0DTE options—once reserved for large institutions—are now popular among even the smallest investors. What’s behind the recent surge in 0DTE options, who trades them, and why?

Think back to two closely related market moments 20 years apart: In Berkshire Hathaway's 2002 annual report, Charlie Munger and Warren Buffett called derivatives "financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal." Then, during the COVID-19 pandemic, many people picked up a less-than-obvious hobby: trading equity options.

Options contracts allow purchasers to buy or sell the underlying security at a fixed price by a set date, and they’ve become increasingly popular since Munger and Buffett’s comment in 2002. Their usage—typically reserved for large institutions at the time—now extends to the smallest retail investors. The “mass” prediction has come true, but options’ lethality is debatable. Let’s examine the recent volume surge in options expiring in less than a day (zero days to expiration [0DTE]) and explore who trades them, their use cases (structures), their potential risks, and the importance of gamma.

Who trades 0DTE options?

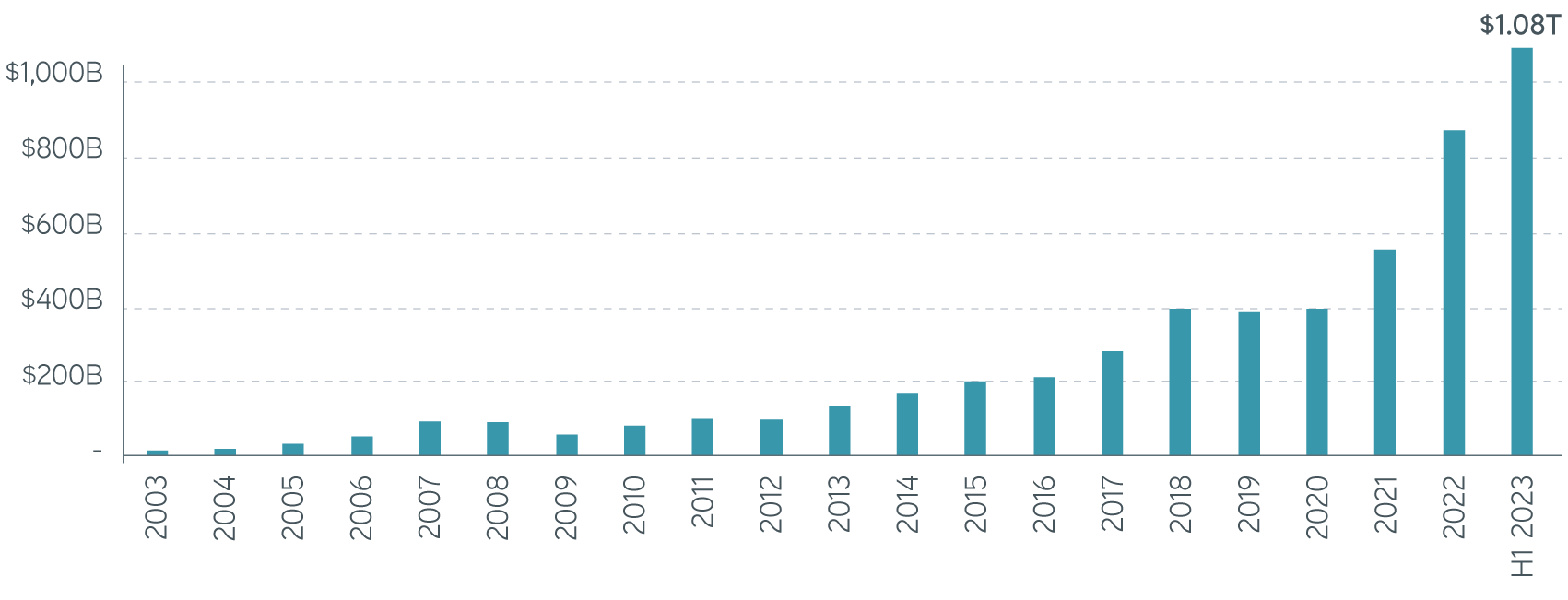

The Chicago Board Options Exchange (Cboe) lists options a few weeks before their expiration day. When options reach their final day of life, they become 0DTE. In that sense, 0DTE options have always existed. Only recently have the number and usage of discrete expirations (every trading day) accelerated. Today nearly half of the daily S&P 500® options volume comes from 0DTE trading.

Average daily S&P 500® options volume by year, 2003–2023

Sources: Parametric, Bloomberg, 6/30/2023. For illustrative purposes only. Not a recommendation to buy, sell, or hold any security.

The Cboe tracks options trading volume by origin (customer, professional customer, broker-dealer, firm, or market maker), buying or selling, and opening and closing positions. Using that data, Bank of America finds that “0DTE options are concentrated between market makers and customers,” with each representing about half of the volume. Customer includes both individual and institutional investors, which makes it impossible to identify directly whether a trade is from retail or institutional traders. Trade size may not be reliable either. For example, although small trades (one to 10 contracts) are typically conducted by retail investors, not all are.

Nevertheless, the surge in small options trades—especially single-contract options—suggests increased participation from retail traders. We estimate that up to 40% of customer volume is retail. Tracking the trade’s origin is important for predicting end-user behavior based on the “position + behavior = (potential) weapon” framework. For example, investors might wish to close positions before the market closes, having a preset condition or trigger to monetize, liquidate, or roll the position. On the other hand, market makers actively hedge their market risks.

What are the use cases for 0DTE options?

Though the actual composition of all options traded is hard to track and can vary each day, we’ve seen some common uses:

Outright speculation

Daily options expiration enables traders and investors to attempt to isolate macroeconomic events like inflation reports, Federal Open Market Committee guidance, and earning reports while paying the least amount of time value (optionality) for the position. This often involves lottery-type betting and can result in herd behavior, like with the meme stock frenzy of 2021. Investors seek to maximize a convex payout, and retail traders prefer trading single-stock options. Nearly all single-name and ETF options have Friday-only expirations, so Friday’s volume tends to be higher than other weekdays’.

Delta trading (instead of using equity index futures)

Delta trading can significantly contribute to outsized trading volumes. Market makers often use 0DTE options to manage their position exposures, including delta. On the customer side, for example, when an investor seeks to execute a large options structure with long or short delta, adding 0DTE options can offset that market exposure. This potentially improves the execution price, since brokers and market makers don’t need to bear the market risk of the trade. The investor can then let the 0DTE options expire at market close or trade out of them in small pieces during the rest of the day. Investors can also use short-term options in momentum strategies or add other options legs to control maximum loss.

Selling 0DTE to capture potential income

With options decaying faster near expiration, it’s natural for investors to speculate that selling 0DTE options can capture a premium price. The little-to-no margin requirement and end-of-day stop loss can also motivate such trades. Interestingly enough, a simple Google search for “0DTE” produces ample YouTube videos and websites promoting 0DTE “income” strategies. Those strategies usually involve a credit spread, meaning the loss is capped. Short options can face significant potential loss, and selling options in a margin account involves taking leverage.

VRP solutions with a range of options

What are the key potential risks of 0DTE options for the broader market?

Margin requirement

Trading on margin is risky and costly, requiring paying for funding. Financial Industry Regulatory Authority (FINRA) rules require day trader accounts to maintain minimum daily capital, and brokers typically limit the exposure to a trading power. Retail brokers often have tighter rules on who can sell naked 0DTE options. So the difference between buying and selling 0DTE options isn’t “none to all” but sits within a narrower range. On average, about a quarter of retail 0DTE trades receive a credit (selling). Looking at institutional investors and market makers, brokerage and clearing firms typically take position snapshots only at day’s end. Risk arises, therefore, if the margin isn’t adequately held or called for additional margin—since there are only about seven hours in a day-trading session—or for liquidation contingency. For the broad market, if the positions align, a levered position can ignite another levered position, quickly sparking stress for the broader financial markets.

Market condition

Since 0DTE options have gained popularity, we haven’t experienced the extreme volatility in financial markets we saw in March 2020 or especially 1987. The average daily move of the S&P 500® since 2022 has been about 1% in either direction. In March 2020, there were eight trading days when the index moved more than 5%. So we aren’t sure how well 0DTE options can weather a storm. We see this as a potential risk but not one likely to break the ecosystem for two reasons: Market makers actively hedge their position risks, and they’ve already experienced outsized moves in single-stock options. Said another way, they’ve tested their systems and methodologies. However, the risk of a market maker blowout isn’t zero. If Black Monday happens again, we’ll undoubtedly step into unprecedented territory for 0DTE options.

Why is gamma important for 0DTE options?

After a market maker sells a call option to a retail investor, the short position will lose money if the underlying index or stock rises. To limit this risk, the market maker needs to hedge this position by buying stock, typically in a greater value than the option premium amount. For example, a $1 call option premium might cause $5 of stock buying. What if other retail investors purchase the stock or its call options and it keeps rising? We call this gamma, when the market maker must buy more stock to hedge the exposure—say, resulting in another $5 of stock buying. At this point, the original retail investor’s $1 call option purchase has produced $10 of stock buying, maybe even more. Gamma is highest for strike prices near the underlying price closer to expiration. 0DTE options then potentially become a “gamma weapon.”

If outright 0DTE buyers and spread sellers are balanced, market makers can trade more and hedge their risk more effectively. However, we’ve seen situations where retail traders chase the market upside in equity index and single stocks. As a result, market makers’ hedging leads to even higher prices and higher demand for gamma, as seen in options prices, creating a phenomenon called “spot up, volatility up” (the S&P 500® and the Cboe Volatility Index [VIX] move higher simultaneously, when they typically have an inverse relationship).

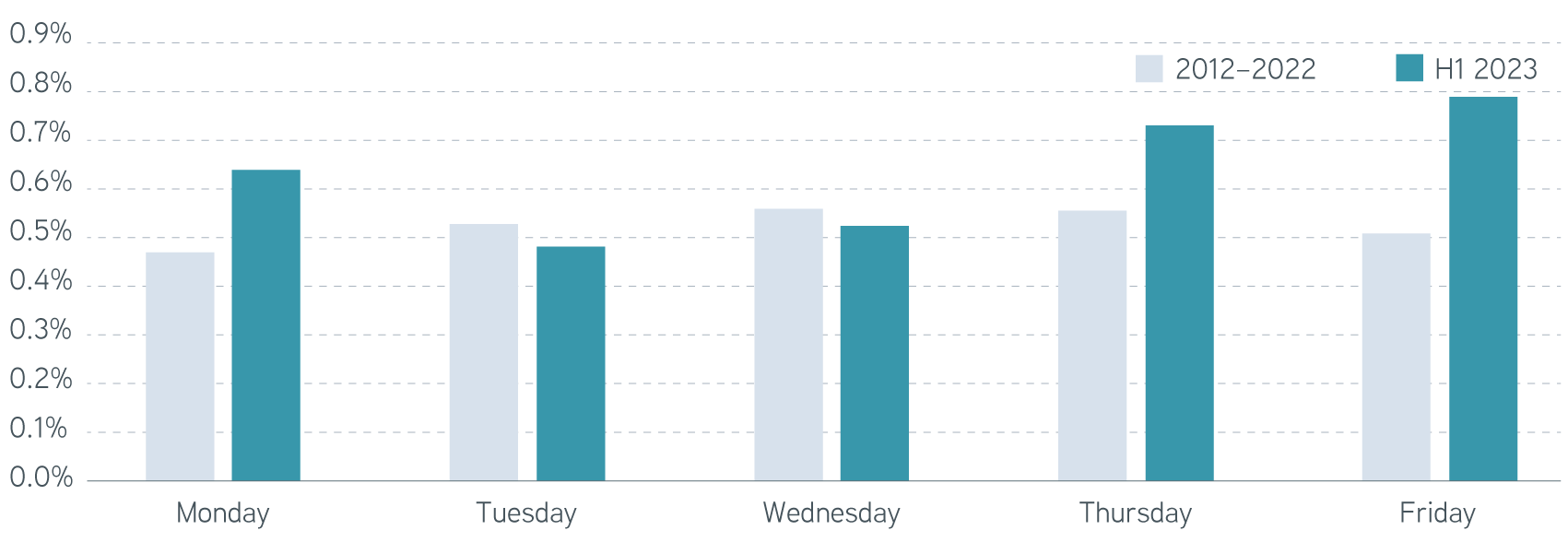

Because both index and single-stock options expire on Fridays and retail investors tend to buy more call options than puts, they can push the index or stock higher intraday, creating a wider upside price range. The following chart compares the daily high price and the S&P 500® open price in two periods with similar VIX prices. The high-to-open range was 0.5% on Fridays from 2012 to 2022. In the first six months of 2023, it was 0.78%.

S&P 500® intraday high price vs. open price, 2012–first half of 2023

Sources: Parametric, Bloomberg, 6/30/2023. For illustrative purposes only. Not a recommendation to buy, sell, or hold any security. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses.

The bottom line

0DTE options trading has the potential to either fuel or suppress market volatility, depending on positioning and owner behavior. As options sellers face an asymmetrical return-and-risk profile, we believe this highlights the importance of having multiple diversified positions in options-based volatility risk premium and overwrite strategies. We continually monitor the impact of 0DTE trading to get investors as close to right as possible.