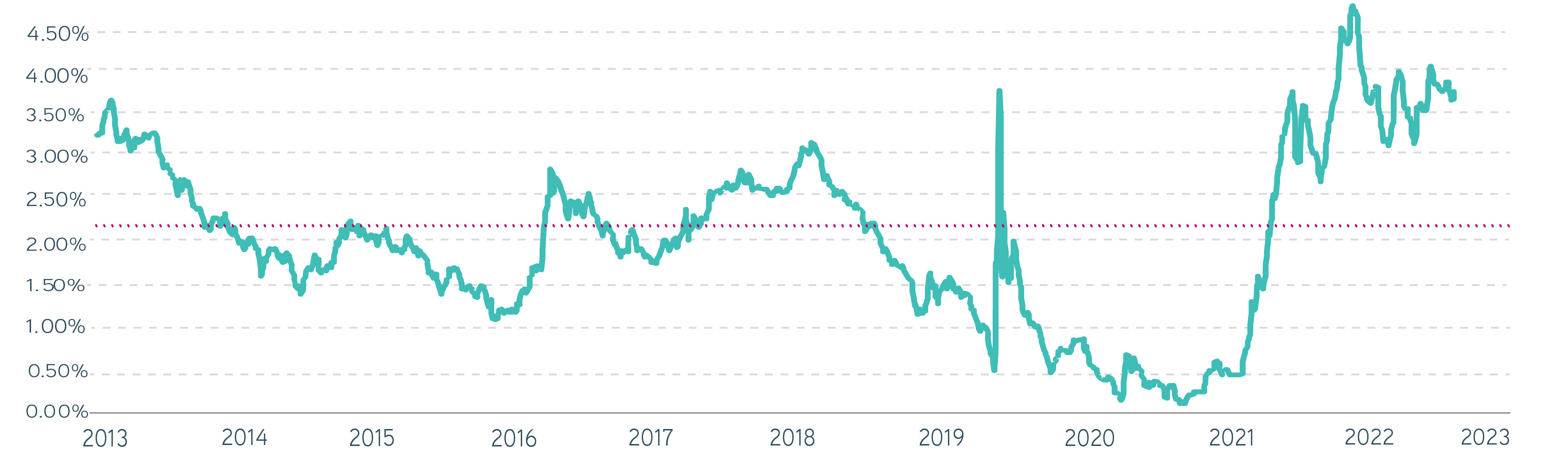

Following the historical trend is compelling. Investors currently can achieve some of the most attractive yields in longer-term fixed income relative to the last decade. In fact, through August 21, the Bloomberg Municipal Bond Index yield-to-worst (3.8%) is higher today than it’s been 98% of the time in the past 10 years. Even if rates stay in the current trading range, investors in the highest tax bracket are seeing a taxable-equivalent yield-to-worst of 6.42%, assuming the highest level of federal taxes and the Affordable Care Act investment tax.

Bond yields, August 2013–August 2023

Source: Bloomberg, 8/21/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

The bottom line

Investors today are achieving attractive yields in longer-term fixed income, whether in investment-grade corporates or municipals. Specifically for municipals, supply-and-demand dynamics are supportive. High-quality corporate and municipal asset classes are broadly well positioned from a fundamental credit perspective should the economy hit the skids. Positioning fixed income portfolios out the curve today may help investors benefit when the current hiking cycle ends and we enter the next chapter of Fed policy.

Fixed income securities are subject to the ability of an issuer to make timely principal and interest payments (credit risk), changes in interest rates (interest-rate risk), the creditworthiness of the issuer, and general market liquidity (market risk). In a rising-interest-rate environment, bond prices may fall and may result in periods of volatility and increased portfolio redemptions. In a declining-interest-rate environment, the portfolio may generate less income. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads, and a lack of price transparency in the market. There generally is limited public information about municipal issuers.